Are we oversimplifying sustainable investing?

Sustainable investing is often viewed through a narrow lens. For some, it represents impact. For others, it means thematic exposure or simple exclusions. Increasingly, it is also associated with constraint and the belief that sustainable strategies sacrifice flexibility, diversification or returns.

Yet the reality is far more nuanced.

Beneath the headlines, our research shows the sustainable equity universe to be diverse and dynamic, shaped by multiple drivers of risk and return rather than a single defining characteristic.

Three observations on sustainable equities

1. Sustainable equity strategies are not homogeneous and are not higher risk quality growth versions of traditional portfolios

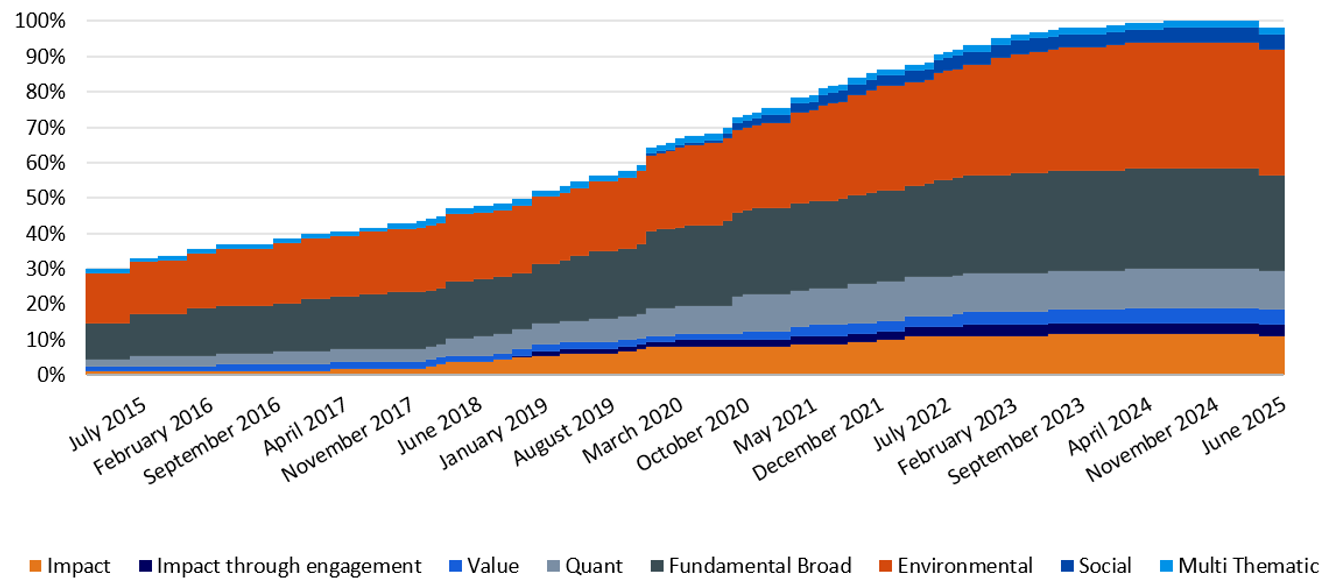

There is still a prevalent idea that sustainable investing is associated with Growth and Quality biases, and while this holds true at the aggregate level, it fails to recognise the significant diversity that exists among the strategies.

The sustainable equity universe now spans beyond Growth or Thematic strategies. Value and Quant strategies make up more than 15% of the overall opportunity set. These come with distinct style, sector or regional exposures.

The diversity in strategies also creates opportunities. With intelligent portfolio design, investors can actively manage style and factor biases, reduce unintended concentration risks and build more balanced exposure profiles.

Different strategies, different biases

Evolution of sustainable equity universe composition over time

Source: Russell Investments, as of 30 June 2025.

