Manager research goes beyond performance data to evaluate how investment decisions are made, whether results are repeatable, and how managers fit within a broader portfolio. Combining quantitative analysis with qualitative insight helps distinguish enduring skill from short-term market outcomes, supporting more informed portfolio construction and manager selection.

Key Takeaways

- Russell Investments' manager research began over 50 years ago with the belief that selecting and combining skilled managers can lead to better portfolio outcomes

- Quantitative and qualitative analysis work together to provide a more complete view of investment managers

- Experience across market cycles is key to identifying consistent manager performance

- AI is expanding the reach of manager research by scaling data analysis, connecting historical insights, and supporting more timely portfolio decisions

As part of our 90-year celebration, we are revisiting manager research. Understanding how the discipline has evolved through changing markets, new technologies, and expanding investment opportunities helps explain why it remains critical today and how it may continue to adapt in the age of AI.

A legacy built on insight and access

Manager research at Russell Investments began with a simple idea that still guides our work today: better portfolio outcomes start with a deeper understanding of how managers think and invest. That idea was put into practice in 1969, when George Russell won the firm’s first consulting client by offering to build a researched list of managers and stand behind it. At the time, many investors relied heavily on a single banking relationship. Russell Investments introduced a more deliberate, structured approach to identifying, evaluating, and combining manager strategies.

From the outset, this work combined data with direct access. Analysts built performance universes to compare individual products offered by managers on a like-for-like basis, laying the groundwork for indices that helped measure portfolios more effectively. Over the decades, this research has expanded to include strategies in a comprehensive set of asset classes, including private markets. While the core of the research methodology remains consistent, it is tailored to each asset class. That evolution has also increased the importance of product and strategy classification, as managers now offer a wide range of products managed by multiple teams within each manager.

Alongside this quantitative foundation, analysts engaged directly with investment teams to understand process, culture, and decision-making. The early discipline was not only about collecting data. It was about listening carefully, asking sharper questions, documenting what mattered, and separating useful insight from manager “fluff.” Quantitative analysis provided structure and consistency; qualitative insight helped build conviction.

Those early practices shaped how portfolios were constructed. Managers were evaluated individually, but selected in combination, with attention to how different investment approaches interacted. The 1980 launch of Russell Investments' first manager-of-managers funds marked an important step in translating research conviction into implementation, packaging selected managers together in portfolios designed around diversification and complementarity. This legacy continues to influence how research translates into portfolio construction today, where combining differentiated sources of return remains central to managing risk.

Our advantage has never been simply having more data. It has been knowing which questions to ask, which signals matter, and how to translate manager insight into portfolio action. That distinction is important. Manager research is not a cataloging exercise; it is an investment discipline built on access, judgment, accountability, and implementation. Russell Investments' formal manager ratings reinforced that research was never meant to be passive commentary. Ratings required conviction, follow-up, and accountability for whether a manager remained worthy of client capital. The value comes from connecting what managers say, what they hold, how they have behaved, and how their strengths can be combined with others to support better portfolio outcomes.

Russell Investments' legacy in manager research also sits alongside its history of improving how investors measure performance, because better manager selection depends on better comparison, clearer benchmarks, and a more disciplined understanding of style. That continuity helps maintain alignment between manager selection and long-term portfolio objectives.

Enduring tenets of manager research

Performance data provides a useful data point, but it does not fully explain how results are generated or whether they are likely to persist. Manager research brings together quantitative analysis, qualitative insight, and experience built over time to close that gap.

Quantitative work provides structure, enabling consistent comparison and defining the opportunity set. Qualitative insight adds depth through direct engagement with investment teams, often with access across the organization, to understand how decisions are made and implemented.

Experience connects the two. Over time and across market environments, repeated interactions allow more subtle distinctions between managers to emerge. It also creates accountability, where manager ratings reflect conviction and are evaluated based on outcomes.

