U.S. banking system update: What are the potential implications for Fed policy?

Executive summary:

- Programs announced by the U.S. government in response to the failures of SVB and Signature Bank should help limit systemic risk in the banking system

- The near-term outlook for the Federal Reserve’s interest rate policy is extremely uncertain

- We believe that a 50-basis-point Fed hike in March is now extremely unlikely

My colleague Erik Ristuben put out a comprehensive article about how to interpret the stresses in the U.S. banking system last night. Today’s report updates what we learned in the last 24 hours and broadens the discussion to consider what recent developments mean for U.S. Federal Reserve (Fed) policy going forward.

To reiterate Erik’s key points:

- Silicon Valley Bank (SVB) was unusually exposed due to its concentrated deposit base—venture tech companies—and a badly managed long duration Treasury portfolio

- The U.S. government announced a forceful response to the failures of SVB and Signature Bank on Sunday, including:

- Full protection of all insured and uninsured deposits at the failed banks; and

- A new Bank Term Funding Program (BTFP) at the Federal Reserve which allows financial institutions to access liquidity at the central bank instead of crystallizing losses on their hold-to-maturity Treasury portfolios. Importantly, this program allows the banks to post their Treasuries as collateral at par—not at currently discounted market prices.

- Collectively, these programs are designed to slow the outflow of deposits from regional banks and to provide a liquidity backstop for those banks that remain under pressure. In our view, this should help limit systemic risk in the banking system.

How did markets react to the U.S. government’s response?

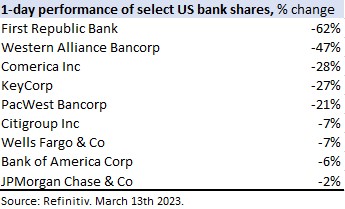

U.S. equities swung from gains to losses to gains and back again in volatile trading. As of the Monday close in New York, the S&P 500 Index ended the day down by a whisker—15 basis points (bps). However, bank shares remained under significant pressure.

As Erik emphasized yesterday, bank exposures vary wildly from one institution to the next and the more vulnerable banks were going to be scrutinized by the market. Social media images from Saturday, which showed customers lined up outside of First Republic Bank, stoked concerns of a run on that bank among investors. For some context, First Republic is another Bay Area bank with an outsized share of large, commercial deposits. Western Alliance—the parent company of Bridge Bank in the Bay Area—also suffered a significant drawdown on the day.

Meanwhile, U.S. government bond yields fell sharply amid flight-to-safety flows and a recalibration of monetary policy expectations, with the 2-year and 10-year Treasury yields declining by 59 bps and 15 bps, respectively, on Monday. The near-term outlook for the Federal Reserve’s interest rate policy is extremely uncertain. Ironically, this rally in Treasuries is actual good for bank balance sheets as it cuts the losses of the rate rises over the last year versus last week.

50-bps Fed rate hike next week now appears very unlikely

Arguments in favor of further rate hikes include an overheated labor market, an inflation overshoot and prevailing Fed guidance that “the historical record cautions strongly against prematurely loosening policy.” On the other hand, leading economic indicators are slowing and a few U.S. banks just failed.

We argued back in February that additional rate increases were no longer necessary. That view looked like it was in right field as chatter of a 50-basis-point hike in March intensified around Powell’s congressional testimony last week. It’s more mainstream now. Ultimately, the March decision will be up to Powell and the Federal Open Market Committee, not us. While the situation is fluid with an important inflation release tomorrow morning, our expectation is that a 50-basis-point hike in March is now extremely unlikely.

The relevant question for markets has refocused to whether the Fed will hike again, or not. That decision will likely hinge on the inflation data and whether the Fed can build confidence that its backstops for the banking system are working. Our baseline is that the backstop measures will prove effective, and the Fed will choose to deliver a 25-basis-point hike next week. But it is a close call for March, in terms of whether there is any hike at all. Either way, market pricing has downshifted notably in recent days toward our more dovish view. This repricing has been favorable for our tactical preferences within U.S. fixed income markets for duration and curve steepeners.

Source: Refinitiv. March 13th 2023.

The bottom line

This episode is another useful reminder that the Fed has raised rates very sharply in a very short period of time and the full effects of its actions can take time to show up on the real economy. We will continue to keep you apprised of the latest developments.