Key Takeaways:

- Venture capital markets is at an attractive entry point for long term investors.

- Demand remains strong, driven by transformative trends in AI, climate tech, and fintech.

- Manager selection is critical, with performance dispersion reinforcing the need for access to top-tier managers.

Venture capital (VC) markets have reset. Capital has reduced, competition has faded, and the next wave of innovation is accelerating. We believe today’s environment offers a particularly attractive entry point, provided investors take a patient, long term approach and focus on accessing the right managers in the asset class.

Cyclical Headache

VC has historically offered compelling return potential. As a subset of private equity, VC stands out for its higher risk/return profile and its ability to access innovation-driven value creation. However, some investors have been warded off due to the market’s inherent cyclicality.

Throughout the history of the VC industry, there have been multiple instances where overexuberance has spurred an influx of capital, leading to artificially high valuations and eventual market correction. Trying to time the market is extremely difficult and we advocate for investors to make steady, consistent commitments annually, allowing for greater vintage year diversification.

Why Invest Now?

Companies are staying private longer, now averaging 10.7 years before going public, up from 6.9 a decade ago.1 This shift, driven by regulatory burdens and ample private capital, means more value is created before initial public offering (IPO), making private markets essential for accessing early-stage growth companies.

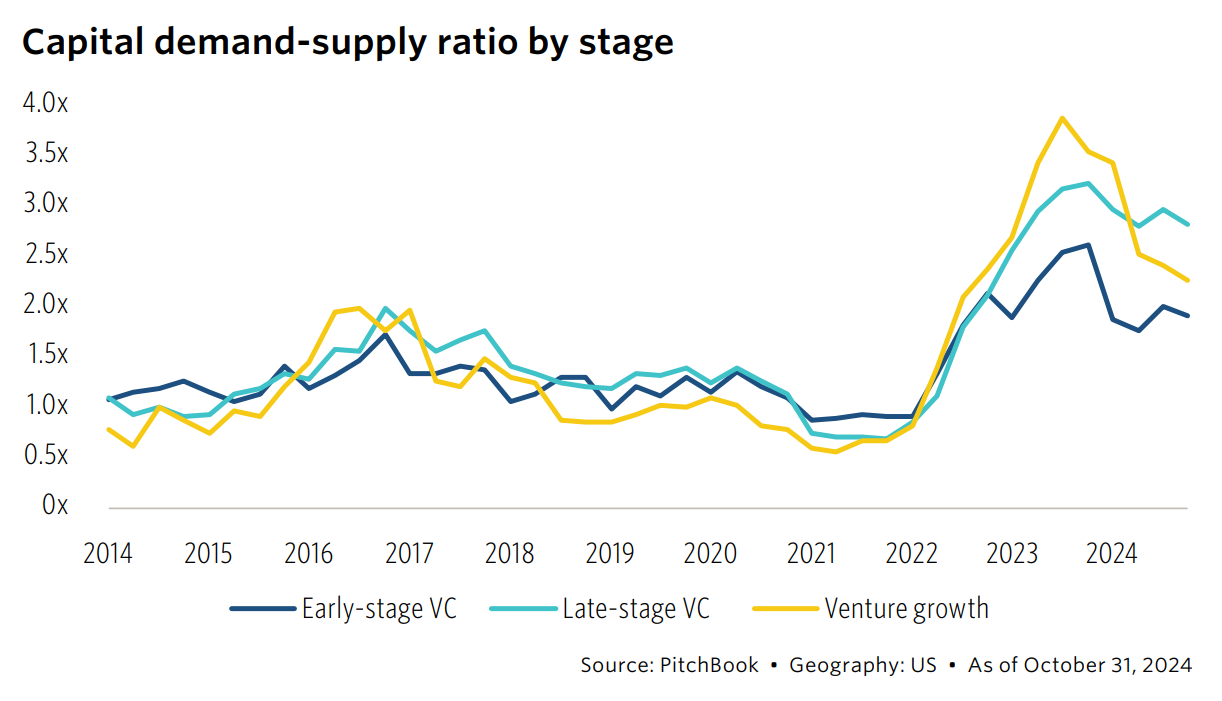

Additionally, we believe there’s an imbalance between the supply and demand for capital compared to much of the last decade. According to Pitchbook, the ratio of demand to supply for VC funding spiked in 2023 and remains elevated relative to much of the 2010s and early 2020s, suggesting that supply-side scarcity could support valuations going forward.

