Key takeaways:

- Views are split on recent developments in inflation and labour market data

- Labour market data supports the case for easing, while stubborn inflation jeopardises the Bank’s inflation target

- For markets, what could be more important for long-term yields is the upcoming quantitative tightening decision in September.

In a narrowly split 5-4 vote, the Bank of England Monetary Policy Committee (MPC) trimmed the bank rate by 0.25% to 4%, representing a fifth straight cut and fall to the lowest level since March 2023.

Five members, including Governor Andrew Bailey, backed the cut while four members (Green, Lombardelli, Mann and Pill) voted to hold interest rates steady. In a dramatic twist, Alan Taylor had preferred a 0.5% cut but sided with 25 basis point camp to secure a majority decision.

Unexpectedly Hawkish

The vote was more hawkish than analysts had predicted. Prior to the meeting, observers had expected only two to three MPC members to go for unchanged rates and two members to opt for a more aggressive 50 basis point reduction.

The wafer-thin majority reflects a stark contrast in how policymakers are interpreting recent developments in inflation and labour market data since its May meeting.

What's Changed?

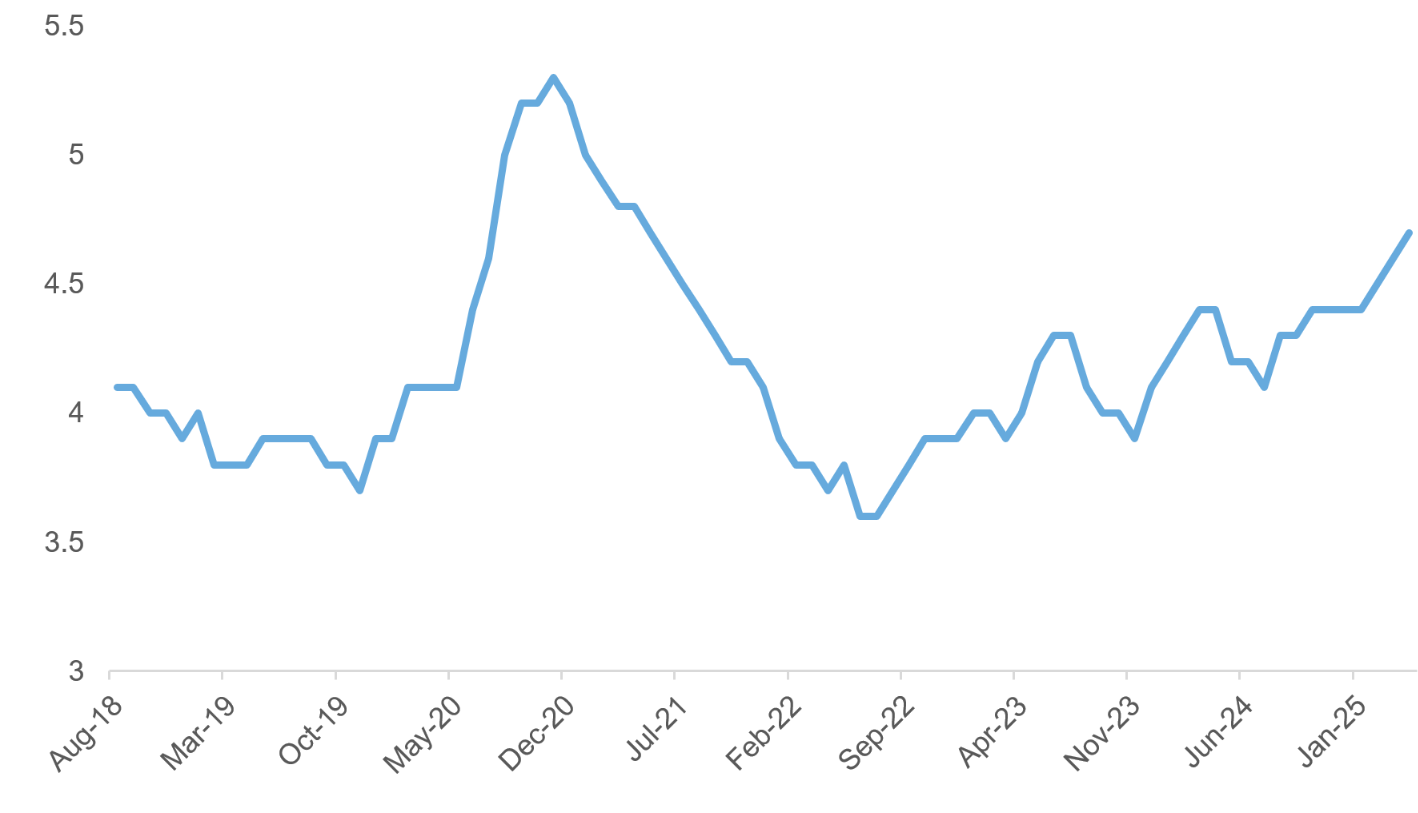

The labour market has weakened more than central bankers expected. Unemployment rose to 4.7% in the three months to May, marginally above the MPC’s forecast. Payrolls have fallen for eight consecutive months, and the vacancy-to-unemployment ratio has dropped below the Bank’s estimate of equilibrium, suggesting a meaningful rise in labour market slack.

Crucially, wage growth—an essential input for domestic inflation pressure—has slowed more than anticipated. Private sector regular pay growth was 4.9% year-on-year in the three months to May, below Bank staff forecasts made at the last MPR.

More Pink Slips

UK Unemployment Rate

Source: LSEG Datastream

Inflation Worries

Meanwhile, inflation has surprised to the upside. Headline CPI for June printed 3.6%, above the Bank’s projection, with food and services inflation being the primary culprits.

Core and services inflation remain frustratingly stubborn. Inflation is set to peak around 4% over the next few months and, worryingly, medium-term inflation expectations have moved higher.

