Key Takeaways

- Pension surplus can be used strategically to benefit both participants and sponsors

- Uses include funding benefit enhancements, early retirement incentives, or future plan accruals

- Sponsors should balance participant security, fiduciary duties and organizational goals when using pension surplus

Trapped capital? Think again.

In recent years, pension funded status has markedly improved, with average funded ratios surpassing 100%.1 Many sponsors who once faced significant contribution requirements and PBGC premiums now manage well-funded plans with fewer complications. Historically, the primary goal for many sponsors was to achieve sufficient funding to enable either plan hibernation or plan termination. Today, however, an increasing number of sponsors are recognizing the range of potential opportunities surplus assets can provide.

Yet the traditional view often undervalues pension surplus beyond termination needs. It’s time to rethink that. Simply put, the industry expression of pension surplus as “trapped capital” is an exaggeration. Why? Because there are many ways to put plan surplus to work strategically (some are easier to implement than others). First and foremost, though, each option should be thoughtfully evaluated with the organization’s goals and fiduciary responsibilities in mind.

Hidden Value

First, when deciding how to value a pension plan’s surplus, sponsors should closely examine the range of available options and their alignment with organizational objectives. The potential value of surplus assets should not be underestimated, as using them wisely can lead to significant benefits.

The value attributed to surplus pension assets also affects how a sponsor chooses to invest. For example, a sponsor with a 120% funded plan with 90% of assets invested in liability-hedging fixed income may choose to reduce that allocation to 80% to build in more potential for asset growth, while keeping the liability hedge. This makes sense if value is placed on surplus and the chances of becoming underfunded again are low.

Once participant benefits are secured and fiduciary requirements met, sponsors can explore numerous ways to use surplus assets. These range from strategies that primarily benefit participants to those that favor plan sponsors, as well as approaches that deliver shared advantages to both.

Plan sponsors should be mindful of the role they are filling when making decisions regarding pension surplus. Fiduciaries act in the interest of participants in the plan, while settlors act in the interest of the business.

Benefit Boost

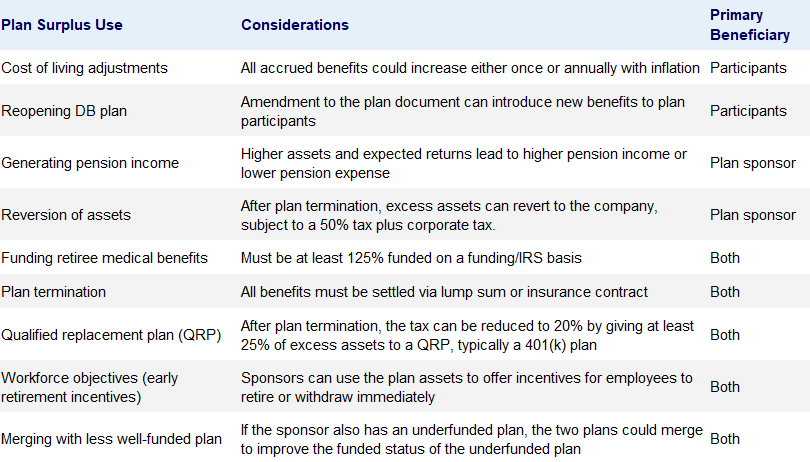

One of the simplest ways to use surplus for participants is by enhancing the plan to increase accrued benefits. Examples include granting ad hoc benefit increases above original plan commitments or—as seen in recent precedent (IBM in 2023)—reopening previously closed or frozen plans to new accruals.

Sponsors might also consider introducing one-time cost-of-living adjustments—a feature largely absent from U.S. corporate pension structures—or providing supplemental “13th check” payments to retirees. Each of these measures uses surplus assets to elevate participant outcomes while maintaining the plan’s full funded status.

Unlocking Sponsor Gains

Meanwhile, pension surplus can also directly help the sponsoring organization. From an accounting perspective, more surplus and a higher expected rate of return may result in increased pension earnings, which may be important to sponsors.

Following plan termination, a part of the excess assets may be returned to the sponsor. However, this reversion is subject to a substantial tax rate of 50%, plus applicable corporate taxes. If at least 25% of the surplus is used to benefit 401(k) participants, the tax rate on the reverted amount may be reduced to 20%. For sponsors of non-frozen plans, pension surplus can be used to fund future ongoing benefit accruals.

Mutual Benefits

In addition, some uses of pension surplus could potentially benefit both the participants in the plan and the sponsoring organization. If the company sponsors a separate underfunded plan, they could merge it with the fully funded plan. This could potentially increase the benefit security for participants in one plan while maintaining it in the other. Participants could receive early retirement incentives, helping the sponsor with workforce objectives while supporting participants ready for retirement.

Here are some key uses of pension surplus, along with considerations.

Unlocking Pension Surplus

Sponsors can use pension surplus to benefit participants, the company or both

Applications, key considerations and beneficiaries of pension surplus

Breaking the Mold

For many years, plan sponsors with underfunded pension plans focused on achieving full funding. Most closed or frozen plans followed a glidepath approach—reducing exposure to return-seeking assets in favor of liability-hedging assets—to help secure gains in funded status.

Now, as many sponsors find themselves with fully funded plans but without immediate plans to terminate, it is time to reconsider the potential value of surplus assets. There is no need to compromise benefit security, and several practical options exist that may deliver tangible value. It is worth re-examining whether plan surplus truly is “trapped capital.”

1 Source: Milliman’s Pension Funding Index