Key takeaways

- Capital gains distributions are higher in 2025 due to strong market returns.

- Most equity categories expect increased distributions, especially growth and mid-cap segments.

- Investors should assess tax exposure and redirect distributions to more tax-efficient solutions.

The year is winding down, but Cap Gains SZN is ramping up. It’s that time when the holidays bring together family, friends and shared traditions. There is a natural pause to reflect on the year’s accomplishments and lessons learned. It also marks the period when fund families start to calculate their net realized capital gains. For investors, “lessons learned” can take on a new meaning as they start to see what their tax bill could look like.

Around this time, most mutual fund and exchange-traded fund (ETF) providers release estimates of their upcoming distributions. We track and aggregate these early numbers to help you better prepare for what to expect. While the amounts won’t be final until distributions are officially announced and paid, with more than 75% of all funds having their estimates announced at this point, there is enough information to start assessing the broader picture.

Reflecting on 2025 market returns & historical distributions

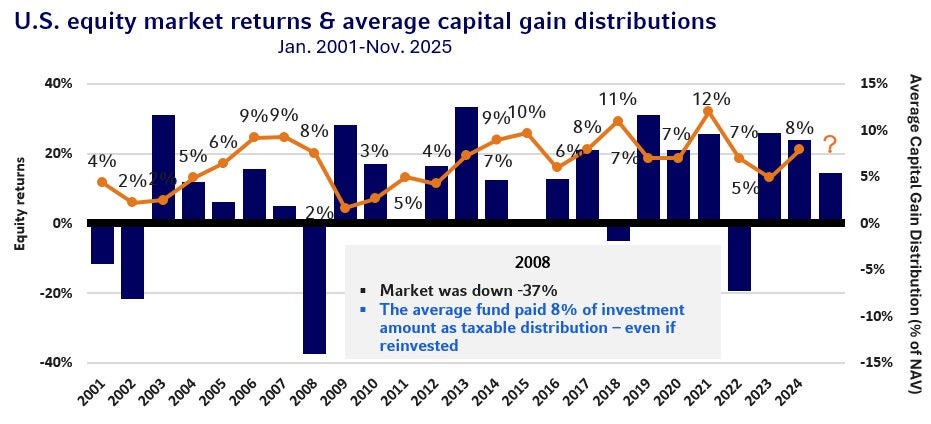

Despite volatility early in the year, year-to-date market performance remains strong across the board. Focusing on equites, the Russell 3000 Index is up roughly 17.4% through the end of November, while international developed (MSCI EAFE Index) and emerging markets (MSCI EM Index) are up 24.5% and 29.5%, respectively, through the same time frame. So, the tradition of investors running into capital gains distributions is expected to continue and can potentially be a bit more widespread across asset classes given broader participation outside of U.S. equites.

As shown in the chart below, capital gains are distributed annually—typically during the month of December—and happen regardless of how markets perform. In strong market years, like this one, a tax bill alongside positive performance seems like a natural trade-off. Strong performance adds pressure, but it’s the investment activity within the funds that causes taxable distributions.

Having a highly appreciated portfolio—something that many investors may have experienced lately—makes it harder for managers to incorporate active management decisions without tapping gains. That challenge grows when investor preferences lead to outflows, which can pressure managers to sell positions they otherwise wouldn’t touch. This is also why capital gains may still occur in down years.

Source: Russell Investment & Morningstar Direct, 12/5/2025, unless noted. U.S. Stocks: Russell 3000® Index as of 11/30/2025. U.S. equity funds: Morningstar U.S. Category Group ‘U.S. Equity’ which includes mutual funds and ETFs (and multiple share classes). For years 2001 through 2020 % = calendar year cap gain distribution ÷ year-end NAV, 2021 through 2023 % = total cap gain distribution ÷ respective pre-distribution NAV. For years 2001 through 2013, used oldest share class. 2014 forward includes all share classes. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

The table below offers a snapshot of how this translates in dollar terms. We incorporated the average capital gain distribution paid by U.S. equity funds over the last 4 years (2021-2024) along with this year’s estimate of 8.1%. Assuming a $500k portfolio at the start of each year and applying the highest long-term capital gains tax rate (23.8%), that comes to roughly $6-$12k in tax each year. If this year plays out as estimated, that’s nearly $50k in taxes over the last 5 years.

