시장 전망: 2분기

업데이트

글로벌 시장

전망 안갯속으로

억눌린 과열

연착륙 기대감으로 단기적으로 시장 상승세가 지속될 수 있지만, 2024년 후반 급격한 경기 둔화 리스크 역시 높아질 수 있습니다. 인플레이션 하락세는 중앙은행이 하반기부터 양적 완화를 시작할 수 있음을 의미하지만, 시차를 두고 영향을 미치는 금리 정책의 특성상 기존 금리 인상의 여파가 아직 완전히 가시화되지 않았을 수 있습니다.

From the desk of the CIO

2024년 2분기에 들어서며 최신 글로벌 시장 전망을 공유하게 되어 기쁩니다.

진화하는 환경은 전통적인 기대와 오랫동안 유지되어 온 일부 투자 가정에 도전하는 시장 변칙을 계속 제시하고 있습니다.

2023년에는 많은 주요 경제학자들이 물가 안정을 회복하기 위해 필요하다고 말한 글로벌 경기 침체 없이 인플레이션이 빠르게 하락하는 모습을 보였습니다.

특히 미국에서는 강력한 경제 성장을 달성했음에도 불구하고 드물게도 물가와 임금 압박이 완화되었습니다.

노동 참여율의 증가는 노동 공급을 개선하는 데 도움이 되었고, 기업들이 대량 해고에 의존하지 않고도 인플레이션을 낮추는 데 도움이 되었는데, 이는 세계 대전 이후 역사에서 볼 수 없었던 현상입니다.

동시에 전 세계적으로 예상치 못한 다른 발전이 일어나고 있습니다. 일본에서는 기업 행동에 주목할 만한 변화가 일어나 자기자본이익률(ROE)을 개선하는 데 도움이 되었습니다. 캐나다는 미국과 달리 성장세가 둔화되었지만, 시장에서는 캐나다은행의 금리 인상 조치가 연준과 비슷할 것으로 예상하고 있는 것으로 보입니다. 한편, 미국 대형주 전반의 수익률은 갈수록 엇갈리고 있습니다. 예를 들어, Tesla는 35% 하락한 반면 Nvidia는 78% 상승했습니다.

종합하면, 이러한 복잡한 경제 및 투자 환경은 투자자들이 위험 자산을 전략적으로 재평가하고 보다 분별력 있는 접근 방식을 취할 것을 요구합니다. 글로벌 금융위기 이후 시대에는 액티브 투자와 패시브 투자가 혼합된 시대가 도래했지만, 현재의 분위기는 새로운 알파 및 다각화 소스를 통합하는 보다 적극적이고 신중한 접근 방식을 요구한다고 생각합니다.

당사의 최신 글로벌 시장 전망은 수석 투자 전략가인 Andrew Pease와 그의 팀이 제공하는 통찰력을 통해 이러한 새로운 트렌드에 대해 더 깊이 파고듭니다. 이러한 정보를 공유할 수 있도록 해주셔서 감사합니다.

Kate El-Hillow

President & Chief Investment Officer

Andrew Pease

GLOBAL HEAD OF INVESTMENT STRATEGY

“Just as last year’s investor pessimism was overdone, we worry this year’s optimism could eventually prove to be excessive.”

- Andrew Pease

억눌린 과열

미국 애틀랜타 연방준비은행의 라파엘 보스틱(Raphael Bostic) 총재는 최근 연설에서 ‘억눌린 과열(pent-up exuberance)1 ’이라는 표현을 사용했습니다. 이는 물론 보스틱 총재가 경기 가속화 위험이 다시 불거지고 있음을 언급하며 사용한 표현이지만, 현 시장 분위기도 잘 포착하고 있다고 생각합니다. 현재 경제 성장률은 회복 탄력적이며 인플레이션은 완화되고, 인공지능(AI) 열풍 테마와 관련된 초대형주를 필두로 기업 실적은 탄탄하게 유지되고 있습니다. 2023년에는 경기 침체 우려가 상당했지만, 증시로 신규 자금이 대거 유입되며 S&P500®지수가 다시 한번 사상 최고치를 경신하기 위한 긍정적인 모멘텀이 형성되고 있습니다. 예상외로 견조한 미국 경제 상황에 대한 기대감이 투자 열기로 번지고 있습니다.

미국 노동 시장, 둔화 조짐 보이나?

그러나 수면 아래를 들여다보면 균열이 눈에 띄고 있습니다. 3월 중순 기준 신규 일자리가 2022년 초 정점 대비 약 25% 감소하는 등 미국 노동 시장은 냉각되고 있으며, 특히 저소득층 가구가 위태롭다는 조짐이 포착되고 있습니다. 신용카드와 자동차 대출 연체율은 팬데믹 이전 수준 이상으로 치솟았습니다. 기업 부문에서는 고위험 등급 채권 연체율이 상승하고 있으며 상업용 부동산 연체율도 계속 증가세입니다.

팬데믹 발발 이후 기업과 가계는 막대한 현금을 비축하고 30년 만기 주택담보대출에 대해 저금리로 갈아타고 기업은 장기 회사채를 발급하는 등 연준의 긴축에 대한 강력한 방어책을 구축했습니다. 그러나 이러한 방어책이 이제 약화되고 있습니다. 미 연준이 통화 정책을 완벽하게 미세 조정함으로써 인플레이션이 2% 근처에서 안정되고 신규 일자리가 지난 3개월 평균인 26만 5천 개에서 실업률이 더 이상 하락하는 것을 막기 위해 필요한 수준인 월 10만 개 근처로 줄어드는 시나리오가 펼쳐지는 것이 가능할 수는 있습니다.

연준의 딜레마는 금리 인하 시점을 늦추고 인하폭을 지나치게 적게 하면 경기 침체 위험이 발생할 수 있고, 너무 성급히 금리 인하에 나서면 보스틱 총재가 우려하는 인플레이션 반등을 유발할 수 있다는 것입니다.

연준은 언제 금리 인하를 시작할 수 있나?

결국, 현 경기 주기에서 연준의 공격적인 긴축 정책이 시차를 두고 경제에 미치는 영향과 관련해 ‘이번에는 다르다(this time is different)’가 아니라 ‘이번에는 좀 더 오래 지속된다(this time is longer)’의 상황이 전개될 수 있습니다. 인플레이션 고착화를 우려한 미 연준의 신중론 때문에 금리 인하가 더욱 지연될 수 있다는 점은 걱정스럽습니다. 이 경우 최근 증시 랠리를 부추긴 연착륙 예상이 빗나가고 대신 완만한 경기 침체가 진행될 가능성이 높아집니다. 미 연준은 올해 중반부터 양적 완화를 시작할 것으로 전망되지만, 금리 인하 시기가 연말로 늦춰질 경우 장기적인 경기 전망에 대한 우려가 커질 것입니다.