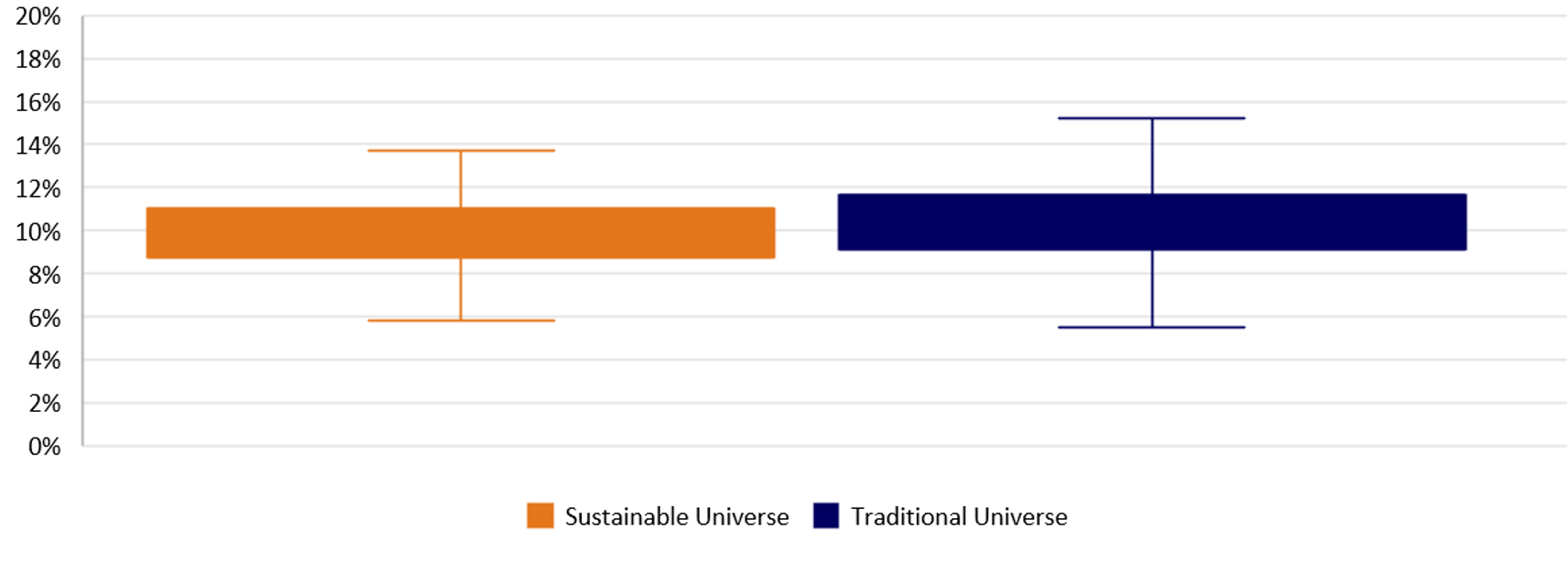

2. Long-term performance remains competitive

While performance across sustainable investing over the last 5-years has been challenging, this can largely be attributed to market headwinds. Over the long-term returns remain competitive relative to traditional peers, challenging the notion that sustainability objectives inherently detract from returns.

Competitive performance

Spread of product 10Yrs annualised returns

Source: Russell Investments, as of 30 June 2025.