The four MPC members who voted to hold rates cited elevated business and household inflation expectations. They pointed to firms’ continued willingness to pass on cost increases, indicating that structural pressures in labour and goods markets could entrench inflation. In their view, a slower pace of easing would better safeguard the return to target.

This leaves the committee in a bind. On the one hand, the labour market data supports the case for continued easing. On the other, stubborn inflation—particularly in services—raises concerns about second-round effects that could jeopardise the Bank’s ability to return inflation to target.

Market Reaction

The narrow vote was a hawkish surprise for markets. As of 4 p.m. UK time, Gilt yields rose across the curve, with two-year yields up 5 basis points from yesterday’s close and 10-year yields 2 basis points higher. The pound rose by 0.3% against the U.S. dollar and 0.6% against the euro.

Today’s rate cut offers modest relief to mortgage borrowers with a tracker product, which will see rates fall immediately. Borrowers looking at fixed-rate mortgages will be disappointed by the increase in yields.

The slim majority for today’s rate reduction and the Bank’s cautious guidance on further easing signals that a return to pre-2022 levels of borrowing costs is unlikely. Homeowners coming off fixed-rate deals will still face significantly higher rates than they did four to five years ago.

What's Next?

While the Bank’s close call is grabbing attention today, the decision on quantitative tightening coming up in September may have greater significance for long-term yields.

With fewer gilt redemptions in 2025–26, maintaining the current £100 billion per year pace at which the Bank shrinks its balance sheet would require record levels of active sales.

If the latter are concentrated in long-dated bonds, it could lead to a further rise in long-term yields. A slower pace—potentially £70–75 billion—would ease pressure and reduce volatility in the long-dated gilt market. Pension funds will look to tightening as a more important factor for the path of long-term interest rates.

The Bottom Line

The split within the MPC reflects a tough trade-off between the rapidly cooling UK labour market and sticky inflation. However, when it comes to pension schemes, what could be more important for long-term yields is the upcoming quantitative tightening decision in September. If this MPC outcome is any guide, more difficult decisions are coming soon.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.