유럽의 경제 회복력을 뒷받침하는 요소는?

대부분의 여타 선진국 경제도 반등하고 있습니다. 유럽과 일본 경제는 예상외로 강한 모습을 보이고 있습니다. 유럽 경제의 경우, 러시아의 우크라이나 침공 이전보다 낮아진 천연가스 가격, 글로벌 제조 활동 회복, 은행 대출 회복세가 긍정적으로 작용하고 있습니다. 유럽중앙은행(ECB)은 근원 인플레이션 하락 추세에 대응하여 6월 금리 인하를 시작할 가능성을 시사했습니다.

일본은 경제 활동과 기업 순익 증가세 측면에서 기대치를 상회하고 있으며, 올 들어 현재까지 토픽스 지수(TOPIX) 상승률이 최고치를 기록하는 등 증시도 고공 행진을 이어가고 있습니다. 일본을 둘러싼 리스크는 기업 지배 구조 개선 호재가 이미 주식 밸류에이션에 완전히 반영되었으며 일본은행의 통화 긴축 정책으로 엔화 강세가 유발되며 경제 회복의 발목을 잡을 수 있다는 점입니다.

대부분의 선진국 경제가 예상외로 선전하는 가운데 영국만은 예외적으로 경제 활동이 침체되고 인플레이션 또한 더디게 하락하고 있습니다.

중국의 2024년 GDP 성장률 목표는?

중국 경제 소식은 여전히 엇갈리고 있습니다. 부동산 시장 문제는 아직 해결되지 않았고 소비자 물가지수는 디플레이션 상태입니다. 지금까지의 경기 부양책은 단편적인 것이었지만, 2024년 중국의 GDP 성장률 목표가 5%라는 점은 향후 중국 당국이 의미 있는 정책을 내놓을 수 있음을 시사합니다.

당사는 지난 12월에 발표한 2024년 연간 전망 보고서에서 올해가 경기 둔화, 경기 침체 가능성, 경기 회복 사이의 중간 지대(twilight zone)가 될 것이며, 어떠한 시나리오도 명확한 판단을 내리기 어렵다고 언급한바 있습니다. 시장 전문가들은 향후 경제 침체 없이 인플레이션이 둔화되고 성장만 둔화되는 연착륙이 펼쳐질 것으로 예상하고 있습니다. 연착륙은 가능하겠지만, 경제 성장률이 결국 시장에 충격을 가할 위험이 지나치게 간과되고 있는 것으로 보입니다. 라파엘 보스틱 총재의 ‘억눌린 과열’ 언급은 투자자들이 신중하게 고려해야 할 경고라고 생각합니다. 작년 투자자들의 비관론이 지나쳤던 것처럼, 올해 낙관론이 결국 과도한 것으로 판명될 수 있는 점은 우려스럽니다.

