Adviser - Checklist and Stoplist

Do you sometimes struggle to find the time to accomplish all you need to do in your work day, week, year? It’s time to take a step back, assess and organise. What’s your team’s Checklist & Stoplist?

Let's start with the Checklist.

Checklists are great. I love checklists. For those of you who aren't on the checklist bandwagon, Atul Gawande's best-selling book The Checklist Manifesto, should do the trick. Checklists are excellent tools for delivering results and optimising a team's time, especially when the checklists are simple and managed by process-focused team members.

But don't stop there. Your team has about 2,000 "Working Team Hours" per year (assuming a 42-hour work week and 2 weeks of holidays) and an increasing boatload of things to take care of—including getting through your Checklist.

How are you going to pull it off? Work harder? How about working smarter. With the help of your Stoplist .

TEAM EXERCISE: Review your Checklist and, as a team, create your Stoplist. Make sure every team member adds at least one "Stop" item to the list.

Here are some ideas to get your creative juices flowing.

1. Stop: Taking on clients who don't fit your ideal profitable client profile.

Every client deserves to be some adviser's best client. If the client doesn't fit your ideal profitable client model, give them suggestions of other advisers who might better fit their needs. Per PriceMetrix, "Outperformers recognise that, by saying no to some, they will have the capacity to deliver more to those who fit with their core value proposition."1

2. Stop: Worrying about what your clients "may" think about changing your service model.

Your clients asked you to help them make money and achieve their investment outcomes. That may mean reviewing your service model for them, but it does not mean you're reducing your value.

It comes down to confidently being able to state your value proposition to your clients. Reminding them about the value of your advice and refocusing your conversations on client goals and their overall progress towards those objectives.

Focus on the benefits that the client will gain from the new service offering - If it's partnering with an asset manager, it could be the depth of resources, insights and expertise that will monitor their portfolio and respond quickly to market conditions while managing risk. (also see #4).

Believe in your ability and demonstrate your value, be clear in your new offering on what the client will receive and when. Tell it to them straight - don't talk around the issue, get straight to the point or clients will sense a lack of confidence in your direction. Set a deadline and expectations – Prepare clients with plenty of notice and set clear expectations on when and how future progress will take place.

3. Stop: Trying to time the market.

History has taught us that trying to time the market is incredibly difficult – if not impossible. Markets can go through large swings in short periods of time and trying to determine if current market trends are going to continue or are ready to reverse can consume huge amounts of time and energy – and be extremely costly if wrong. Just look at 2017 calendar-year returns compared to returns for the first nine months of 2018.

Exhibit 1: 2017 and YTD September 2018: Rank reversals

![]()

Australian equities—S&P/ASX Russell 200 Index; World Equities ex Australia—MSCI World ex Australia Index; Emerging Markets: MSCI Emerging Markets;

Global Treasury Bonds—Bloomberg Barclays Global Treasury Index AUD Hedged; Global real estate—FTSE EPRA/NAREIT DevelopedIndex AUD Hedged;

Commodities—Bloomberg Commodity Index; Global infrastructure—S&P Global Infrastructure Index. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

In our view, a globally-diversified multi-asset portfolio has the best potential to offer long-term investing success

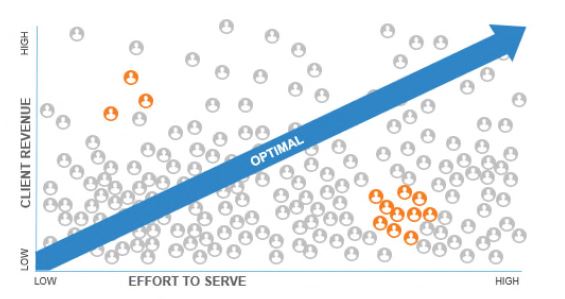

4. Stop: Building a new portfolio for every client who walks in the door.

Map your clients on a simple chart of Revenue vs Resource Allocation (or effort to service).

Keep in mind that in order to meet the best interests or fiduciary responsibility to all of your clients, you already provide a number of services for them, such as conducting trading operations, servicing their account, investment selection and reporting. When you create your map, look in particular for high revenue clients who may be at risk of being underserved.

As well, you may be able to serve the best interests of your smaller clients through the use of a model portfolio that you can adapt for their individual needs. That can help reduce the number of products you hold, thus reducing the amount of due diligence you need to do. This could free up your time to focus on helping your larger clients with their wealth management needs.

5. Stop: Ignoring the liability that comes from low-revenue clients your teams haven't spoken to in years.

Just because your team doesn't talk with them, doesn't mean you're not responsible for those clients. Consider alternative solutions such as partnering with an external asset manager who can help you with the amount of time and resources required for:

- Objective research: Independent research by the adviser focused on multiple variables, including selection, pricing, and performance.

- Subjective research: Meetings and updates to gain insight into the decision-making of the most recent quarter.

- Client education: Translating both the objective and subjective research into relevant information for client communications.

- Administration: There can be continued significant administration burdens in managing these portfolios and all this takes time and resources.

Having a dedicated and focused asset manager to provide diversified, actively managed solutions for your clients gives you the ability to use your time and resources in other areas of your business. Taking advantage of the research, reporting and insights that you can pass onto your clients.

Your aim is to create a service model for your low-revenue clients that allows you to properly serve them more efficiently. Giving you back time to spend on seeking new business, servicing your top clients appropriately and identifying those clients who have the potential to grow. The end result is the potential for increased revenue.

6. Stop: Looking for reasons not to be invested right now.

With the U.S. stock market at all-time highs, interest rates rising and geopolitical risks spreading around the globe, it could be easy to find reasons to avoid investing. However, thinking that "it's different this time" historically hasn't been a winning strategy. Time is on the investor's side and those who have stayed invested with long-term horizons nearly always have been rewarded with positive investment outcomes compared to being in cash.

Source: RussellInvestments, Datastream

Cash represented by Bloomberg AusBond bank Bill Index

7. Stop: Taking calls from "That Client," who calls all the time, puts you and your staff in a bad mood, and psychologically stops productivity.

Enough said. You know who "That Client" is in your book.

8. Stop: Giving away financial planning.

According to a 2016 Investment Trends report, the up-front cost of the first meeting with a financial planner is about $2250 on average2. It's incredibly valuable – don't give it away as part of the prospecting phase, only for clients to walk out your door with the plan and try and implement it themselves.

9. Stop: Not allocating enough time to your Centre Of Influence (COI) list.

When correctly cultivated and guided, COIs can be powerful advocates for you and your business. Yes, it takes time to deliver A-client level service to COIs—but it's how they gain an understanding of how you will treat their trusted relationships.

10. Stop: Not following through on any of the action items or best practices learned from the conferences you attended this year.

You invested the time to attend the conference—the time away from your office, your clients and maybe even your family. Do yourself the courtesy of choosing at least one action item from each conference to follow through on.

When you and your team have agreed on your Stoplist, plaster copies of it around the office and add it to your weekly team meeting so you're all holding each other accountable for correcting these habits.

The bottom line

Maximise your potential by being purposeful with your time—that includes both what your team chooses to do and what you all choose to stop doing. Time spent thinking and worrying is just as costly as time spent actually doing – both detract from your team's true productivity. Whether they are physical or psychological barriers, stop doing the things that are sucking up your team's time in order to focus on what's most important – your best clients.

What things are your team going to stop doing to take back time to focus more on clients?

1 Source: 2015 PriceMetrix The Anatomy of Outperformers

2 Source: Investment Trends 2016 Planner Business Model Repor