Executive summary:

- Stronger-than-anticipated economic data released during the first quarter led to a significant downward shift in market expectations for 2024 rate cuts.

- While equity markets were mostly unfazed by this change in expectations, fixed income markets experienced increased levels of volatility during the quarter.

- The exchange rate between the U.S. dollar and the Japanese yen hit a 34-year high.

Markets started the year anticipating several U.S. Federal Reserve (Fed) rate cuts in 2024, but by the end of the first quarter, a continued string of stronger-than-anticipated economic data readings led to a significant dialing-down of expectations.

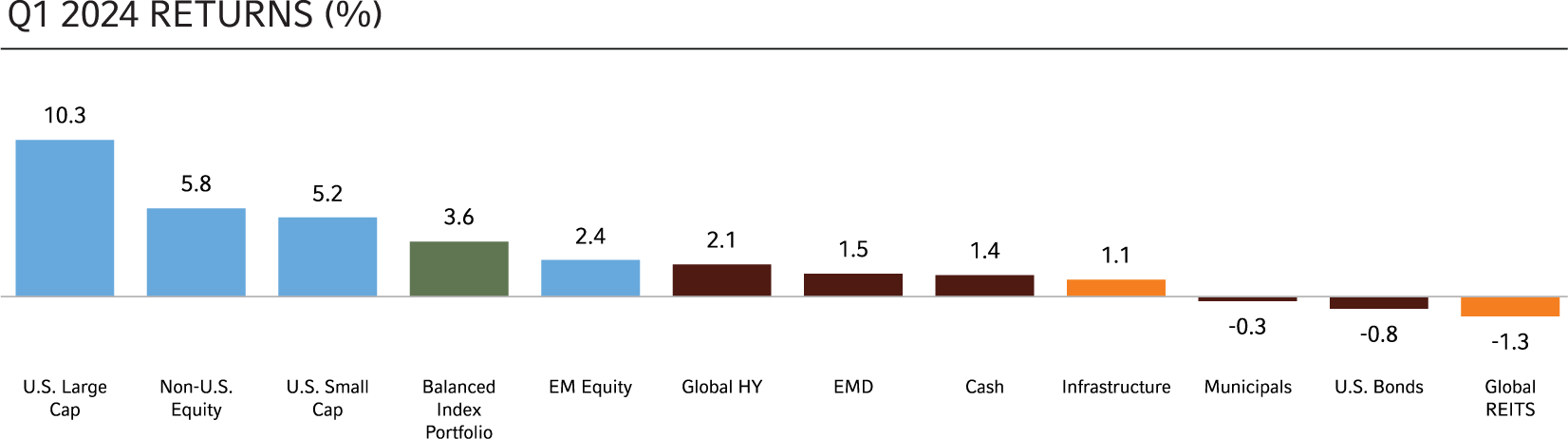

Equity markets were largely unfazed by the shift, generally climbing anywhere from 5% to 10%, depending on the region. It was a different tale in fixed income markets, however, with heightened volatility throughout the quarter as markets recalibrated their expectations for Fed policy. Meanwhile, in foreign exchange markets, the delay in rate cuts helped further boost the U.S. dollar’s strength, while derivatives markets established first-quarter records for average daily volume for U.S. Treasury futures and options.

At Russell Investments, our 35-plus years of experience executing trades for a wide range of institutional clients affords us unique and valuable insights into today’s market trends and insights. We trade approximately $2.3 trillion annually through our multi-venue trading platform, and maintain a 24-hour global trading desk with access to over 100 countries across all asset classes. Here are key observations from the first quarter of 2024.

EQUITIES

The first quarter of 2024 saw strong market performance in the U.S., Europe, Japan, Taiwan, and India.

U.S.

In the U.S., the S&P 500® Index set a record high, rising over 10% and logging its best first-quarter performance since 2019—and second-straight quarter of double-digit percentage gains.

While most of 2023’s robust market gains were driven by the Magnificent Seven stocks, the first quarter of 2024 saw marked divergence in performance among these seven members. Four of the seven kept up the momentum, with Amazon (AMZN), Meta (META), Nvidia (NVDA), and Microsoft (MSFT) leading the pack, while both Apple (APPL) and Tesla (TSLA) were the laggards, declining by 11% and 29%, respectively.