완벽한 디스인플레이션

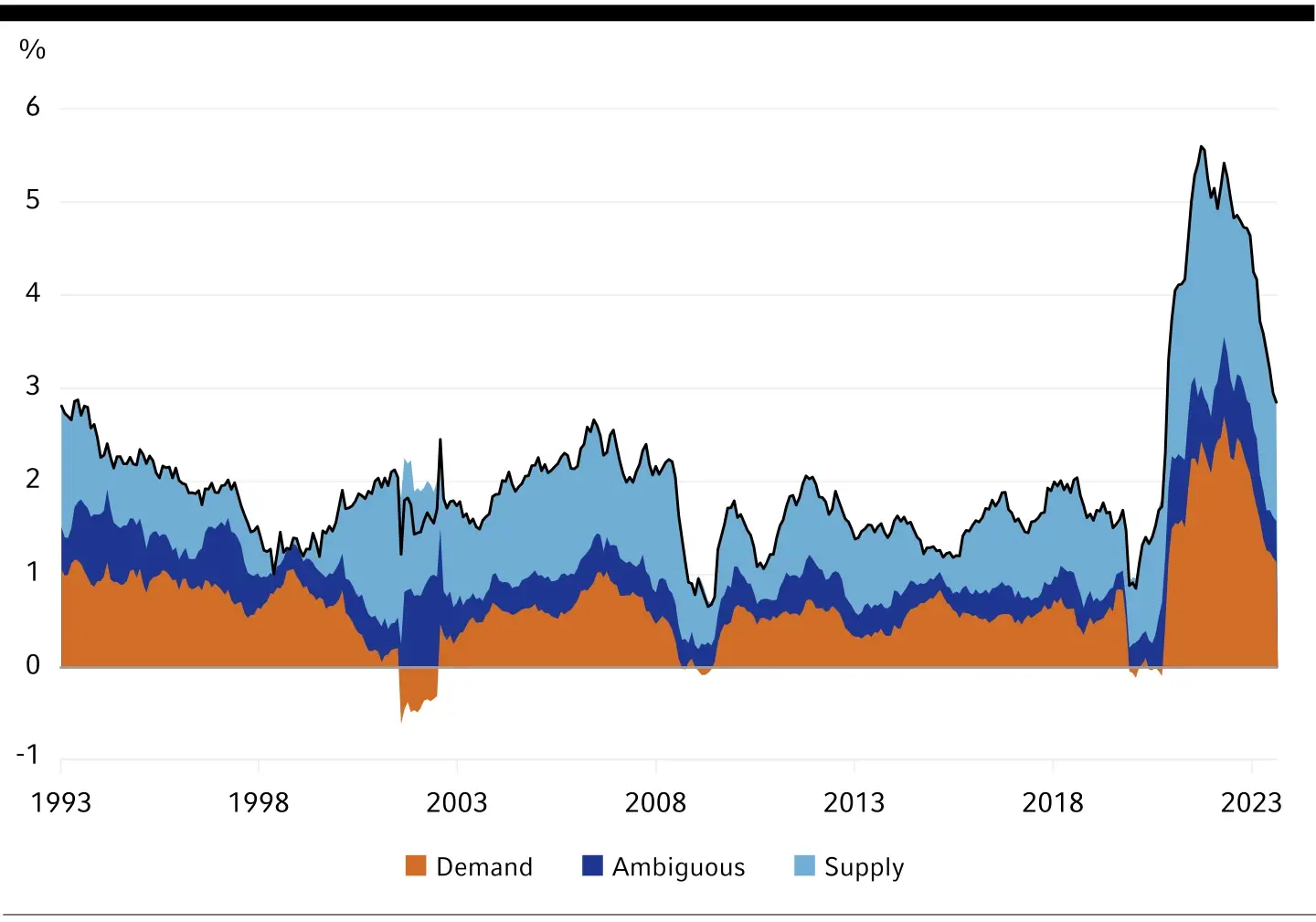

2022년 인플레이션 문제가 절정에 달했을 때 대부분의 경제학자들은 글로벌 경기 침체 가능성이 높으며 물가 안정을 회복해야 한다고 생각했습니다. 예를 들어 미국의 저명한 경제학자 래리 서머스(Larry Summers)는 1년 안에 인플레이션을 억제하려면 미국 실업률이 10%까지 상승해야 한다고 주장했습니다. 하지만 2023년에 인플레이션은 경기 사이클을 의미 있는 수준으로 훼손하지 않고 급격히 꺽였습니다. 완벽한 디스인플레이션(인플레이션 완화, immaculate disinflation)이었던 셈입니다. 이러한 디스인플레이션은 전 세계적으로 발생했지만, 특히 미국의 경우 추세 이상의 강력한 경제 성장에도 불구하고 물가와 임금 상승 압력이 약화되는 현상이 두드러졌습니다.

이는 매우 드물고 특이한 결과입니다. 높은 인플레이션은 주로 상품과 서비스 수요가 공급을 압도하기 때문에 발생합니다. 따라서 높은 인플레이션은 수요 감소, 공급 증가 또는 둘 다를 통해 억제될 수 있습니다. 중요한 것은 공급 증가는 과열된 경기가 비교적 고통 없이 균형을 되찾을 출구를 제공했으며, 실제 2023년 미국 디스인플레이션의 약 3분의 2를 주도한 것으로 나타났습니다.

차트 삽입 #1:

Source: LSEG DataStream, as of 29 February 2024.

미국의 인플레이션 완화에 도움이 된 요인은?

미국의 공급은 두 가지 방식으로 회복되었습니다. 첫째, 팬데믹 기간 동안 공장 봉쇄, 인력 부족, 해운 병목 현상 등으로 인해 전 세계적으로 악화되었던 상품 공급이 이제 대부분 회복된 것으로 보입니다. 이는 예상된 결과이긴 하나 그래도 여전히 반길 일이었습니다. 고무적인 것은 지난 8개월 동안 핵심 상품 가격이 하락했다는 점입니다. 둘째, 더욱 예상 밖의 사실은 은퇴 연령에 가까운 근로자, 장애인 근로자, 젊은 여성의 경제 활동 참가율 증가와 순 이민자 수 급증으로 노동 공급도 회복되었다는 점입니다. 이러한 노동 공급 회복은 대규모 해고 없이 임금 인플레이션을 억제하는데 도움이 되었는데, 이는 2차 세계 대전 이후 미국 역사상 처음 있는 일입니다.

전망 측면에서 미국 경제는 이제 훨씬 더 나은 균형을 유지하고 있으며, 대부분의 업계에서 추정하는 근원 인플레이션율은 3% 미만으로 둔화되었습니다. 또한 주택 인플레이션이 완화되고 향후 몇 달 동안 시의적절한 대안 임대료 조치에 따라 디플레이션이 더욱 강화될 수 있을 것으로 전망합니다. 인플레이션은 2024년 말 2~2.5%를 기록할 것으로 전망하며, 연준은 시간이 지남에 따라 점진적으로 정책을 보다 정상적인 환경으로 전환할 수 있을 것으로 예상합니다. 인플레이션 상방 리스크에는 억눌린 과열, 여전히 풀가동률에 가까운 경제, 우크라이나와 가자 지구 전쟁으로 인한 추가 공급망 차질 가능성 등이 있습니다. 인플레이션의 하방 리스크에는 경기 침체, AI 사용 증가에 따른 생산성 급증, 지속적인 노동 공급 회복이 포함됩니다. 중요한 것은 연준이 인플레이션 목표를 달성하고자 한다는 점이며, 이 목표에 따르면 실현 인플레이션(realized inflation)과 인플레이션 기대치가 중기적으로 2%에 가깝게 유지되어야 합니다.

“We think 2-2.5% inflation is in sight for year-end 2024.”

- Paul Eitelman, Chief Investment Strategist, North America.

