The eurozone: Maintain your enthusiasm Gas in the tank

In order to explain why we think there are still gains to be had, it is important to start with our analysis of both the size and value of future earnings. With respect to the size of future earnings, we see a positive impact from a continued economic recovery, rising profit margins, and a weaker euro. With GDP growth expected to continue at 1.5%-2%, driven by pent-up consumer demand, positive credit growth, a cheap euro, and low oil prices, revenue growth should be supported. At the same time, profit margins are expected to keep on trending higher as the input cost of raw materials is falling and wage growth is low. Finally, the weaker euro is supporting the export sector and is boosting foreign earnings in euro terms. Combined, we expect corporate earnings to grow by 4-8% in 2016, which, given the 10% growth1 already achieved in 2015, is quite healthy.

With respect to the value of future earnings the focus lies on the discount rate used to calculate their present value. We expect the discount rate to remain under downward pressure from loose monetary policy. Indeed, although European Central Bank (ECB) President Mario Draghi boosted monetary policy on Dec. 3, 2015, he did not quite meet elevated market expectations.

In previous reports, we’ve often focused on eurozone tailwinds and our focus on the balance between reflationary and deflationary forces. Nothing has really changed in this respect. What has changed, however, is the fact that expectations have been steadily increasing. Not only does that make it harder to surprise on the upside, it also means more of the recovery has been priced in already.

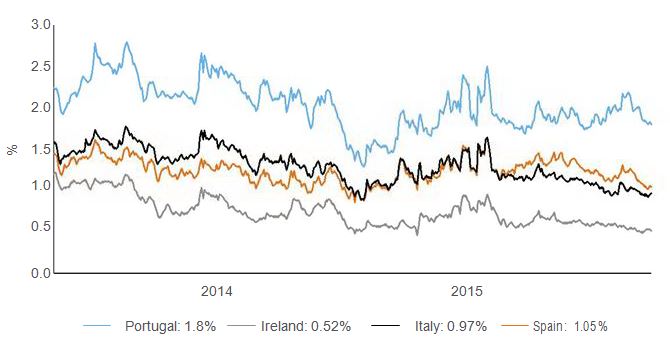

After meeting our target for 10% corporate earnings growth in 2015 we are looking for a healthy 4% to 8% in 2016. In fact, for government bonds in the periphery we have trimmed our overweight back to neutral after reaching our target spread of 1% versus German bunds (see chart on page 9). In equities, however, we still strongly favour the eurozone because the supports mentioned above are combined with relatively cheap valuations versus U.S. equities.

10-year bond spread relative to Germany

Source: Thomson Reuters Datastream: Benchmark Bonds data as of Dec. 3, 2015

Revisiting our watchpoints

As always, we continue to monitor watchpoints for signs of trouble:

- The 5-year, 5-year forward inflation swap. At approximately 1.7%, this watchpoint is still flashing amber, although only slightly. We would like to see inflation expectations pick up a bit more, and we expect the latest ECB moves to do just that.

- Credit impulse. The credit impulse (the change in credit growth) has gone back from a slight shade of amber to a slight shade of green. Credit growth has picked up again after a lull in the third quarter and the ECB’s Senior Loan Survey continues to improve.

Strategy outlook:

- Valuation: Eurozone equities are neutrally valued in an absolute sense, but they are cheap relative to the U.S. In government bonds we have gone back to neutral in peripheral bonds after having gone back to neutral in core bonds last quarter.

- Business cycle: We maintain our positive outlook for the business cycle although higher expectations have caused us to trim our score a tad. GDP growth in 2016 is expected to be 1.5% to 2%, the same as in 2015. After meeting our target for 10% corporate earnings growth in 2015 we are looking for a healthy 4% to 8% in 2016. Finally, both fiscal and monetary policies remain supportive.

- Sentiment: Price momentum is still neutral, but our contrarian indicators continue to keep the overall score slightly positive.

- Conclusion: We maintain our overweight position to eurozone equities, but we go to neutral in peripheral bonds alongside our existing neutral position in core government bonds.

