Key takeaways:

- While investors may be averse to seeing losses in their portfolio, those losses can be used to minimize investment taxes

- Implementing a tax-loss harvesting strategy throughout the year can create a bucket of tax “assets” to offset taxable gains

- Considering a portfolio as a whole rather than a collection of stocks can help

What's in a name? While Shakespeare was right that a rose would smell as sweet no matter the name, some words are less appealing for investors than others.

Let’s take tax-loss harvesting as an example. The point of this strategy is to help reduce investment taxes. It’s a good thing. What it creates are often known as tax-loss carryforwards. That’s a bit of a mouthful and may sound negative to many investors. I prefer to call them tax “assets,” which has a much more positive connotation than "loss."

Think about sitting down with a client and saying: "in this time of market volatility, we are maximizing value creation by harvesting tax assets that can be used to lower your tax bills." Sounds a lot better than saying "markets are down, and we are harvesting losses." The second option might scare an investor, since it sounds as though they will be losing rather than adding value.

Many investors are averse to having losses in their portfolios. But as we have all experienced, losses are inevitable in a stock portfolio. Because of their aversion to losses, investors don’t realize that they can actually benefit from them. That’s why tax-loss harvesting is somewhat of an art: it turns losses into something of value.

The typical investor path

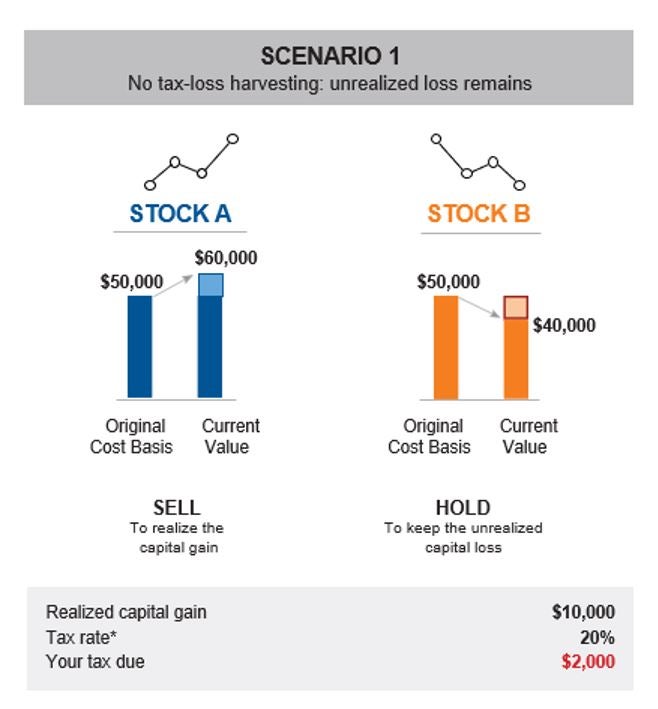

Let’s start with a basic two-stock portfolio: Stock A and Stock B.

Just as they hate losses in their portfolio, many investors are averse to selling stocks that have lost them money. It’s a behavioral trait we have as humans in that we get a hormonal high when we make money, but an opposite reaction when we lose money. It’s why you are more likely to hear investors brag about their “winners,” but rarely, if ever, talk about their “losers.”

Let’s look at the first illustration below. Two stocks were purchased at the same price, and over time Stock A gains $10,000 in value and Stock B loses $10,000 in value. Most investors will look at Stock A and say something like: “I made good money on it, it’s time to lock in my profit,” and then look at Stock B and react: “ouch, I don’t want to realize a paper loss. I’ll wait”.

The outcome is that they sell Stock A for a $10,000 gain and hang on to Stock B. The Internal Revenue Service will want their pound of flesh in the form of a tax on that capital gain. Assuming a 20% tax rate, this investor will receive a tax bill of $2,000 (which reduces their profit to $8,000) and will still be holding on to the other security in their portfolio that’s currently trading at a loss.

(Click image to enlarge)

The example provided above is for illustrative purposes only and does not constitute tax, legal, or investment advice. Tax-loss harvesting strategies may not be suitable for all investors and may have tax implications.