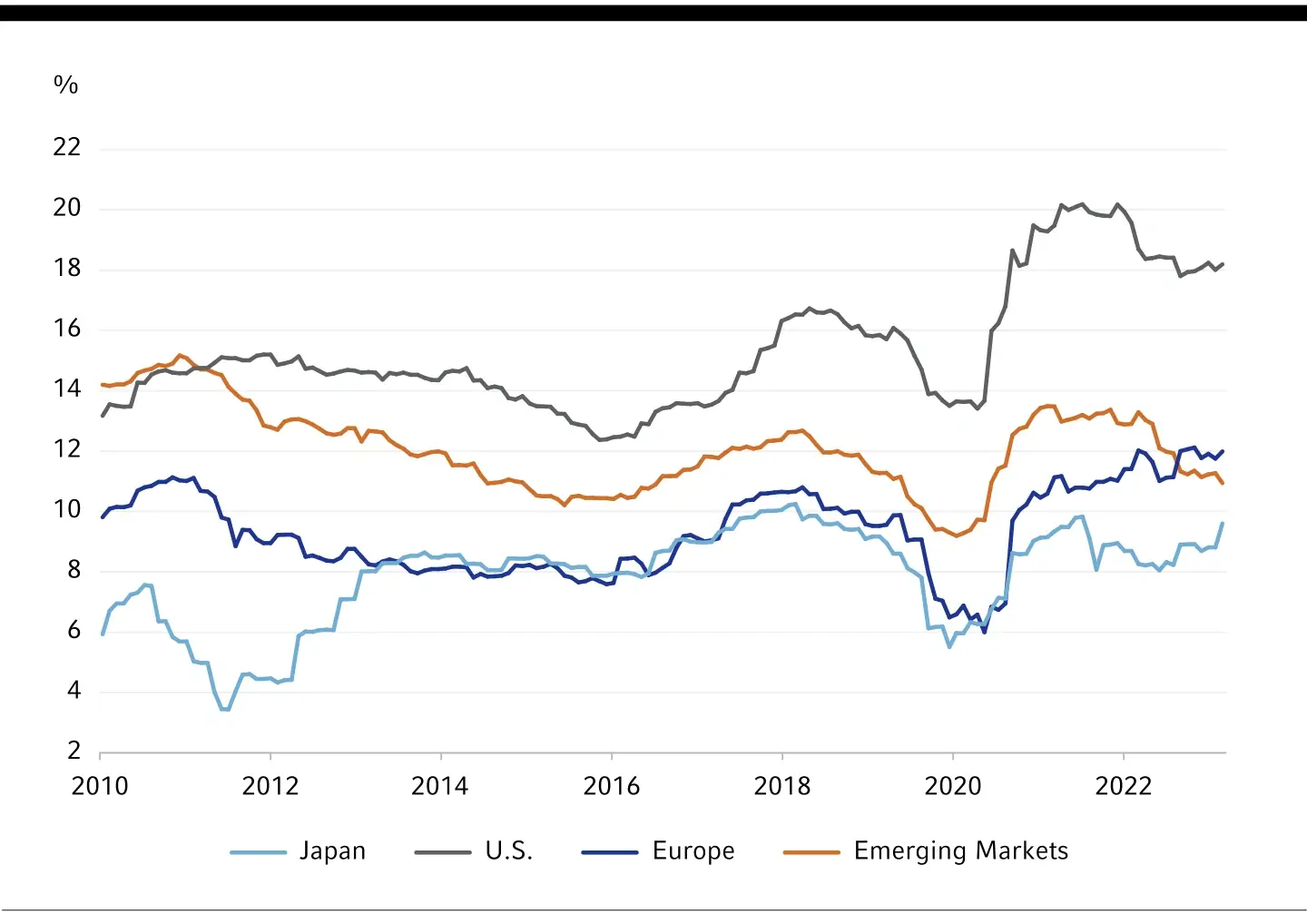

일본 기업의 부활

인플레이션 기대치와 임금 상승률이 상승하는 등 일본의 거시 환경이 변화하고 있습니다. 이러한 변화와 도쿄증권거래소의 이니셔티브가 더해지면서 일본 내 기업 행보에 변화가 일기 시작했습니다.

도쿄증권거래소는 장부가액 이하로 주가가 거래되는 상장 기업, 즉 순자산 가치보다 주식 가치가 낮은 기업을 대상으로 기업 가치 제고 방안을 제출하도록 요구했습니다. 처음에는 몇몇 기업들이 자사주 매입에 참여하여 주가를 장부가 근처로 끌어올리는 움직임이 일어났으나, 최근에는 인수합병 활동이 활발해지는 등 실질적인 개혁과 자기자본수익률(ROE)로 초점이 전환되고 있습니다.

아래 도표는 일본과 다른 주요 선진국 및 신흥국 시장의 ROE2 를 비교한 것으로, 최근 노력의 일부가 일본의 ROE 회복으로 결실을 맺기 시작했음을 확인할 수 있습니다. 이는 고무적인 신호이지만, 당사의 밸류에이션 모델에 따르면 이러한 '긍정적 소식'의 상당 부분이 이제 주가에 충분히 반영된 것으로 보입니다.

차트 삽입 #2:

결론: 일본 기업의 실적과 자기자본 수익률(ROE)이 도쿄증권거래소가 도입한 개혁 이니셔티브에 힘입어 회복세를 보이고 있습니다.

“Japanese corporate performance and return on equity are picking up.”

- Alex Cousely, Director, Senior Investment Strategist

지역별 현황

미국

미국 노동 공급이 놀라운 회복력을 보이면서 미국 경제는 균형을 되찾고 있습니다. 미 연준이 금리 인하를 서두르고 있지는 않지만 인플레이션 둔화로 인해 올해 중반부터 점진적인 금리 인하를 단행할 것으로 보입니다. 2024년 미국이 경기 침체를 피할 가능성은 높지만, 경제가 풀가동하는 상태에서 가계 저축이 감소하며 노동 시장이 둔화되고 미국 국채 수익률 곡선 역전 현상이 지속되는 등 경제 불확실성은 여전히 높습니다. 시장에는 다소 조심스러운 낙관론이 형성되어 있습니다. 현재 시장 가격은 경기 침체 가능성이 매우 낮다는 전망을 반영하고 있으며, 업계 컨센서스는 2024년 S&P 500 편입 기업들의 순익이 고무적으로 10% 증가할 것으로 예상합니다. 이러한 기대치는 달성 가능하지만, 투자자들의 낙관론 때문에 조심스러운 비대칭성이 초래되기 쉬우며 이 경우 포트폴리오 다각화가 핵심일 것입니다. 현재 수익률 곡선을 고려할 때 미 국채의 밸류에이션은 여전히 매력적입니다.

유로존

유로존의 각종 경제 지표는 예상외로 호전되고 있으며, 근원 인플레이션은 유럽중앙은행(ECB)의 목표치인 2%에 근접하고 있습니다. 에너지 가격 하락, 가계의 실질 임금 상승, 글로벌 제조업 활동 회복으로 성장률이 탄력을 받고 있습니다. 은행 대출 회복은 다음 분기에도 긍정적인 경제 모멘텀이 유지될 수 있음을 시사합니다. 유럽중앙은행의 긴축 정책이 시차를 두고 경제에 영향을 미치면서 연말에는 성장률이 둔화될 것으로 예상되지만, 경기 침체가 심화될 위험은 감소하고 있습니다. 유럽중앙은행은 근원 인플레이션 하락 추세에 대응하여 6월 금리 인하를 시작할 수 있다고 시사했으며,통화 완화 정책은 경기 둔화 여파를 완충하는 데 도움이 될 것입니다.

인공지능(AI) 테마주가 S&P500 지수 상승을 견인한 것과 달리 유럽 주식의 경우 AI 수혜주가 부족하지만, 미국에 비해서는 가격 측면에서 저렴합니다. 올해 유럽 증시 편입 기업들의 주당순이익(EPS) 성장률이 2.8%에 그칠 것이라는 비교적 부진한 시장 컨센서스를 상회할 수 있다면 유럽 증시에도 수혜가 기대됩니다.

영국

영국 경제 전망은 여전히 밝지 않습니다. 국내총생산(GDP) 성장은 정체되어 있고 인플레이션은 다른 선진국보다 느린 속도로 하락하고 있습니다. 시장 전문가들은 영란은행이 3분기 금리 인하를 단행하기 시작할 것으로 전망합니다. 금리가 내리면 다소 경제 숨통은 트이겠으나, 2~5년 고정 금리 모기지 금리 상승에 따른 여파는 시차를 두고 반영될 것입니다.