1 Based on the MSCI European Monetary Union Index- (in €), 12-month-trailing earnings-per-share as of Nov. 30, 2015.

IMPORTANT INFORMATION

Issued by Russell Investment Management Ltd ABN 53 068 338 974, AFS License 247185 ("RIM"). This document provides general information only and has not been prepared having regard to your objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation or needs. This information has been compiled from sources believed reliable, but is not guaranteed. Past performance is not a reliable indicator of future performance. Copyright © 2016 Russell Investments. All rights reserved. This material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from Russell Investments.

The views in this Annual Outlook are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Keep in mind, like all investing, that multi-asset investing does not assure a profit or protect against loss.

No model or group of models can offer a precise estimate of future returns available from capital markets. We remain cautious that rational analytical techniques cannot predict extremes in financial behavior, such as periods of financial euphoria or investor panic. Our models rest on the assumptions of normal and rational financial behavior. Forecasting models are inherently uncertain, subject to change at any time based on a variety of factors and can be inaccurate. Russell believes that the utility of this information is highest in evaluating the relative relationships of various components of a globally diversified portfolio. As such, the models may offer insights into the prudence of over or under weighting those components from time to time or under periods of extreme dislocation. The models are explicitly not intended as market timing signals.

The Business Cycle Index (BCI) forecasts the strength of economic expansion or recession in the coming months, along with forecasts for other prominent economic measures. Inputs to the model include non-farm payroll, core inflation (without food and energy), the slope of the yield curve, and the yield spreads between Aaa and Baa corporate bonds and between commercial paper and Treasury bills. A different choice of financial and macroeconomic data would affect the resulting business cycle index and forecasts.

Investment in Global, International or Emerging markets may be significantly affected by political or economic conditions and regulatory requirements in a particular country. Investments in non-U.S. markets can involve risks of currency fluctuation, political and economic instability, different accounting standards and foreign taxation. Such securities may be less liquid and more volatile. Investments in emerging or developing markets involve exposure to economic structures that are generally less diverse and mature, and political systems with less stability than in more developed countries.

Currency investing involves risks including fluctuations in currency values, whether the home currency or the foreign currency. They can either enhance or reduce the returns associated with foreign investments.

Investments in non-U.S. markets can involve risks of currency fluctuation, political and economic instability, different accounting standards and foreign taxation.

Bond investors should carefully consider risks such as interest rate, credit, default and duration risks. Greater risk, such as increased volatility, limited liquidity, prepayment, non-payment and increased default risk, is inherent in portfolios that invest in high yield (“junk”) bonds or mortgage-backed securities, especially mortgage-backed securities with exposure to sub-prime mortgages. Generally, when interest rates rise, prices of fixed income securities fall. Interest rates in the United States are at, or near, historic lows, which may increase a Fund’s exposure to risks associated with rising rates. Investment in non-U.S. and emerging market securities is subject to the risk of currency fluctuations and to economic and political risks associated with such foreign countries.

The S&P 500, or the Standard & Poor’s 500, is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

The Russell Eurozone Index measures the performance of the equity markets located in the Euro Zone, based on all investable equity securities in the region.

The Bloomberg U.S. Aggregate Bond Index is a broad based index often used to represent investment grade bonds being traded in United States. It is maintained by Bloomberg.

Bloomberg U.S. Corporate Investment Grade Index is an unmanaged index consisting of publicly issued U.S. Corporate and specified foreign debentures and secured notes that are rated investment grade (Baa3/BBB-or higher) by at least two ratings agencies, have at least one year to final maturity and have at least $250 million par amount outstanding.

Bloomberg U.S. Corporate High Yield Index is an unmanaged index that covers the US dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market.

The MSCI EMU (European Monetary Union) Index is an unmanaged index considered representative of the EMU group of countries.

The S&P/ASX 200 Index tracks the performance of 200 large companies based in Australia.

The trademarks, service marks and copyrights related to the Russell Indexes and other materials as noted are the property of their respective owners. The Russell logo is a trademark and service mark of Russell Investments.

Copyright © Russell Investments 2016. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an ‘as is’ basis without warranty.

Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide and is part of London Stock Exchange Group.

2016 Annual Outlook

UNI-10682