VC Demand Remains Resilient

Market Reset

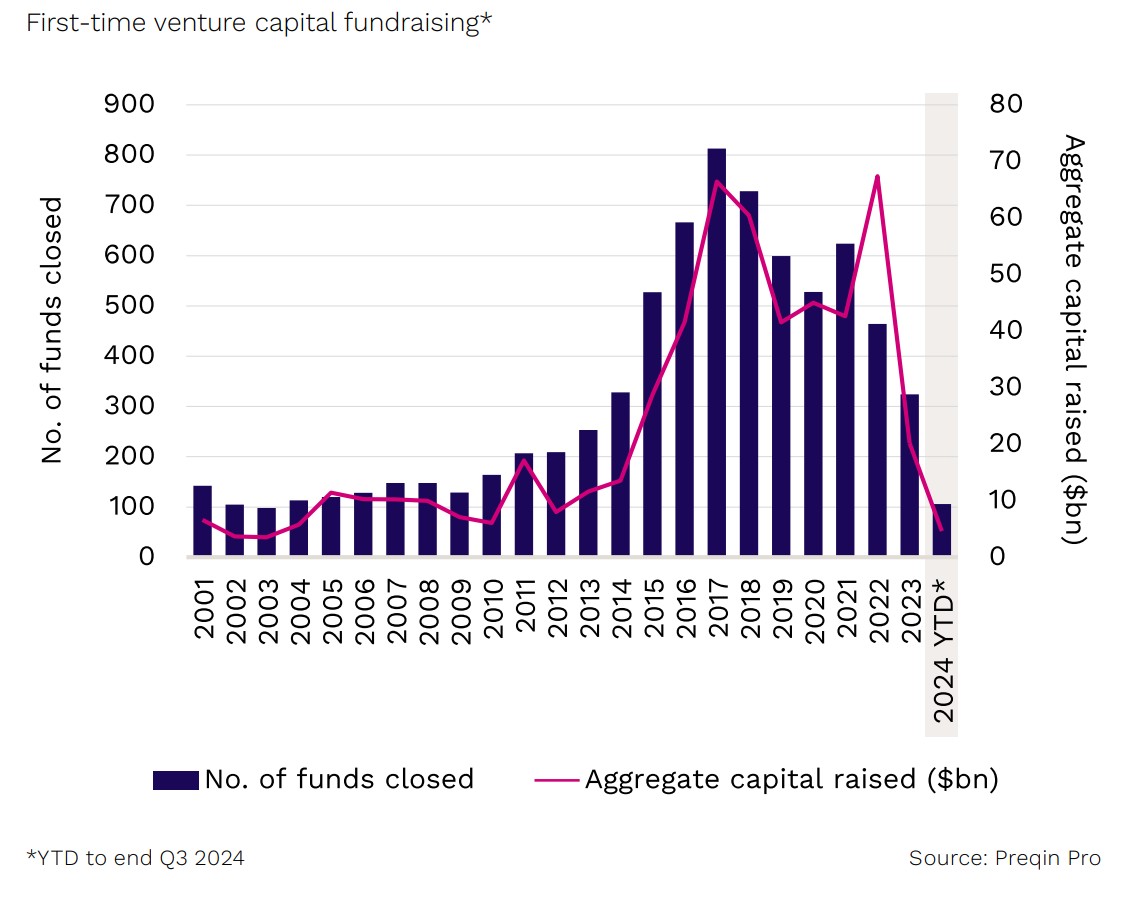

The reason? The slowdown in both M&A and IPO activity in recent years has caused distributions from VC funds to dry up since 2021. This has created a liquidity crunch for investors, preventing them from recycling capital into newer vintages. As a result, many GPs have struggled with fundraising, suppressing the amount of capital available for new deals.

Fundraising Drop Off

Furthermore, after experiencing somewhat of a reset in valuations since 2021, we’ve seen many non-traditional VC investors, including crossover funds and corporate VCs, exit the industry. This is a meaningful change from 2021 when approximately 60% of investment rounds were led by a crossover fund or hedge fund. Meanwhile, deal activity by corporate VCs has continued to trend downward for the last three years.2

Growth Trends

Despite the supply of capital having trended down in recent years, we expect several new innovations to drive higher demand for VC funding.

Artificial Intelligence (AI): We see AI as having the potential to reshape business models, with generative AI streamlining content creation and reducing costs. Sector-specific applications are emerging rapidly, including enhanced diagnostics and personalized care in healthcare, real-time threat detection in cybersecurity, and fraud prevention, risk management and customization in financial services.

Climate Tech: To achieve targeted carbon emission reductions, VC funding will be needed for the development of clean energy solutions, carbon capture technology and advancements in sustainable agriculture.

Fintech: We also believe the integration of blockchain technology, the growth of digital banking and payment solutions represent key VC opportunities.