최근 여론 조사에서는 키어 스타머(Keir Starmer) 당수가 이끄는 야당 노동당이 앞서고 있어 연말 이전 치러질 총선에서 노동당이 집권할 가능성이 있습니다. 현 보수당 정부가 여론조사 지지율을 끌어올리기 위해 일부 세금을 인하했지만, 이러한 정책은 통화 정책과 반대 방향이므로, 결과적으로 영란은행의 통화 정책 완화 시기를 지연시킬 위험이 있습니다.

현재 채권 시장에는 영란은행이 올해 2~3차례 25bp의 금리 인하를 단행하리라는 예상이 반영되어 있지만, 약화된 영국 경제 기초 체력을 감안할 때 인하폭이 커질 수 있다고 생각합니다. 영국의 10년물 수익률은 4.1%로 매력적입니다.

일본

당사는 올해 남은 기간 동안 일본이 현 추세 수준의 성장세를 이어갈 것으로 전망합니다. 현재 일본의 임금 상승률과 인플레이션 기대치가 일본은행(BoJ)의 인플레이션 목표치와 일치하는 수준으로 움직이고 있습니다. 이에 따라 일본은행은 2024년 전체에 걸쳐 서서히 정책을 정상화할 수 있을 것으로 예상됩니다. 시장에서는 일본은행이 올해 금리를 0.4% 인상할 것으로 예상하나, 글로벌 통화 완화 기조로 인해 예상이 빗나갈 수도 있습니다.

일본 증시가 지난 6개월 동안 상승 행진을 이어간 데 따라 당사의 밸류에이션 모델 전반에 걸쳐 고평가 신호가 감지됩니다. 일본은행이 채권 매입을 줄이고 정책 금리를 점진적으로 인상함에 따라 올해 채권 수익률은 상승 압력을 받을 것으로 예상합니다. 일본 엔화는 매우 저렴해 보이지만 미 연준이 금리를 인하하거나 글로벌 경제가 둔화되기 전까지는 크게 절상될 가능성은 낮습니다.

중국

중국은 2024년 GDP 성장률 목표를 약 5%로 발표했습니다. 작년과 달리 팬데믹 이후 리오프닝 특수 효과가 사라졌기에 5% 성장률 목표는 달성하기는 어려울 것으로 예상됩니다. 중국 정부의 재정 정책은 제한적인 지원만 제공하고 있지만, 5% GDP 성장 목표가 위협받는다면 더 많은 조치가 시행될 수 있습니다. 중국의 디플레이션 고착화 조짐과 함께 소비 시장 체력이 주요 관전 포인트가 될 것입니다.

중국 주식은 주가수익배수 10배 미만에서 거래될 정도로 저렴합니다. 당사의 센티먼트 모델에 따르면 중국 증시는 높은 과매도 국면에 있지만, 최근 반등 이후 과매도 정도는 다소 완화되었습니다. 애널리스트들은 중국 경제가 리플레이션(reflation)에 접어들고 성장 모멘텀을 회복한다면 올해 15%의 순익 성장을 달성할 수 있을 것으로 예상하고 있습니다.

캐나다

캐나다는 경기 침체를 피했지만 성장세는 여전히 부진하며, 향후 12~18개월 동안 경기 침체에 진입할 가능성이 높다고 생각합니다. 2023년 3분기 GDP 성장은 위축되었으며 연평균 성장률은 약 1.0%로 잠재 성장률3 인 약 2%를 밑돌았습니다. 2024년의 예비 추정치에 따르면 GDP는 플러스 성장을 향해 나아가고 있습니다.

캐나다 중앙은행(BoC)은 경제적 어려움을 인식하고 있으며 금리가 충분히 긴축적이라고 밝혔습니다. 그러나 캐나다 중앙은행은 정책 금리를 인하하기 전에 인플레이션이 지속적으로 2% 목표를 향해 나아가고 있음을 보여주는 지표를 기다리고 있습니다. 금리 인하를 너무 늦추면 경기 침체의 위험이 있고, 섣불리 단행하면 주택 시장과 인플레이션을 부채질할 수 있기에 섬세한 균형을 잡는 것이 중요합니다. 그럼에도 불구하고 올해 중반에는 캐나다 은행이 목표 금리 인하를 시작할 근거를 확보할 것으로 예상됩니다.

캐나다의 GDP와 고용 추세가 약세를 보이고 있다는 점을 고려할 때, 연말까지 시장에서 전망하는 캐나다 은행과 미 연준의 금리 인하 기대치가 비슷하다는 것은 당혹스러운 일입니다. 당사는 결국 캐나다은행이 미 연준보다 더 큰 폭으로 금리를 인하할 것으로 예상합니다. 향후 경제 전망에 근거해 캐나다 국채는 선호하지만, 경기 순환 측면 때문에 캐나다 주식에 대해서는 신중한 포지션을 유지하고 있습니다.

호주 및 뉴질랜드

호주 경제는 추세 이하의 성장세를 이어갈 것으로 예상하지만 적어도 경기 침체는 피할 수 있을 것으로 예상합니다. 임금 상승률은 완만해지고 있으며 인플레이션은 호주중앙은행(RBA)의 전망치보다 낮습니다. 노동 수요는 둔화되고 있으며, 높은 이민 수준으로 인해 노동 공급 증가율이 높아지고 있습니다. 주택 시장은 기준 금리 인상에도 불구하고 회복 탄력성을 유지해 왔으며, 이러한 추세는 지속될 것으로 예상합니다. 호주중앙은행(RBA)은 여타 선진국 중앙은행보다 늦은 시점인 3분기 말에 가서야 첫 금리 인하를 단행할 것으로 예상합니다.

호주 주식 밸류에이션은 미국에 비해 저렴하지만 다른 선진국 시장과 비슷한 수준입니다. 호주 국채는 미국 국채보다 낮은 수준에 거래됨에도 불구하고 여전히 밸류에이션이 매력적입니다. 호주 달러는 금리차 개선에 힘입어 올해 상승세를 보일 것으로 예상됩니다.

뉴질랜드 경제는 호주보다 더 큰 압박을 받아왔는데, 이는 뉴질랜드 중앙은행(RNBZ)이 더 긴축적인 통화 정책을 펼쳤기 때문입니다. 단, 기업 신뢰 지수가 상승하고 있고 뉴질랜드 중앙은행이 금리 인상 사이클이 마무리 단계라는 신호를 보냈다는 점은 긍정적인 조짐입니다.

뉴질랜드 주식은 호주 및 해외 주식에 비해 고평가된 것으로 보입니다. 뉴질랜드 채권은 가격이 적정한 수준이며 경제가 더 심각하게 둔화되고 뉴질랜드 중앙은행이 더 공격적으로 금리를 인하해야 할 경우 상승 여력이 있습니다.