*Capital gain distribution percentages for 2021–2024 reflect actual average capital gain distributions, while the 2025 figure reflects an estimated average. All values are based on Morningstar U.S. Category Group ‘US Equity,’ which includes mutual funds and ETFs. **Represents maximum long-term capital gain tax rate of 20% for Married Filing Jointly and 3.8% Net Investment Income Tax. Illustrative example only. Actual tax outcomes will vary. This is not tax advice. Please consult your tax advisor.

2025 – The broad view

With that backdrop in mind, it makes sense to start the broader asset-class discussion with U.S. equities. They tend to command the largest share of most investor portfolios and have also delivered some of the strongest multi-year returns across asset classes, which means they typically drive the bulk of capital gain distributions. This year is no exception as U.S. equity funds are expected to make the largest distribution relative to other major fund categories, averaging about 8.1%.

This isn’t much of a surprise as the Russell 3000 Index has delivered returns of +20% in five of the last six years and is up 17.4% year-to-date, so most funds are sitting on some hefty, embedded gains. Below, you will see a summary of distribution estimates within the U.S. equity category, broken down in style box form.

Source: Russell Investments & Morningstar Direct as of 12/5/2025. Total number of funds expected to make a distribution is based on the funds that formally announced capital gains estimates. Currently 735 out of 939 for Large Value, 759 out of 1,054 for Large Blend, 699 out of 908 for Large Growth, 218 out of 325 for Midcap Value, 178 out of 313 for Midcap Blend, 290 out of 411 for Midcap Growth, 264 out of 388 for Small Value, 317 out of 461 for Small Blend, 300 out of 452 for Small Growth are expected to make a distribution. The calculation excludes funds that are not expected to make a distribution. For the details of the calculation and total number in each category, see disclosures.

First, across market cap, estimated distributions are coming in slightly higher across the board. Large cap funds are averaging 7%-10%, mid-cap 7%-11% and small cap 6% through 8%. Growth-oriented strategies are toward the top of each market cap segment.

Most categories are estimating distributions roughly 1 to 3 percent higher than what they paid out in 2024. Mid-cap growth stands out in particular; after paying the highest distribution among all U.S. equity segments last year, they are estimating an increase of about 3 percent for 2025.

Outside of U.S. equities, international equity estimates are coming in a bit higher than we have been used to, at 7.2% on average. This is partially due to their strong 2025 returns. The largest estimates are seen within smaller and more growth-oriented segments. Sector equity is coming in modestly lower at roughly 6% on average, with a wide range. Growth-leaning sectors are at the higher end, aligning with U.S. style-box trends, whereas real assets and defensive sectors are on the lower side.

Source: Russell Investments & Morningstar Direct as of 12/5/2025. Total number of funds expected to make a distribution is based on the funds that formally announced capital gains estimates. Currently 3,760 out of 5,251 for U.S. Equity, 1,691 out of 3,175 for International Equity, 449 out of 1,165 for Sector Equity, 64 out of 280 for Non-Traditional Equity, 18 out of 106 for Commodities, 2,718 out of 3,831 for Allocation, 64 out of 197 for Alternative are expected to make a distribution. The calculation excludes funds that are not expected to make a distribution. For the details of the calculation and total number in each category, see disclosures.

Non-traditional equity funds, which include funds focused on derivatives and long-short approaches, are tracking just under 6% on average. Given the nature of these strategies, they tend to be less tax-efficient, so expecting a mid-single digit average estimate isn’t surprising.

Commodities and alternative funds are estimating to pay a distribution toward the lower end of the overall range, with most distributions classified as short-term rather than long-term. Allocation funds are estimating similar levels, with larger averages coming from more aggressive, equity heavy mixes, topping out at 5.7% on average.

Summary - Investor and advisor action steps

While we could go much deeper and dissect each asset class, fund family, or individual funds, investors should use this data as a broad starting point. It can help identify areas that may not be aligned with their taxable interests.

Investors may consider not automatically reinvesting distributions if minimizing current-year tax drag is a priority. Instead, consider directing distributions to more tax‑efficient options that align with your objectives and circumstances. One way to pursue after‑tax wealth growth is to reduce tax drag where possible.