The Investment Association’s buy-side overview highlights that FX trading through a dedicated trader and specialist currency manager can deliver more competitive rates, greater access to liquidity sources which can support best execution. In contrast, while custodian-instructed FX may seem simpler, it may not produce optimal execution when compared to sourcing liquidity from multiple venues. Under T+1, that trade-off becomes harder to ignore and what seems simplest on the surface might not lead to best outcomes for investors.

Key takeaways

- While the United States and a select few countries have already made the move, the UK, Switzerland, and the rest of Europe are set to transition to T+1 settlement in October 2027.

- For asset managers and asset owners not yet operating in a T+1 environment, this will be a significant change in workflow due to the loss of operating time between security trades and settlement.

- For the transition, FX is still likely to be one of the main pressure points. The FX aspect of any security trade may need expediting under T+1, with Europe’s multi-jurisdiction operational environment making cut-offs and post trade coordination even more complex.

- Regardless of if teams are already managing T+1 as part of their current workflow, the October 2027 transition makes it an opportune time to revisit managers, custodians, settlement agents and FX providers to decide whether each part of the workflow is still fit for purpose.

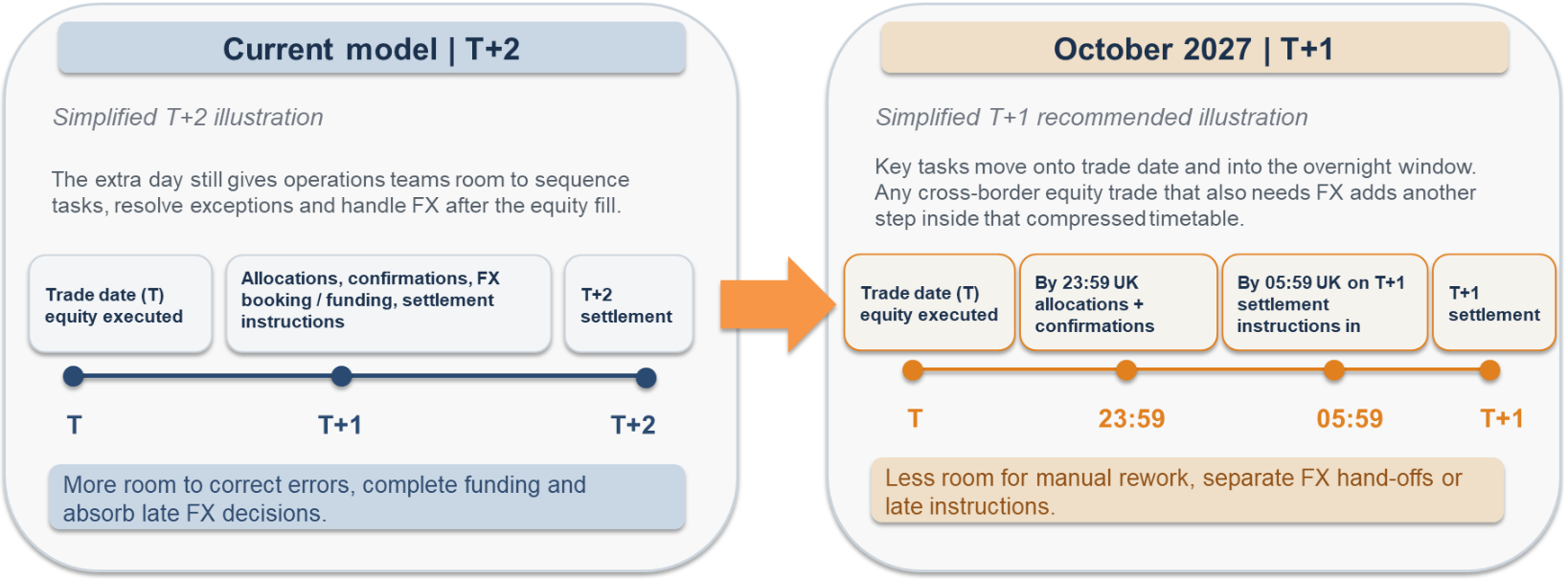

While the move to T+1 is often described as a market-structure reform, for asset managers and asset owners, it becomes a true litmus test of current operating-models. The Investment Association, the UK Asset Management industry body, notes that the available post-trade processing window can shrink by about 83% as markets move from T+2 to T+1.

This means that preparation for the T+1 switch is crucial and we see some distinct sets of questions that every asset manager and asset owner should ask.

FX questions every asset manager should ask

This is where the impact of T+1 becomes immediately clear. According to the UK’s Accelerated Settlement Taskforce, T+1 allocation and confirmation processing should be completed on trade date by 23:59 UK time, and settlement instructions should be submitted no later than 05:59 on T+1. The Financial Conduct Authority, the UK’s financial regulator, (FCA), is also clear that firms should be addressing manual bottlenecks now, not treating them as a permanent solution. For those asset managers still expecting to manage this in-house, this creates considerable time constraints and adding any FX requirements increases this pressure significantly.

The FCA expects firms to carry out end-to-end reviews of trading, clearing and settlement arrangements, speak with settlement agents about earlier cut-offs and remember that outsourcing does not remove accountability. For asset managers, that means testing whether current providers, or current in-house models, can actually support a shorter cycle, not just whether they worked under T+2. The move to T+1 is coming and the FCA is expected to take a more active role in ensuring firms are ready.

FX questions every asset owner should ask

Different managers will handle FX timing, liquidity sourcing and exceptions differently. In a T+1 environment, those differences become harder to absorb. For asset owners, the oversight question is not just price; it is whether the operating model is consistent enough to support timely settlement across the FX workflow chain. The move to T+1 provides asset owners the opportunity to ensure this FX trading workflow is working as efficient as possible, and delivering the trading results expected.

The FCA has highlighted the industry recommendation that many funds should continue to settle at T+2 even where underlying securities move to T+1, in order to preserve cash-management flexibility and reduce funding gaps. For asset owners, that makes fund terms part of the T+1 discussion, not an afterthought. That added complexity adds to the benefit of working with a specialist currency provider, to ensure flexibility can be crucial in the new operating model.

T+1 puts more weight on who owns FX timing, SSI quality, governance, and exception escalation. Where responsibilities are split across managers, custodians and other providers, owners should be clear on who does what, by when, and how issues are surfaced before they become settlement problems. Alignment of interest is crucial and the move to T+1 can be a catalyst to ensure service providers are still fit for purpose. To help with this, using independent transaction cost analysis (TCA) can provide clear and quantifiable evidence to ensure service providers are accountable.

Preparing for T+1: Revisit FX operating models

T+1 can reduce risk and improve market efficiency, but for both asset managers and asset owners, the practical value will be won or lost in the operating model. The firms best placed for 2027 are likely to be the ones that simplify workflows, revisit provider relationships early, and treat FX as part of the same implementation decision as the security trade. This means ensuring that both implicit and explicit costs of FX trading are taken into consideration, ensuring best execution and post-trade transparency remain the focus during the T+1 transition.

Fundamentally, the move to T+1 provides a strong opportunity to revisit alignment of interest and ensure that your providers are providing best execution.

Footnotes

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.