A better path forward

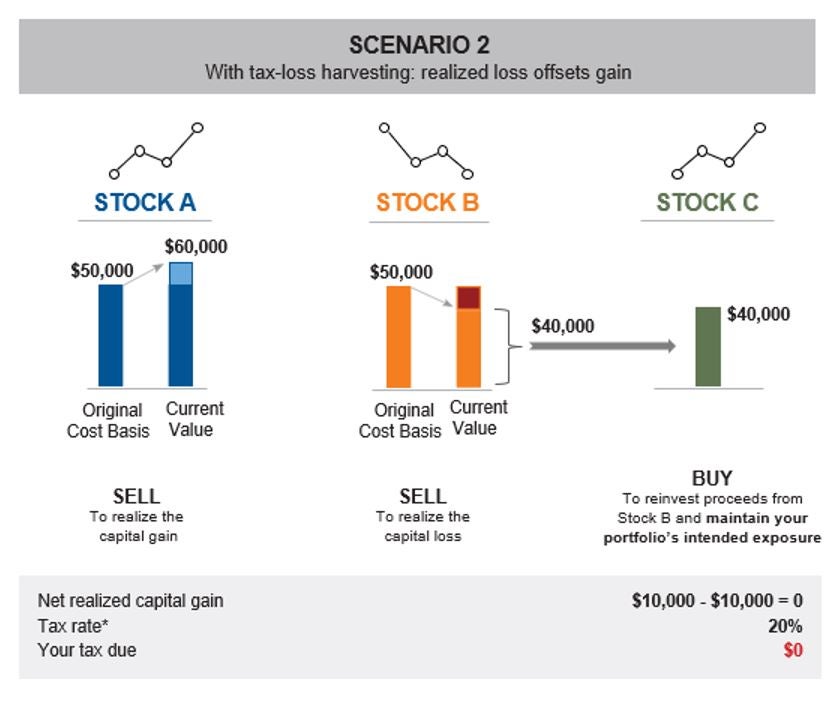

What an investor can do instead is think about the portfolio as a whole rather than in terms of individual stocks. While it may be exciting to see individual winners, the reality is that most portfolios are built using a basket of stocks to achieve a greater goal. Let’s look at the portfolio through this type of lens instead.

When we look at the portfolio now and think about making changes, we can see there is a gain of $10,000 in Stock A and a loss of $10,000 in Stock B. Instead of just selling Stock A, we now also sell Stock B. This creates a $10,000 loss (or better said, a tax asset!) that we can use to offset the gain from stock A. This gives us the ability to redeploy the proceeds of the sale to another stock that could have the potential for future gains, while canceling out the tax bill ($10,000 gain - $10,000 loss = net even = no tax bill).

(Click image to enlarge)

{kind=link}

The example provided above is for illustrative purposes only and does not constitute tax, legal, or investment advice. Tax-loss harvesting strategies may not be suitable for all investors and may have tax implications.

The key is to look at the portfolio as a whole rather than as a collection of individual parts.

As for why buy or sell any of the portfolio in the first place – there could be a number of reasons, including portfolio repositioning. The point here is to illustrate how a more thoughtful approach to tax management could help achieve a better after-tax outcome for investors.

Endless opportunities

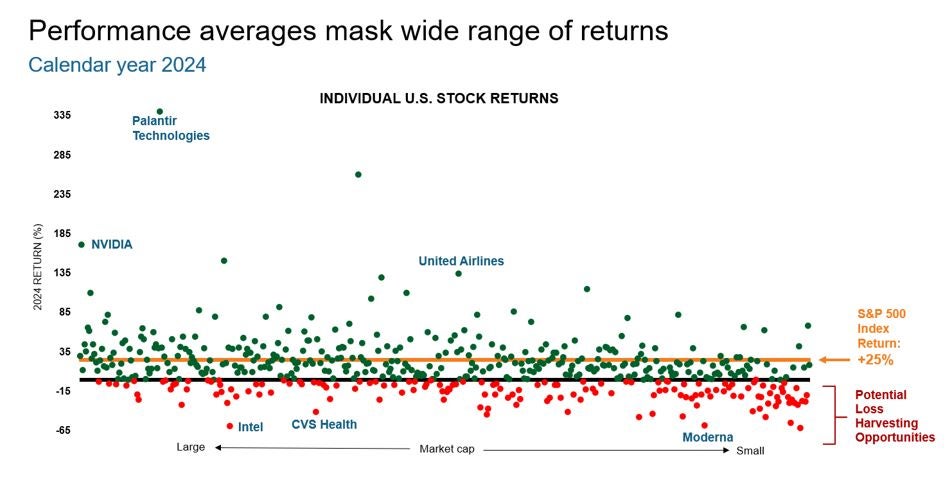

Let’s now expand on how large the tax-loss harvesting opportunity can get in a diversified portfolio.

When you look at a pool of stocks, let’s say the 500 largest in the U.S. as shown in the chart below, you can see there is a large dispersion of outcomes. As an example, in 2024 the S&P 500 Index had a return of around 25%. Yet, look at the number of red dots below the gray line which represent stocks that ended the 365-day period at a loss.

(Click image to enlarge)

Source: Russell Investments. Stocks represent companies in the S&P 500 Index on 12/31/2024. Past performance is not an indication of future opportunities/performance.

In any diversified portfolio comprised of individual stocks, there will be winners and losers no matter what the market is doing. One can create even better after-tax outcomes by harvesting losses frequently throughout the year so that more tax "assets" can be made available to help an investor lower their year-end tax bill.

Russell Investments is your partner

There is a lot that goes into managing a portfolio to minimize the cost of taxes and maximize after-tax wealth. I have just illustrated the art of tax-loss harvesting in its simplest form. What’s harder is doing it at scale, in a systematic manner, and with a level of frequency throughout the year that makes it impactful. This is how partnering with us can help you. We can leverage our years of experience performing tax management to help you guide your clients to a better after-tax outcome. Please reach out to learn more about our approach to tax management.