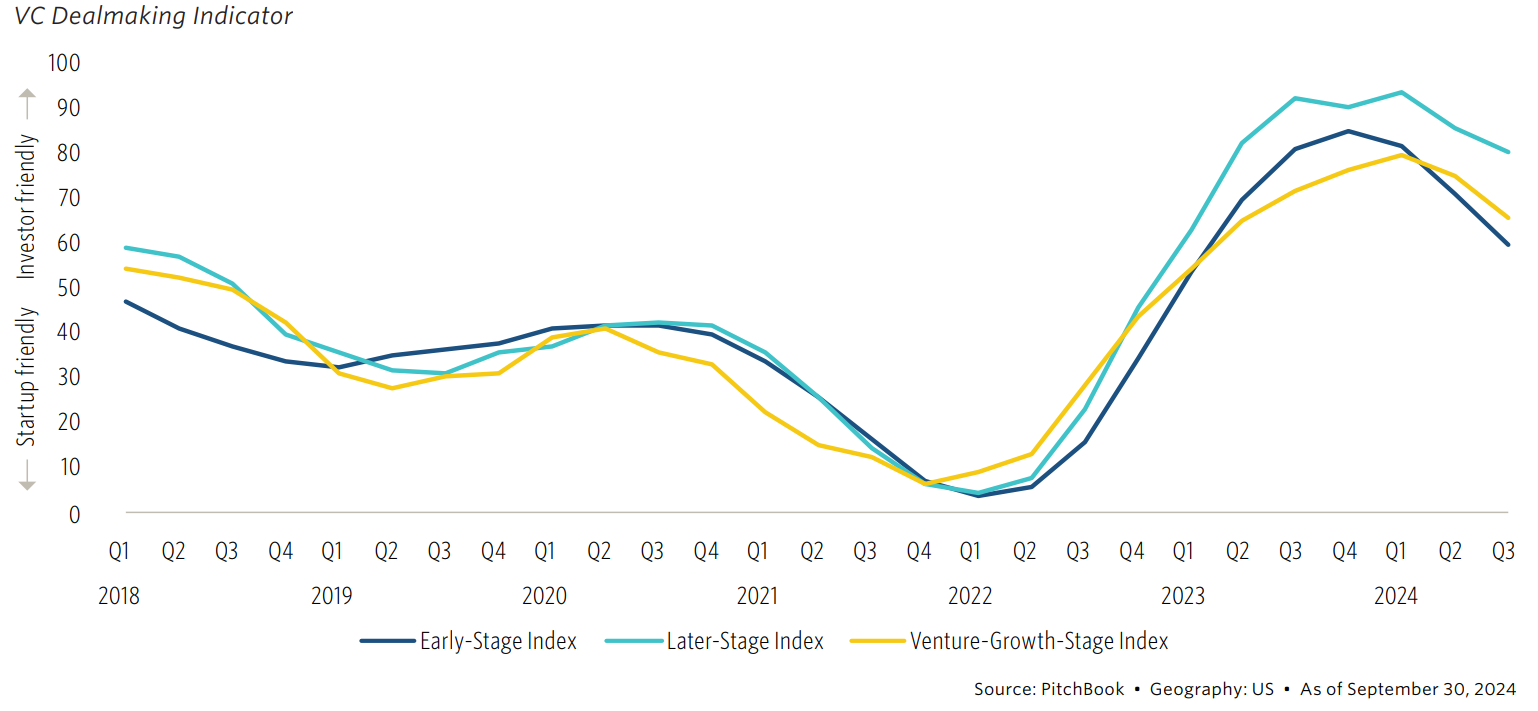

Given these trends, we expect that the demand for capital relative to the available supply should remain favorable for investors for the foreseeable future. Since this shift began in 2022, we’ve seen it manifest in more favorable deal terms for VCs, in both price and deal structure. This can be seen in Pitchbook’s VC Dealmaking Indicator, which shows the current market environment to be more investor-friendly than we’ve seen in recent years.

Dealmaking Resurgence

Finding the Right Manager

A key factor in VC investing is manager selection. Outcomes in the asset class can vary widely and the top quartile performance is often based on a manager’s ability to source and attract top entrepreneurs. Therefore, the spread between the best and worst performing tends to be greater than in other asset classes and top managers are often over-subscribed and difficult to access. For less experienced investors, partnering with well-connected, research-driven firms is key to optimizing results.

Ultimately, we believe VC investing will reward patience and discipline. Market cyclicality, extended private company lifecycles, and rapid innovation are characteristics that demand a long term, strategic investment approach that’s often best executed by top-tier managers.

In today’s reset environment, with lower valuations and capital supply constrained, there’s rarely been a better investor entry point to the market.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 Source: Morningstar. Unicorns and the Growth of Private Markets. June 24, 2024.

2 Source: Andreessen Horowitz