Global IPOs

Looking at the Global IPO (initial public offering) market, the results from the first quarter were mixed, based on geography. On a year-over-year basis, Q1 2024 global volumes fell 7% due to ongoing declines in China/Hong Kong, but global IPO proceeds were up 7% year-over-year. Notably, the U.S., Europe, and Japan saw solid growth in the number of IPOs and the value of offerings.

Europe

European markets closed the first quarter around 6.8% higher. This positive trend was driven by recent inflation data that showed consumer prices are coming down.

Click image to enlarge

Asia

In Asia, healthy inflows continued in Japan, South Korea, Taiwan, and India, which were reflected in market performance. China even saw net foreign inflows for the first time in six months.

One major event in the region during the quarter was the Bank of Japan’s (BOJ) decision to end eight years of negative interest rates on March 19. The BOJ additionally decided to discontinue purchases of risky assets like exchange-traded funds (ETFs) and Japanese real estate investment trusts (REITs).

Other key observations

From a market structure point, the U.S. market set new records for average daily volume ($11.7 billion shares) and average daily turnover ($619.6 billion).

Bid/ask spreads were steady on an aggregate global basis and closing auction volumes stayed in line, with the exception of quarter-end volumes, which are historically higher than average.

As we look to the second quarter, the focus will be on earnings growth, U.S. interest rates, China’s economic recovery, and whether inflation will continue to moderate across the globe.

FIXED INCOME

Rates continued to be volatile over the first quarter of 2024, with news hanging on every word from the Fed. With expectations of three interest-rate cuts this year, Treasury bonds sold off hard during the January-through-March period, while riskier assets outperformed. CPI (consumer price index) numbers continued to surprise to the upside over the quarter, leaving many market observers speculating on whether the Fed may push back its timeline for an initial June rate cut. Fixed income markets also speculated over the end of quantitative tightening and the reduction of the Fed’s balance sheet. Particularly, with already high issuance in the Treasury market, there is concern that the reduction of the central bank’s balance sheet could lead to too much supply for investors. Many analysts are projecting new issuance to be reduced to make room for the balance-sheet reduction, with plenty estimating the Fed will start with mortgages in the first phase.

U.S. investment grade and high yield credit had a strong quarter, led by financials for investment grade assets and energy for high yield. New issuance in investment grade continued its hot start to the year, with $537 billion of new deals year-to-date—up 35% from the same time period in 2023. Continued expectations for new issuance in April are around an additional $100 billion. With strong supply, we’ve seen dealers’ balance sheets build over the quarter, adding new inventory with net positions peaking above $25 billion—up from $10 billion in early February. From our vantage point, the strong risk-on rally in equities and credit could continue if inflation consistently outperforms estimates in Q2.