“European indexes lack the AI-themed stocks that have boosted the S&P500, but are cheap relative to the U.S.”

- Andrew Pease

자산군별 선호도

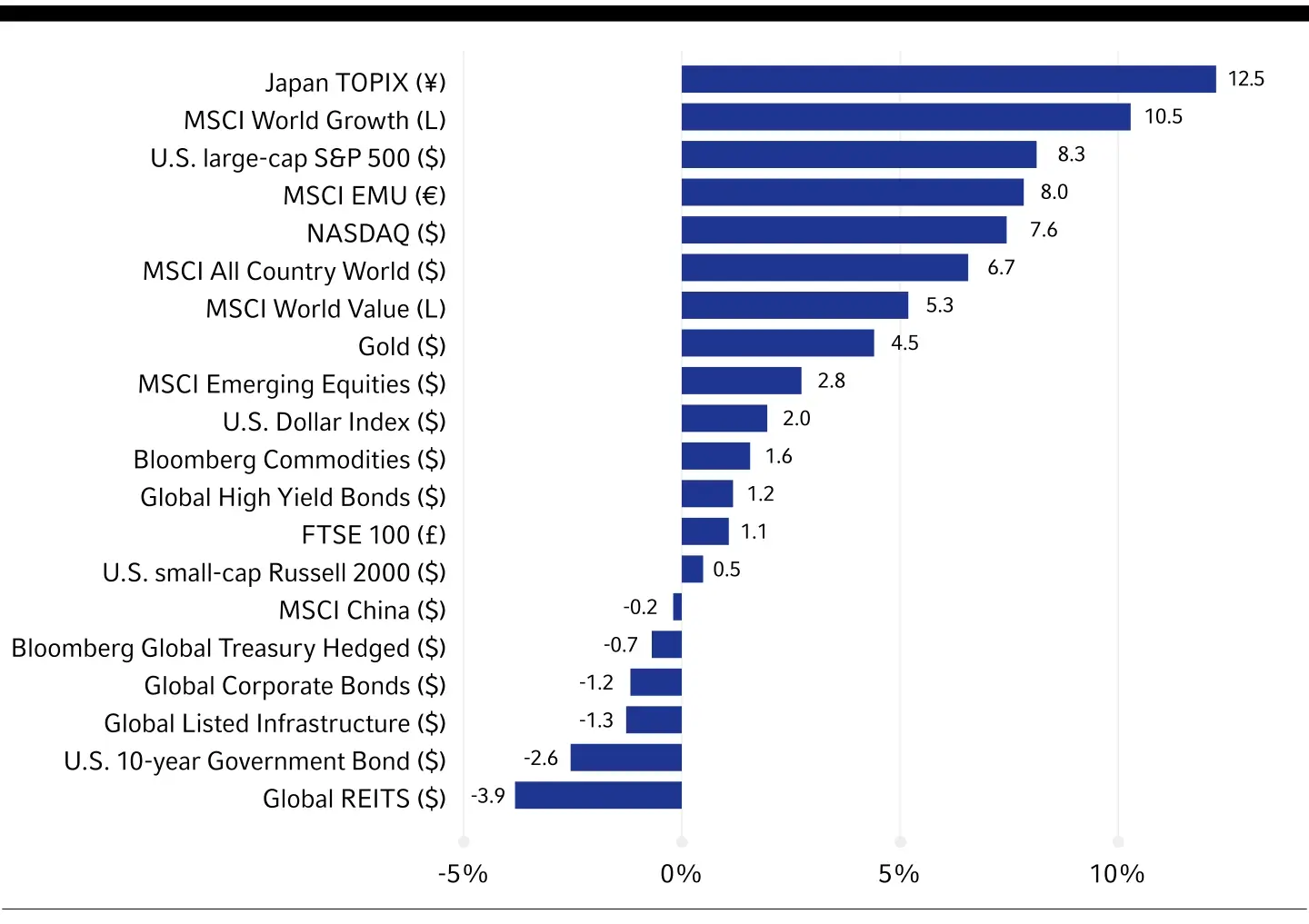

2024년은 일본, 유럽, 미국 전반의 주식 시장 수익률이 강세를 보이면서 다시 시작되었습니다. 미국 증시에서 7대 기술주, 즉 매그니피센트 74 의 상승률은 기준 지수를 지속적으로 앞서고 있지만, 이들 그룹 가운데서도 수익률은 엇갈리고 있습니다. 예를 들어 올 들어 3월 14일까지 테슬라는 35% 하락한 반면 엔비디아는 78% 상승했습니다. 미국 소형주 실적을 측정하는 Russell 2000® 지수는 2022년 정점 대비 17% 하락한 상태로 올 들어 보합권에서 등락하고 있습니다. 중소기업은 금리 상승의 직격탄을 맞고 전반적으로 수익성이 약해진 탓입니다. 한편, 글로벌 투자자들이 중국 당국의 조심스러운 정책 대응과 부동산 시장 우려로 중국 시장에 대해 관망세로 돌아서면서 중국은 여전히 신흥국 시장의 발목을 잡고 있습니다.

