Key takeaways

Rapid gilt yield rises show how quickly market expectations can shift.

Fast moves are testing liquidity and collateral resilience in defined benefit (DB) schemes.

Strong cashflow planning and governance are key to staying aligned with long-term objectives in volatile markets.

Markets don’t need to break to feel uncomfortable, they just need to move fast enough.

The recent move in gilt markets has reflected this concern. While not a repeat of the 2022 mini-budget crisis, price movements have been substantial enough to raise eyebrows across pension schemes.

Sharp moves in gilt markets

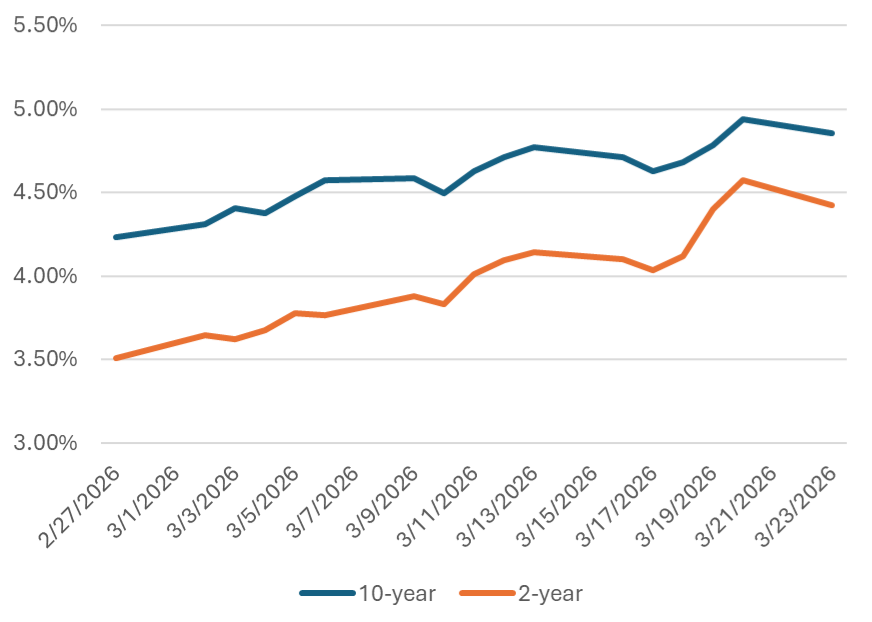

Since 27 February, UK gilt yields have risen sharply. Two-year yields moved from around 3.5% to c.4.5%, an increase of roughly 100 bps. At the long end, 10-year yields reached around 4.9%, up close to 70 bps over the same period and briefly touching their highest levels since 2008.

Gilt yields rise

Source: Market Watch, 23 March 2026

Recent geopolitical developments and uncertainty around the Iran conflict have brought yields back towards levels seen at their peak over the past 12 months; the highest in 25 to 30 years.

As highlighted in media coverage, this reflects a rapid shift in market expectations. Only weeks ago, the focus was on Bank of England rate cuts. Markets have since reassessed the inflation outlook, particularly in light of higher energy prices, and are now questioning whether the next move could be a hike.

Implications for DB pension schemes

For DB schemes, the impact is technically complex and highly dependent on structure. Here are factors we consider important to schemes:

1. LDI and liquidity

Higher yields reduce liability values. However, where interest rate and inflation risks are hedged, asset values will also have declined. Funding outcomes therefore depend on hedge ratios and execution.

The more important issue has been the path of the move. Rapid rise in gilt yields places pressure on collateral buffers and liquidity waterfalls, particularly for schemes with tighter headroom. This has not led to the forced selling seen in 2022, but it is a reminder of how quickly liquidity can become the binding constraint.

2. CDI and cashflow resilience

Cashflow matching and cashflow driven investments (CDI) strategies come into focus in this environment. Schemes with well-structured income portfolios are better positioned to meet benefit payments without needing to sell assets at stressed levels. Avoiding forced asset sales in volatile markets can be as important as managing funding levels.

3. Valuations and timing

With many schemes approaching March valuation dates, moves of this magnitude can influence funding outcomes and technical provisions. How post-valuation experience is treated may become more relevant, particularly if volatility persists.

At the same time, growth portfolios have come under pressure from both equity weakness and rising yields, with diversification offering limited support.

Endgame implications

This environment also puts current discussions around endgame options into context. Strong governance is key to ensuring that schemes’ endgame objectives are protected, and that investment strategies not only align with those objectives but can evolve as market conditions change.

It is also a reminder for schemes running on that periods of market volatility can still impact funding positions. Ensuring that the level of risk remains appropriate to the desired outcomes, supported by a robust sponsor covenant and clear guardrails, is critical.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.