United States: Life after liftoff

The Fed has consistently communicated an intention to hike rates gradually. But the exact meaning of “gradualism” is open to interpretation. Our favoured scenario predicts continued moderate 2.0-2.5% real GDP growth and a tighter labour market that helps drive inflation higher. In such an environment, we think the Fed would feel comfortable hiking four times in 2016 (i.e. at every other meeting). Indeed, that would be the most gradual hiking cycle in the modern era of U.S. monetary policy. However, it could be perceived as aggressive relative to current market valuation, which appears to be pricing in only two hikes in 2016.

On a standalone basis, the U.S. appears resilient enough to weather higher interest rates. But the impact of further dollar strength – on both the U.S. and other global markets – could stay the Fed’s hand. Fed liftoff is a signal of a more robust expansion, but that isn’t to say that U.S. financial markets are without risk.

Years of asset purchases and ultra-accommodative monetary policy have pulled market returns forward. As a result the U.S. equity market is now fully priced at 17 times forward earnings, based on the S&P 500® as of Dec. 11, 2015. Expensive valuations act as a headwind to the market, and further upside in 2016 will hinge increasingly on corporate earnings power. Our baseline forecast calls for low to mid-single-digit U.S. earnings growth in 2016 as the large drags from the energy and materials sectors fade. But, in our view, the risks to earnings are still skewed modestly to the downside. In particular, we anticipate the unemployment rate will fall to 4.5% (or lower) by the end of 2016, and that could trigger upward pressure on wages, which would eat into profit margins.

The good news is that we do not see a recession on the horizon for 2016. The U.S. Business Cycle Index supports that view. And more fundamentally, we do not observe the types of economic imbalances today that would typically drive a recession. The labour market is nearly back to normal, but it isn’t overheating; business investment remains below trend (and well below the worrying levels of the late 1990s); and household balance sheets are much healthier than they were in the run-up to the financial crisis. The corporate credit cycle, however, is moving into the later innings. For the time being this does not appear to be a systemic risk, as low interest rates make it easy for businesses to service their debt. But corporate credit will be a watch point for investors in the years to come.

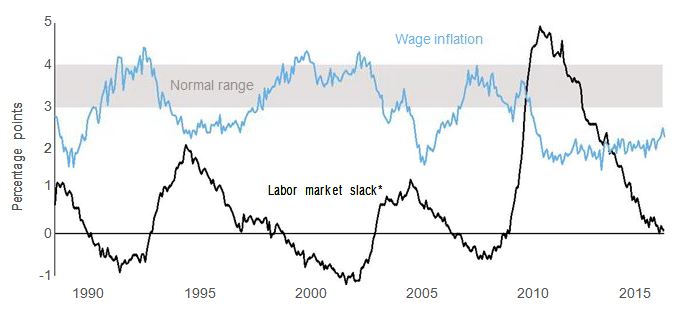

A tightening labour market poses upside to wages and downside to earnings

Percentage-point deviation of unemployment from its normal level

*labour market slack is when there are more workers than jobs

Sources: Bureau of labour Statistics, Russell Investments as of Nov. 30, 2015

Investment outlook

We maintain our underweight to the United States equity market in global portfolios as expensive valuations offset a modestly favourable macro backdrop.

- Monetary policy: We expect the Fed to hike interest rates four times in 2016 and for that to drive further upside in the U.S. dollar and push the 10-year U.S. Treasury yield towards 2.8% by the end of 2016.

- Stronger dollar: We expect the dollar to appreciate by another 5% to 10% in 2016 on a trade-weighted basis, driven by policy divergence between the U.S. and other major central banks. A stronger dollar is a drag on multinationals’ profits, and our dollar estimates subtract roughly one to two percentage points from the corporate earnings growth outlook in 2016.

- Corporate earnings growth: Excluding energy and materials, U.S. trailing earnings growth estimates remain decent, at roughly 5%. However, earnings expectations for 2016 (+8%) remain somewhat elevated relative to our forecast for mid-single-digits. A tighter labour market and peak profit margins pose a risk and we expect earnings expectations to be downgraded as the year progresses.

Strategy outlook

- Valuation: U.S. equities remain quite expensive, which is a headwind to future market performance.

- Business Cycle: We expect the U.S. economy to continue to grow at an above-trend pace in 2016. Fed policy is tightening, but still accommodative in an absolute sense. The economy should be able to chug along with little risk of recession in 2016.