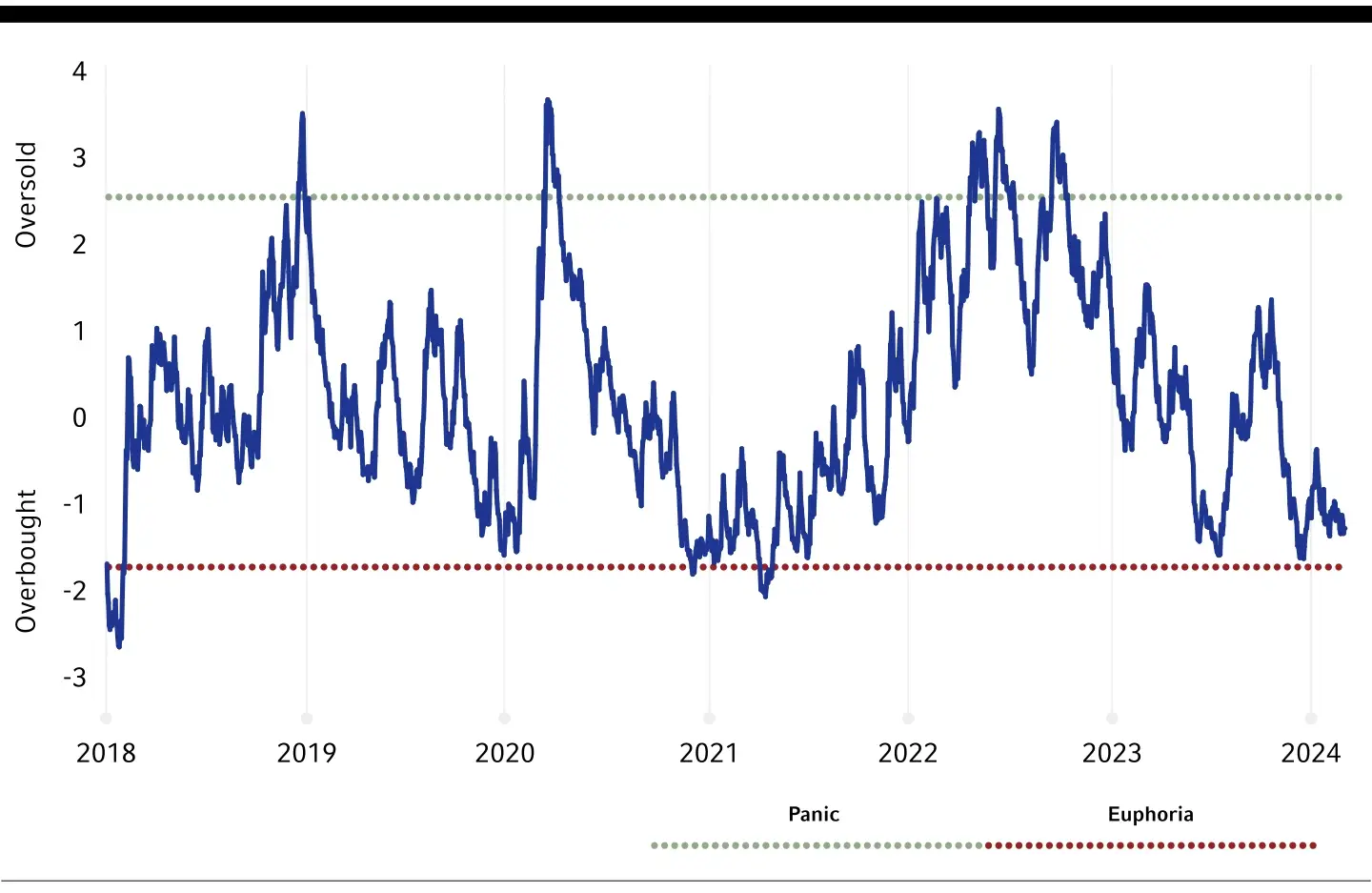

차트 삽입 #3:

당사의 사이클, 가치, 센티먼트(CVS) 투자 의사 결정 프로세스는 다가올 한 해 시장에 대해 여전히 다소 신중한 입장입니다. 투자자들이 직면한 다양한 잠재적 시나리오에 대응하기 위해서는 상장된 실물 자산과 사모 시장을 통한 선별적인 분산 투자가 전통적인 포트폴리오 자산 배분을 보완하는 데 중요한 역할을 담당할 것으로 보입니다.

특히 미국의 경우 상장 주식의 주가 배수(multiple)는 비싸며 기업 신용 스프레드(금리 격차)는 축소되어 있습니다. 또한, 높은 밸류에이션은 위험자산에 대한 전망을 약화시키고 있습니다. 국채 수익률은 여전히 예상 인플레이션을 상회하는 수준이므로 국채 밸류에이션은 매력적인 수준이라고 생각합니다.

경기 사이클 전망

미국 경제가 균형을 되찾고, 글로벌 제조업 사이클이 긍정적인 변곡점에 달했다는 초기 징후가 나타나며 유럽 경제 전망도 밝아지고 있으며, 최근 일본의 밸류업 정책에 따른 자기자본 수익률 개선 등에 힘입어 이번 분기에는 글로벌 경기 사이클 전망은 긍정적입니다. 미국이 2024년 경기 침체를 피할 가능성은 높다고 생각하지만 불확실성은 여전히 높으며 시장은 최근 몇 달간 긍정적인 뉴스의 전부는 아니더라도 대부분을 가격에 반영했습니다.

당사의 독자적인 투자자 심리 지수에 따르면 3월 중순 현재 대부분의 투자자들이 낙관적인 시장 심리를 보이고 있습니다. 현재의 심리 지수는 시장의 하방 비대칭 가능성에 무게를 실어주지만, 포트폴리오에서 상당한 위험 회피 포지션이 적절하다고 판단할 만큼 지속 불가능한 극단 수준은 아닙니다.

차트 삽입 #4:

종합 역(逆)투자 지표:

투자 심리가 다소 과매수 국면에 들어셨지만, 아직 극도의 낙관론 구간은 아닙니다.

출처: Russell Investments. 마지막 관측치는 2024년 3월 11일 기준 표준편차는 -1.4입니다. 투자자 심리를 보여주는 대한 종합 역(逆)투자 지표는 중립 수준 상회 또는 하회 표준편차로 측정됩니다. 양수 값은 투자자 비관론 신호에 해당하고 음수 값은 투자자 낙관론 신호에 해당합니다. 이 차트는 투자 센티먼트가 과매수되었음을 보여 주지만, 아직 극도의 낙관론(euphoric extreme) 구간은 아닙니다.

전반적으로 당사의 CVS(사이클, 가치, 센티먼트) 투자 의사 결정 프로세스에 근거할 때 다소 신중한 편이지만, 포트폴리오를 현저하게 리스크 온 또는 리스크 오프에 포지셔닝할 정도로 극단적인 시장 상황은 보이지 않습니다. 대신 2024년 2분기 초 대부분의 포트폴리오 전략은 내년의 다양한 잠재적 시나리오에서 고객 성과를 보호하기 위한 종목 선택과 다각화에 중점을 두고 있습니다.

- 증시 전망은 높은 밸류에이션, 실적 성장에 대한 업계 컨센서스 낙관론, 과매수 심리 등으로 상승폭이 제한적일 것으로 보입니다. 당사는 이전에 재무상태가 양호하고 수익성이 좋은 Quality 팩터 주식을 선호했지만, 최근 연이은 급등세에 따라 2월 해당 종목에 대한 포지션을 비중 확대에서 중립으로 전환했습니다.