FOREIGN EXCHANGE

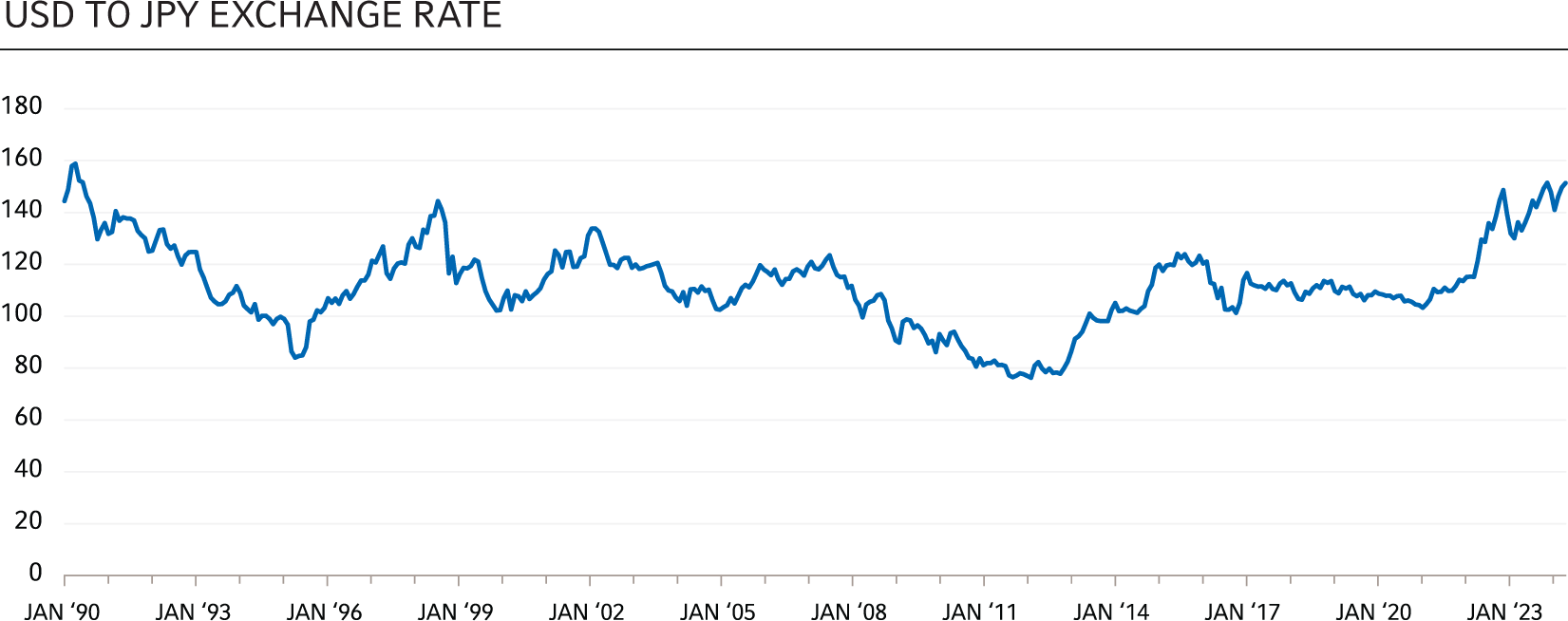

Hope that the Fed could begin cutting rates soon diminished as the first quarter progressed, due to stronger-than-expected U.S economic data. The BoJ’s decision to end its eight-year negative interest rate policy in mid-March was quickly overshadowed by the lack of relief in the USD/JPY (U.S. dollar vs. Japanese yen) exchange rate, with the U.S. dollar hitting its highest level against the yen in 34 years. The days when the JPY and the CHF (Swiss franc) were seen as safe-haven currencies in this unstable geopolitical world seems to be a thing of the past, as the U.S. dollar trudges onward and upward against other major currencies.

Click image to enlarge

DERIVATIVES TRADING

In a moment that seemed eerily familiar, the U.S. Senate passed a measure in the early hours of March 23 to keep the government funded through the end of the fiscal year on Sept. 30, 2024. Meanwhile, the CBOE (Chicago Board Options Exchange) Volatility Index (VIX) closed the quarter at low levels and CME Group reported record first-quarter average daily volume for U.S. Treasury futures and options.

A robust ecosystem Is necessary for high functioning, liquid derivatives markets. Listed futures, cleared swaps and bilateral OTC (over-the-counter) swaps can serve to complement existing listed securities markets and provide alternatives for how to implement views or exposures. Keeping track of regulatory changes that impact any one part of the ecosystem is important. As currently proposed, Basel III implementation in the U.S. could increase costs and impact an otherwise robust ecosystem. In a welcomed move, during the first quarter, U.S. Treasury Secretary Janet Yellen acknowledged the significant industry feedback about Basel III implementation and promised “broad and material changes” to the proposed rules.

The bottom line

The significant shift in rate expectations during the first quarter demonstrates all-too well the fragilities and complexities of today’s economy and markets—and underscores the importance of working with an experienced and agile investment solutions provider in order to manage risk and move money expeditiously.

At Russell Investments, we’re committed to delivering scalable solutions that meet the trading and execution needs of asset owners and asset managers alike. We’re also dedicated to sharing our insights and observations from our global trading desk every quarter. Please reach out if you have any questions.