- Sentiment: Equity sentiment is slightly positive but fading back to neutral. Our short- and medium-term oversold signals have faded since the August selloff.

- Conclusion: We continue to have a modest underweight preference for U.S. equities in global portfolios with our earnings outlook supporting a low- to mid-single-digit total return expectation in 2016. Volatility in U.S. equities and rates should remain somewhat elevated into March when the Fed potentially will provide investors with further clarity on the pace of its hiking cycle.

IMPORTANT INFORMATION

Issued by Russell Investment Management Ltd ABN 53 068 338 974, AFS License 247185 ("RIM"). This document provides general information only and has not been prepared having regard to your objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation or needs. This information has been compiled from sources believed reliable, but is not guaranteed. Past performance is not a reliable indicator of future performance. Copyright © 2016 Russell Investments. All rights reserved. This material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from Russell Investments.

The views in this Annual Outlook are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Keep in mind, like all investing, that multi-asset investing does not assure a profit or protect against loss.

No model or group of models can offer a precise estimate of future returns available from capital markets. We remain cautious that rational analytical techniques cannot predict extremes in financial behavior, such as periods of financial euphoria or investor panic. Our models rest on the assumptions of normal and rational financial behavior. Forecasting models are inherently uncertain, subject to change at any time based on a variety of factors and can be inaccurate. Russell believes that the utility of this information is highest in evaluating the relative relationships of various components of a globally diversified portfolio. As such, the models may offer insights into the prudence of over or under weighting those components from time to time or under periods of extreme dislocation. The models are explicitly not intended as market timing signals.

The Business Cycle Index (BCI) forecasts the strength of economic expansion or recession in the coming months, along with forecasts for other prominent economic measures. Inputs to the model include non-farm payroll, core inflation (without food and energy), the slope of the yield curve, and the yield spreads between Aaa and Baa corporate bonds and between commercial paper and Treasury bills. A different choice of financial and macroeconomic data would affect the resulting business cycle index and forecasts.

Investment in Global, International or Emerging markets may be significantly affected by political or economic conditions and regulatory requirements in a particular country. Investments in non-U.S. markets can involve risks of currency fluctuation, political and economic instability, different accounting standards and foreign taxation. Such securities may be less liquid and more volatile. Investments in emerging or developing markets involve exposure to economic structures that are generally less diverse and mature, and political systems with less stability than in more developed countries.

Currency investing involves risks including fluctuations in currency values, whether the home currency or the foreign currency. They can either enhance or reduce the returns associated with foreign investments.

Investments in non-U.S. markets can involve risks of currency fluctuation, political and economic instability, different accounting standards and foreign taxation.

Bond investors should carefully consider risks such as interest rate, credit, default and duration risks. Greater risk, such as increased volatility, limited liquidity, prepayment, non-payment and increased default risk, is inherent in portfolios that invest in high yield (“junk”) bonds or mortgage-backed securities, especially mortgage-backed securities with exposure to sub-prime mortgages. Generally, when interest rates rise, prices of fixed income securities fall. Interest rates in the United States are at, or near, historic lows, which may increase a Fund’s exposure to risks associated with rising rates. Investment in non-U.S. and emerging market securities is subject to the risk of currency fluctuations and to economic and political risks associated with such foreign countries.

The S&P 500, or the Standard & Poor’s 500, is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

The Russell Eurozone Index measures the performance of the equity markets located in the Euro Zone, based on all investable equity securities in the region.

The Bloomberg U.S. Aggregate Bond Index is a broad based index often used to represent investment grade bonds being traded in United States. It is maintained by Bloomberg.

Bloomberg U.S. Corporate Investment Grade Index is an unmanaged index consisting of publicly issued U.S. Corporate and specified foreign debentures and secured notes that are rated investment grade (Baa3/BBB-or higher) by at least two ratings agencies, have at least one year to final maturity and have at least $250 million par amount outstanding.

Bloomberg U.S. Corporate High Yield Index is an unmanaged index that covers the US dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market.

The MSCI EMU (European Monetary Union) Index is an unmanaged index considered representative of the EMU group of countries.

The S&P/ASX 200 Index tracks the performance of 200 large companies based in Australia.

The trademarks, service marks and copyrights related to the Russell Indexes and other materials as noted are the property of their respective owners. The Russell logo is a trademark and service mark of Russell Investments.

Copyright © Russell Investments 2016. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an ‘as is’ basis without warranty.

Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide and is part of London Stock Exchange Group.

2016 Annual Outlook

UNI-10682