- 당사의 포트폴리오 전략은 주요 증시 전반에 걸쳐 중립입니다. 미국 이외 선진국 주식은 여전히 미국 주식에 비해 저평가되어 있지만, 이들 시장에서 차별화된 수익을 낼 수 있을지에 대해서는 상당한 불확실성이 존재합니다. 중국 증시는 최근 몇 년간 급격한 하락세를 보였습니다. 중국 증시의 경우, 지수는 장부가 수준에서 거래되고 많은 종목이 대차대조표상의 현금성 자산 수준에서 거래되는 등 매우 저렴합니다. 당사의 독자적인 시장 심리 지표에 따르면, 중국 증시에 대한 투자 심리는 극단적 비관론 상태이며, 이는 시장 전망에 있어 긍정적 신호입니다. 그러나 중국 시장은 여러 구조적 문제와 소비 심리 위축 국면에 직면해 있으며, 지금까지 발표된 중국 당국의 경제 및 시장 부양 정책은 조심스러운 수준에 그쳤습니다. 주식 포트폴리오 전략 전반에 있어 당사는 중국 시장에 대해 중립에서 다소 비중 확대 포지션을 유지하고 있습니다. 비중 확대 포지션의 경우, 하위 운용사의 이머징 마켓 내 어느 부문에서 최고의 가치를 발견하느냐에 따라 주로 결정됩니다.

- 국채 수익률은 여전히 예상 인플레이션을 상회하는 수준이므로 국채 밸류에이션은 매력적인 수준이라고 생각합니다. 현재 시장은 부정적인 경제 시나리오 가능성에 큰 무게를 두고 있지 않습니다. 따라서 선진국 시장 경제가 둔화되거나 경기 침체에 빠지면 각국 중앙은행이 현재 선물 수익률 곡선에 반영된 금리보다 더 공격적으로 금리 인하를 단행할 것으로 예상됩니다. 미국 국채는 채권 전략팀에서 선호하는 비중 확대 포지션으로, 특히 수익률 곡선 5년 지점의 밸류에이션이 매력적으로 판단됩니다. 또한 향후 몇 년 동안 더 공격적인 금리 인하가 이루어질 경우 수익률 곡선이 다시 가팔라질 가능성도 있습니다. 캐나다, 독일, 호주, 영국을 포함한 대부분의 주요 선진국 국채에 대한 긍정적 전망은 여전히 유효합니다. 유일하게 주목할 만한 예외는 여타 국가들과 달리 수익률이 침체된 일본입니다.

- 경제적 불확실성이 높아지는 상황에서 미국 하이일드(고위험) 회사채와 투자 등급 회사채 사이의 스프레드가 축소되어 여느 때와 달리 회사채에 대한 전략적 비중 확대 전략을 취하기가 꺼려집니다.

- 선진국 중앙은행이 2024년에 금리를 인하할 것이라는 전망은 부동산에 큰 호재가 될 것입니다. 부동산 투자 신탁(REIT) 밸류에이션은 계속해서 매력적으로 보입니다. 거시 전망을 둘러싼 상당한 불확실성을 감안할 때 인프라 투자의 방어적 특성 덕분에 인프라 부문은 포트폴리오 다변화의 유용한 수단이 될 수 있다고 생각합니다. 시장 침체기에 포트폴리오를 완충하는 동시에 연착륙 시 상당한 상승 잠재력을 포기하지 않을 수 있기 때문입니다. 유가는 성장 둔화세와 석유수출국기구(OPEC)+ 산유국 그룹의 공급 제약 사이의 줄다리기가 계속되면서 박스권에서 등락을 거듭할 수 있습니다. 사상 최고가에 근접한 금은 현재 실질 수익률에 비해 고평가된 것으로 보입니다. 올해 말 금값이 약세를 보일 수 있지만 경기 침체 리스크 상승, 실질 금리 하락 가능성, 지정학적 긴장 고조, 중앙은행의 금 매입에 따른 구조적 지지 등 여러 요인이 사이클상 여전히 금에 유리한 환경을 조성하며 가격 하락세를 완화할 수 있습니다.

- 미 달러는 현재 상당히 고평가되었으며 중기적으로 하락할 가능성이 있습니다. 다만 2024년 글로벌 경기 침체 가능성으로 인해 상대적으로 안전한 미국 자산으로 자금이 몰릴 경우, 단기적으로 달러화 가치는 추가 상승할 수 있습니다. 이처럼 상반된 리스크를 감안하여 우리는 미 달러에 대해 중립 포지션이 적절하다고 생각합니다.

- 공적 신용 수익률이 축소된 상황에서도 사모 신용(private credit) 수익률은 여전히 높기 때문에 사모 신용에서 매력적인 수익 기회가 창출되고 있습니다. 사모 신용의 금리 하한은 중앙은행이 금리 인하를 시작하더라도 변동 금리 사모 신용의 수익률을 보존하는 데 도움이 될 수 있습니다. 거시 경제 불확실성이 높아지면서 사모 신용 펀드 간에 수익률이 엇갈릴 가능성이 높으며, 실사 프로세스가 가장 탄탄한 펀드 매니저가 더 좋은 성과를 거두기 쉬울 것입니다. 저금리에 대한 낙관론과 연착륙 전망에 따른 인수합병 활동 증가는 사모 펀드가 더 많은 양질의 투자를 유치하는 데 도움이 될 것입니다. 동시에 기업공개(IPO) 시장이 개선되면 사모펀드에 더 나은 투자금 회수 기회를 제공할 수 있으며, 유한 파트너에게 배분되는 배당도 증가할 수 있습니다.

“Our cycle, value, and sentiment (CVS) investment decision-making process is still slightly cautious toward markets for the year ahead.”

- Paul Eitelman

Prior issues of the Global Market Outlook

1 라파엘 보스틱 총재는 2024년 3월 4일 비즈니스 리더들이 미국 연방준비제도(Fed)의 금리 인하 힌트가 나오자마자 “뛰어내릴(pounce)”준비가 되어 있다며 억눌린 과열이라고 표현한 이 위협은 앞으로 몇 달 동안 면밀히 주시해야 할 새로운 상방 리스크”라고 밝혔습니다.

2 자기자본수익률(ROE)이란 투자자에게 회사 경영진이 주주가 회사에 투자한 자금을 얼마나 효율적으로 운용하고 있는지에 대한 통찰력를 제공하는 수치입니다. 즉, ROE는 주주가 갖고 있는 지분에 대한 기업의 이익 창출 정도를 나타냅니다. ROE가 높을수록 기업 경영진이 자기자본 조달을 통해 수익과 성장을 창출하는 데 더 효율적이라는 뜻입니다.

3 잠재 성장률이란 경제에 있어 지속 가능한 성장률의 근사치입니다. 잠재 성장률은 대략 장기적인 생산성 성장률에 노동력 증가율을 더한 값으로 계산됩니다.

4 ‘매그니피센트 7’이라는 용어는 7대 기술주 (마이크로소프트, 애플, 알파벳, 아마존, 엔비디아, 메타, 테슬라)를 지칭합니다.