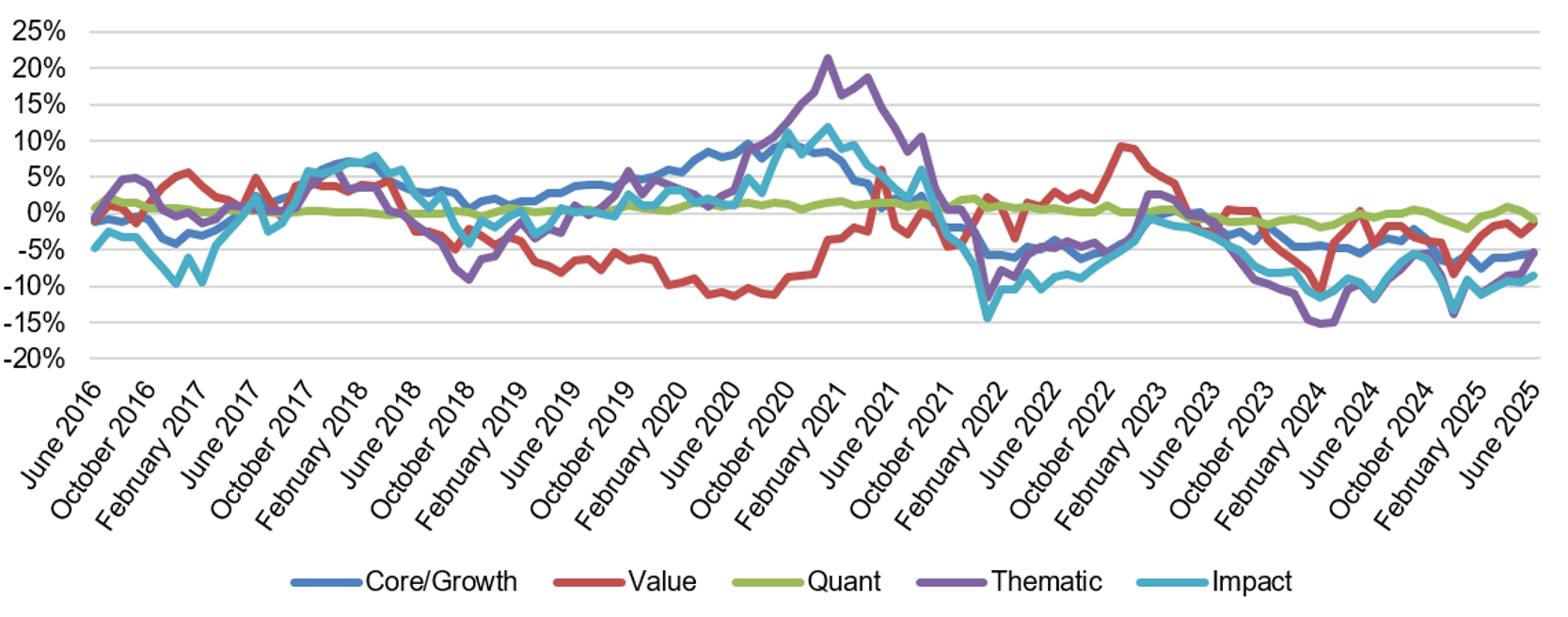

Recent underperformance can largely be explained by a market environment that favoured exposures typically underrepresented in sustainable portfolios, notably U.S. mega cap growth, Value and Energy. These dynamics reflect cyclical factor rotations rather than structural shortcomings.

Importantly, some of these cyclical headwinds can be mitigated by using a multi-manager approach.

Performance varies meaningfully within the sustainable equity universe

Median 1 year rolling annualised arithmetic excess returns, relative to MSCI World Index

Source: Russell investments, as of 30 June 2025.

3. As with any active allocation, manager skill matters

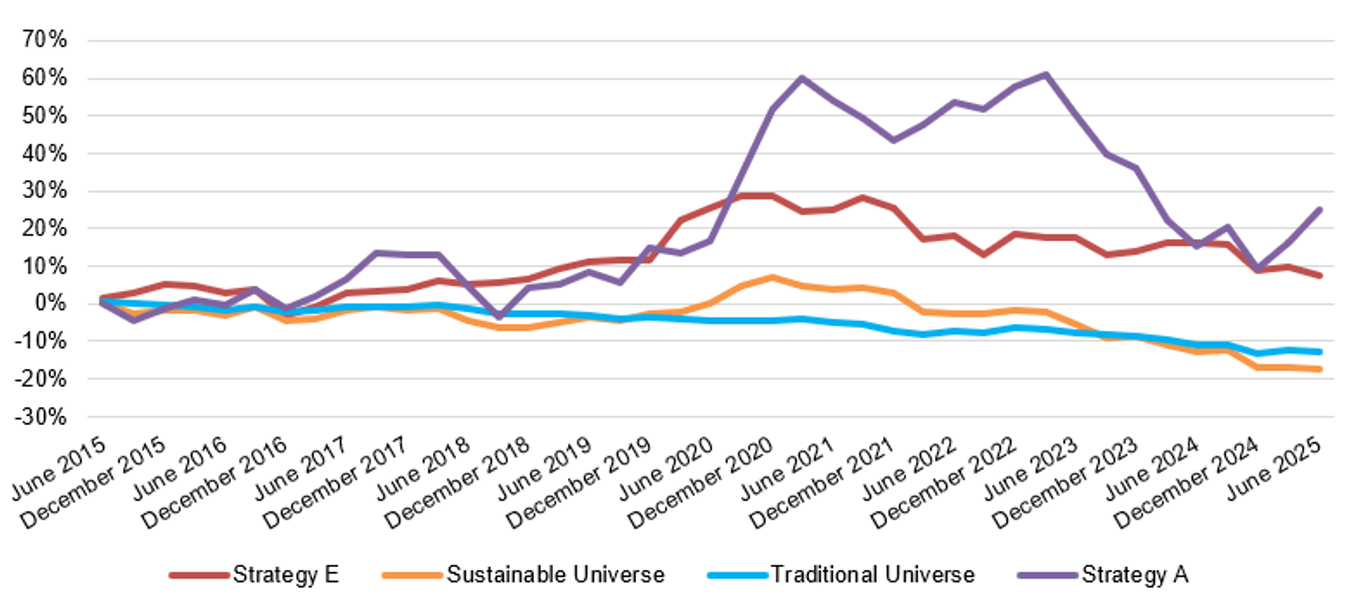

Performance dispersion across sustainable equity managers is wide and cannot only be attributed solely to differences in investment approaches, indicating variation in manager skill and capability.

The strongest long-term performers tend to share common characteristics, including experienced and stable teams, a consistent and authentic commitment to sustainability, robust fundamental research processes and disciplined portfolio construction.

Manager skill matters

Cumulative active returns of two top-performing sustainable equity strategies (strategies A & E) versus the median traditional and sustainable managers (2015–2025)

Note: Returns are presented as geometric cumulative active returns relative to the MSCI World Index from 2015–2025. The exhibit shows two of the top-performing strategies within the sustainable equity universe alongside the median manager in both the traditional and sustainable universes. Strategy names have been anonymised in line with the methodology used in the whitepaper. Source: Russell Investments, as of 30 June 2025.

Investor implications

These insights reinforce a broader point. Sustainable investing is not a narrow opportunity set, but a broad universe of strategies that can help a wide range of investors meet both their sustainability and return objectives.

Sound portfolio construction and manager selection are central to investing in the segment, blending multiple manager approaches and strategies to address potential sector biases and smoothen the investor journey.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.