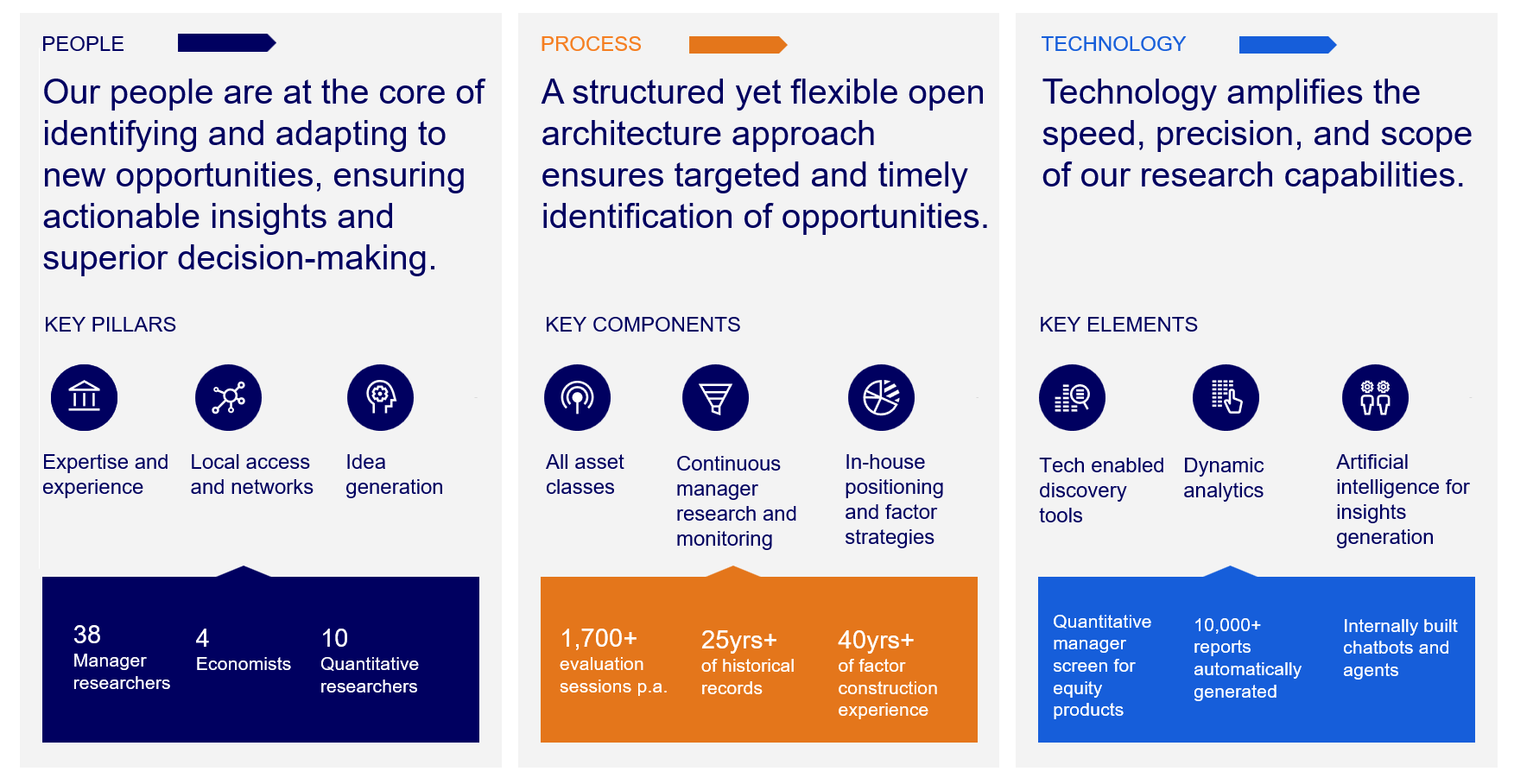

The real test of manager research is not whether it can explain the past, but whether it can improve the next decision. That means identifying whether performance reflects repeatable skill or market noise, understanding when a manager’s edge is changing, and knowing how much confidence to place in that insight when building portfolios. At Russell Investments, the research process is designed to move from observation to conviction to implementation and rests on three interconnected foundations: people, process, and technology.

Three foundations of manager research and monitoring

Source: Russell Investments

Extending research with AI

Today’s manager research operates across a broader and more complex set of inputs. Next to structured data sits a substantial body of unstructured information, including manager reports, portfolio updates, and internal research notes accumulated over decades. Historically, these inputs have been valuable but not always easy to connect at scale.

Recent advances in AI allow that body of work, both quantitative and qualitative, to be used more effectively. This includes summarizing manager materials, identifying patterns across datasets, and linking current observations with historical research. In practice, this connects what we are seeing today with how managers have behaved in different market environments.

AI also supports manager discovery and monitoring. Quantitative tools narrow a large universe, while AI-assisted analysis surfaces signals from unstructured data, highlighting changes in positioning, investment views, or organizational developments. With access to thousands of managers, this helps focus attention where it can add the most value.

These capabilities are integrated into existing workflows, strengthening how research is conducted day to day rather than creating a separate process.

AI changes the scale of the work, but not the ownership of the decision. It can help process more information and surface earlier signals. But the judgment remains human-led. Analysts and portfolio managers still determine what matters, challenge the evidence, and decide how insight should be reflected in portfolios. In that sense, AI is not replacing our manager research discipline. It is helping make that discipline more consistent, more connected, and more responsive.

We continue to apply our multi-manager discipline in new vehicles and formats, using our global research network to identify and combine differentiated strategies for today’s investors.

Looking across 90 years

Manager research has evolved alongside the broader investment landscape, from a hands-on process built on direct interaction to a global capability supported by data and technology. The tools have changed, but the underlying discipline has remained consistent.

What began with building a list of managers has developed into a process that draws on decades of insight and a much broader opportunity set. Today, the role of manager research remains the same: to understand how investment decisions are made, assess whether skill is repeatable, and apply that insight in building portfolios designed to help meet client objectives.

Common client questions

AI expands the scale and speed of manager research by analyzing large volumes of structured and unstructured information, identifying patterns, and connecting current developments with historical insights. Investment professionals remain responsible for evaluating the evidence, challenging conclusions, and determining how research should influence portfolio decisions.

A multi-manager approach seeks to combine managers with complementary investment styles and sources of return rather than relying on a single perspective. Understanding how managers interact within a portfolio can improve diversification, manage concentration risk, and create a more resilient investment strategy across changing market environments.

Performance alone rarely tells the full story. Effective manager research combines quantitative analysis, qualitative assessment, and experience across market cycles to evaluate whether results stem from a repeatable investment process or temporary market conditions, helping investors make more informed allocation decisions.