Multi-Factor Solutions

Cost-effective, actively managed solutions

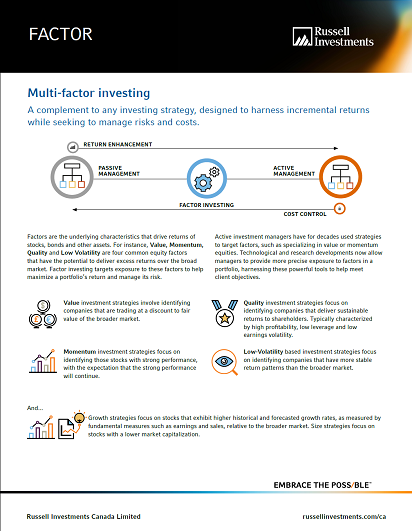

Multi-factor investing is a complement to any investing strategy, designed to harness incremental returns while seeking to manage risks and costs.

Factors are the underlying characteristics that drive returns of stocks, bonds and other assets. For instance, Value, Momentum, Quality and Low Volatility are four common equity factors that have the potential to deliver excess returns over the broad market. Factor investing targets exposure to these factors to help maximize a portfolio’s return and manage its risk.

Factors

![]()

Value investment strategies involve identifying companies that are trading at a discount to fair value of the broader market.

![]()

Quality investment strategies focus on identifying companies that deliver sustainable returns to shareholders. Typically characterized by high profitability, low leverage and low earnings volatility.

![]()

Momentum investment strategies focus on identifying those stocks with strong performance, with the expectation that the strong performance will continue.

![]()

Low-Volatility based investment strategies focus on identifying companies that have more stable return patterns than the broader market.

![]()

Growth strategies focus on stocks that exhibit higher historical and forecasted growth rates, as measured by fundamental measures such as earnings and sales, relative to the broader market. Size strategies focus on stocks with a lower market capitalization.

Our factor investing approach

At Russell Investments1, we understand factor investing—it’s been one of our core capabilities for more than 40 years. We believe there are three key components to a successful multi-factor strategy:

Dynamically-managed factor exposures based on market cycle

Russell Investments (RI) does not believe in a return premium to the Growth factor through the entire cycle, so it is not included in our ‘strategic factors’ above. However, RI believes there are appropriate times to allocate to Growth within certain phases of the cycle as a valuable analogue to allocations to the Value factor. RI does not believe in a premium to smaller size, but does believe that active management, and factor exposures, are more powerful in smaller cap stocks.

Russell Investments’ Multi-Factor Solutions

At Russell Investments we actively manage across multiple factors with the aim of generating incremental returns while managing overall risk.

Discover our four cost-effective, actively managed multi-factor solutions: