The latest reconstitution resulted in some of the most significant style changes in years, with several large-cap companies moving between growth and value indexes as their earnings profiles evolved.

Key Takeaways

- The latest FTSE Russell reconstitution materially reshaped growth and value benchmarks, reflecting how changing corporate fundamentals are redefining traditional style classifications.

- Evolving benchmark weights create new implementation challenges as active managers adjust portfolios to manage unintended active risk.

- SpaceX demonstrates how mega-cap IPOs can become increasingly important benchmark constituents as free float expands over time.

- With more large IPOs expected, benchmark composition may evolve more continuously than investors have historically experienced.

FTSE Russell* reconstitution highlights a changing benchmark landscape

The now semi-annual reconstitution of the FTSE Russell U.S. Indexes is typically viewed as a routine benchmark update. However, the most recent semi-annual reconstitution of the FTSE Russell Indexes, completed on June 26, was one of the most consequential in years. Mega-cap companies previously classified exclusively as growth moved into value, while companies traditionally viewed as cyclical migrated into growth as AI infrastructure spending reshaped their earnings profiles.

These changes illustrate how evolving business fundamentals are redefining traditional style classifications while highlighting a broader shift in how benchmark composition evolves. For active managers, portfolio implementation increasingly extends beyond security selection to managing benchmark change itself. For passive investors, benchmark exposures may become more fluid as large public companies mature after listing, making benchmark evolution a more continuous process than investors have historically experienced.

*FTSE Russell U.S. Indexes are owned and maintained by FTSE Russell and are not affiliated with Russell Investments

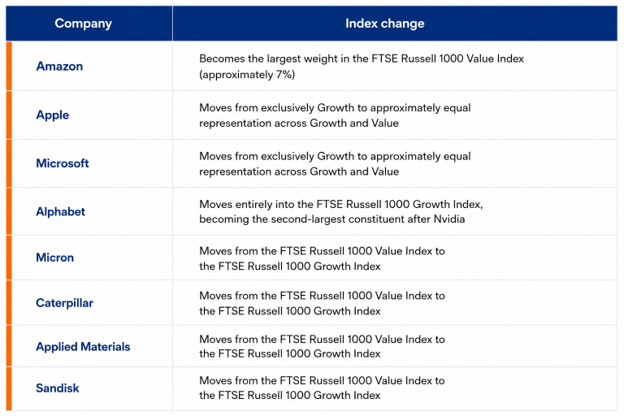

The largest benchmark changes

The scale of this June’s constituent moves materially altered both the FTSE Russell 1000 Growth and FTSE Russell 1000 Value Indexes. Several of the market's largest companies changed style classifications, creating meaningful changes in benchmark weights and sector exposures that active managers must now manage relative to their benchmarks.

FTSE Russell finalized the annual reconstitution of the FTSE Russell U.S. Indexes after the market close on June 26. The largest changes included:

Source: FTSE Russell

While constituent changes occur during every reconstitution, the concentration and size of the shifts concluding this month materially changed benchmark composition. For active managers, benchmark exposures shifted immediately, creating unintended active weights even where underlying portfolios remained unchanged.

What we are seeing with active managers

The largest shifts occurred within the FTSE Russell 1000 Value Index, where several of the benchmark's largest holdings, including Micron, Alphabet, and Caterpillar, moved out of the index and were replaced by mega-cap technology names. That has created sizable active positions relative to the new benchmark. Over recent weeks, managers have reduced unintended overweights and closed underweights to manage relative risk.

Broadly, value managers have added to Amazon while reducing exposure to Alphabet following the latter's strong rally over the past year. Opinions on Apple and Microsoft are more mixed, but most managers expect to maintain positions, even at active underweights, given their combined benchmark weight of roughly 10% following the reconstitution.

Among the more traditionally cyclical companies, including Micron and Caterpillar, many value managers exited their holdings earlier, unwilling to underwrite what they viewed as an AI-driven supercycle. Those decisions have contributed to year-to-date underperformance as both stocks have continued to rally.

Growth managers have long managed a highly concentrated benchmark given the dominance of mega-cap technology names. Independent of the reconstitution, many had already reduced exposure to Apple and Amazon as their relative growth rates slowed, reallocating that capital to Alphabet. For these managers, the reconstitution largely reflects positioning that was already underway rather than driving significant portfolio changes. The next meaningful shift for growth benchmarks may instead come from the recent and expected wave of mega-cap IPOs.

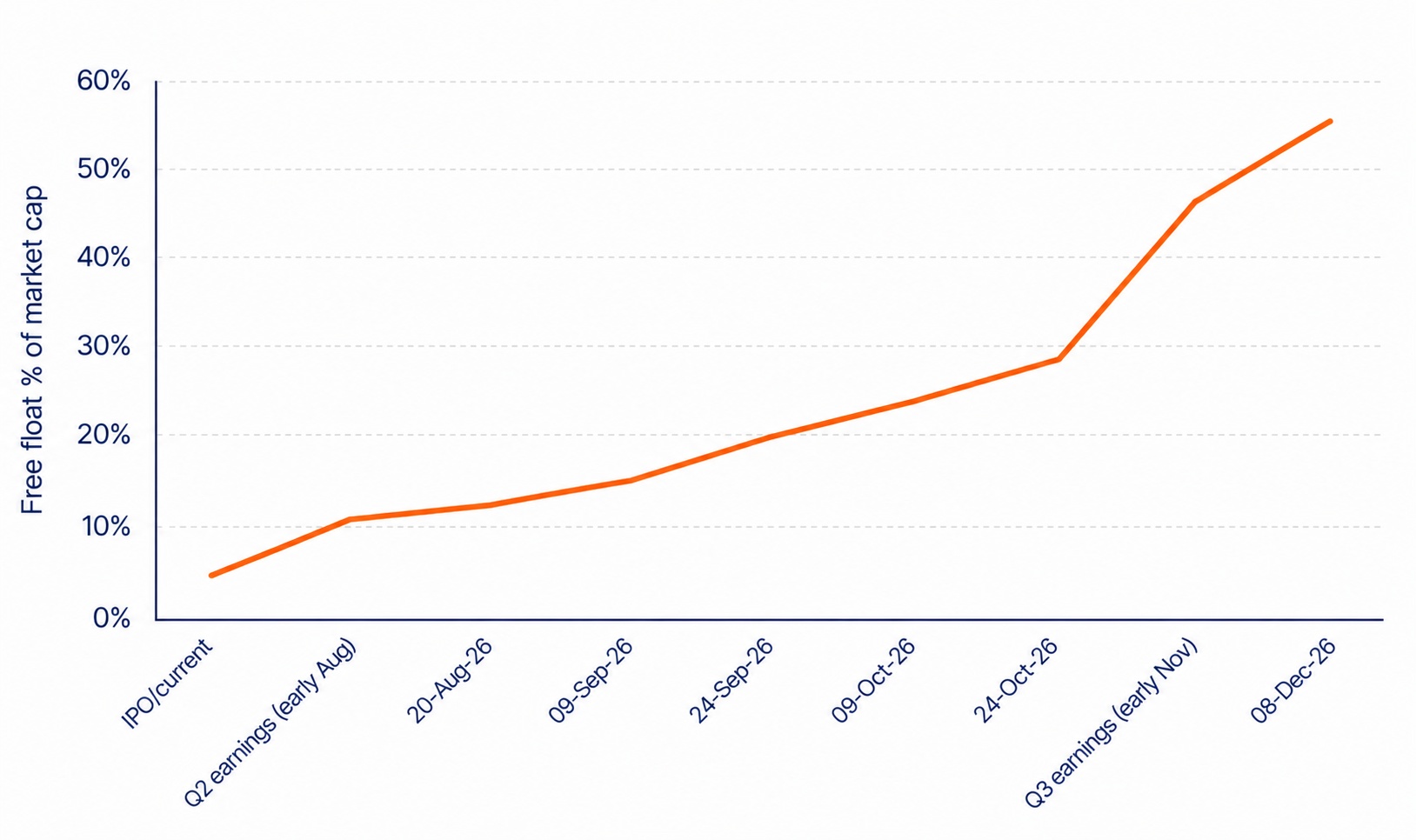

SpaceX offers a preview of mega-cap IPO impacts

SpaceX's IPO offers an early look at how the next generation of mega-cap IPOs could influence benchmark composition. The company priced its IPO at $135 per share on June 12, raising approximately $75 billion in the largest IPO on record. As one of the first companies expected to emerge from the current wave of mega-cap listings, SpaceX immediately sparked discussion around benchmark inclusion and investor positioning.

Despite its size, the IPO had only a modest initial impact on major indexes because fewer than 5% of the company's shares were publicly available. With roughly 91% of shares remaining locked up and held by Elon Musk and other pre-IPO investors, SpaceX entered benchmarks at relatively small weights. That limited public float has also contributed to elevated share price volatility, as supply and demand dynamics have had a greater influence on trading than fundamentals. Most growth managers we spoke with viewed the valuation as fair to somewhat overvalued and expected supply and demand dynamics to outweigh fundamentals in the early days following the IPO, a view that has proved prescient given the elevated volatility in the share price since.

Since SpaceX currently has a relatively small public float, its initial weight in major benchmarks remains modest despite its size. As lock-up periods expire and free float increases as a percentage of market capitalization, the company's benchmark weight is expected to grow over time.

SpaceX free float timeline

Sources: Russell Investments, SpaceX

The next milestone is the expiration of those lock-up periods. As additional shares become publicly available and free float expands, SpaceX's benchmark weight is expected to increase. For active managers, choosing not to own the stock therefore becomes a progressively larger active position over time rather than a one-time IPO decision.

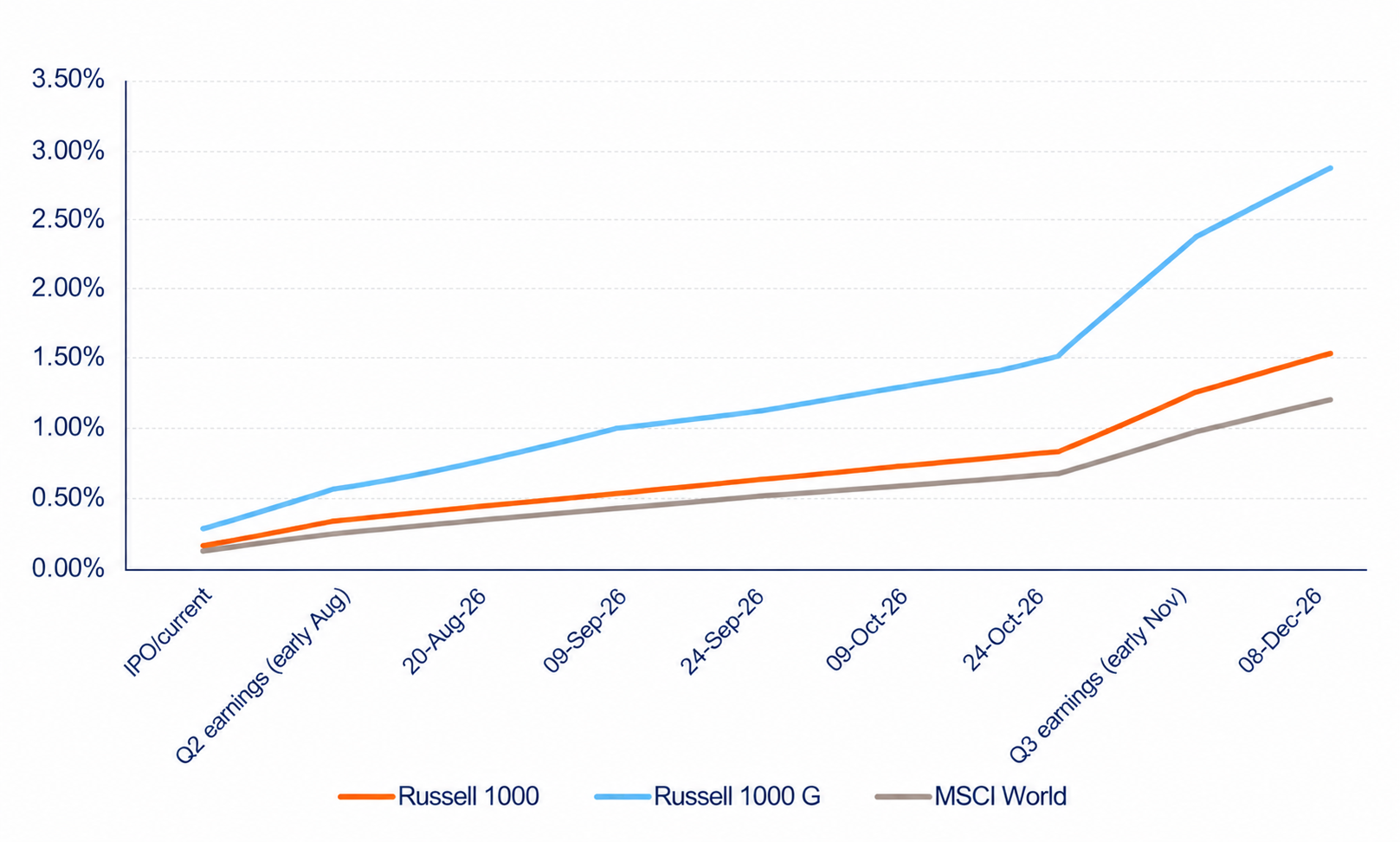

SpaceX benchmark weight

Sources: Russell Investments, SpaceX

SpaceX is unlikely to be unique. Anthropic, OpenAI, and other anticipated mega-cap IPOs, potentially entering the public markets with valuations exceeding $1 trillion, could follow similar free-float dynamics. While their initial benchmark weights may be modest, expanding public float in the months following their IPOs could make them increasingly significant benchmark constituents.

Investor implications

The latest FTSE Russell U.S. Indexes reconstitution demonstrates that benchmark composition is becoming more dynamic as changing corporate fundamentals reshape traditional growth and value classifications.

For active managers, evolving benchmark weights increasingly require portfolio adjustments to manage unintended active risk while maintaining high-conviction positions. For passive investors, benchmark exposures will also continue to evolve as newly public companies expand their free float and become more meaningful index constituents over time.

With a growing pipeline of mega-cap IPOs expected to come to market, benchmark composition may change more continuously than investors have historically experienced, making it increasingly important to understand not only benchmark performance, but how the benchmarks themselves are evolving.

Common client questions

FTSE Russell's style methodology reflects companies' evolving fundamentals. Strong AI-related investment and changing earnings expectations led several companies to shift from their previous classifications.

The reconstitution changes the composition of widely followed benchmarks, prompting portfolio rebalancing by index funds and influencing benchmark-relative performance for active managers.

Passive funds tracking the FTSE Russell U.S. Indexes must rebalance to match the updated index composition, which can change investors' exposures and create elevated trading activity around the rebalance.

For active managers, benchmark changes have become an increasingly important portfolio implementation consideration alongside security selection, particularly when large companies change style classifications.

Yes. The latest reconstitution highlights how rapidly evolving business models and AI-driven earnings growth are reshaping traditional distinctions between growth and value, making benchmark composition more dynamic than in the past.

Yes. While each index provider uses its own methodology, major benchmark providers such as MSCI and S&P Dow Jones Indices regularly review index composition and style classifications to reflect changes in company fundamentals. As business models and earnings profiles evolve more rapidly, investors should expect benchmark composition across providers to become increasingly dynamic over time.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.