Executive summary:

- In a closely watched decision, the U.S. Federal Reserve opted for a larger 50-bps reduction in interest rates today, rather than a more traditional 25-bps rate cut.

- Today’s rate cut marks a clear shift in the Fed’s focus from taming inflation to protecting the U.S. labor market and the economic expansion.

- We expect the Fed to cut rates by 25 basis points at each of its remaining meetings in 2024 and to sustain that pace into 2025. This trajectory would get the Fed down to our estimate of the normal or equilibrium rate of interest of 3%-3.25% this time next year.

Today’s U.S. Federal Reserve (Fed) decision was more consequential than normal for two reasons.

First, it marked the start of the long-awaited easing cycle with the central bank shifting its focus away from inflation risks and toward protecting the U.S. labor market and economic expansion. While the Fed’s track record in achieving such a soft landing is checkered, it’s an important change and a friendlier monetary policy backdrop for financial markets than, for example, early 2022, when team Powell was explicit in its willingness to inflict damage to bring inflation back under control.

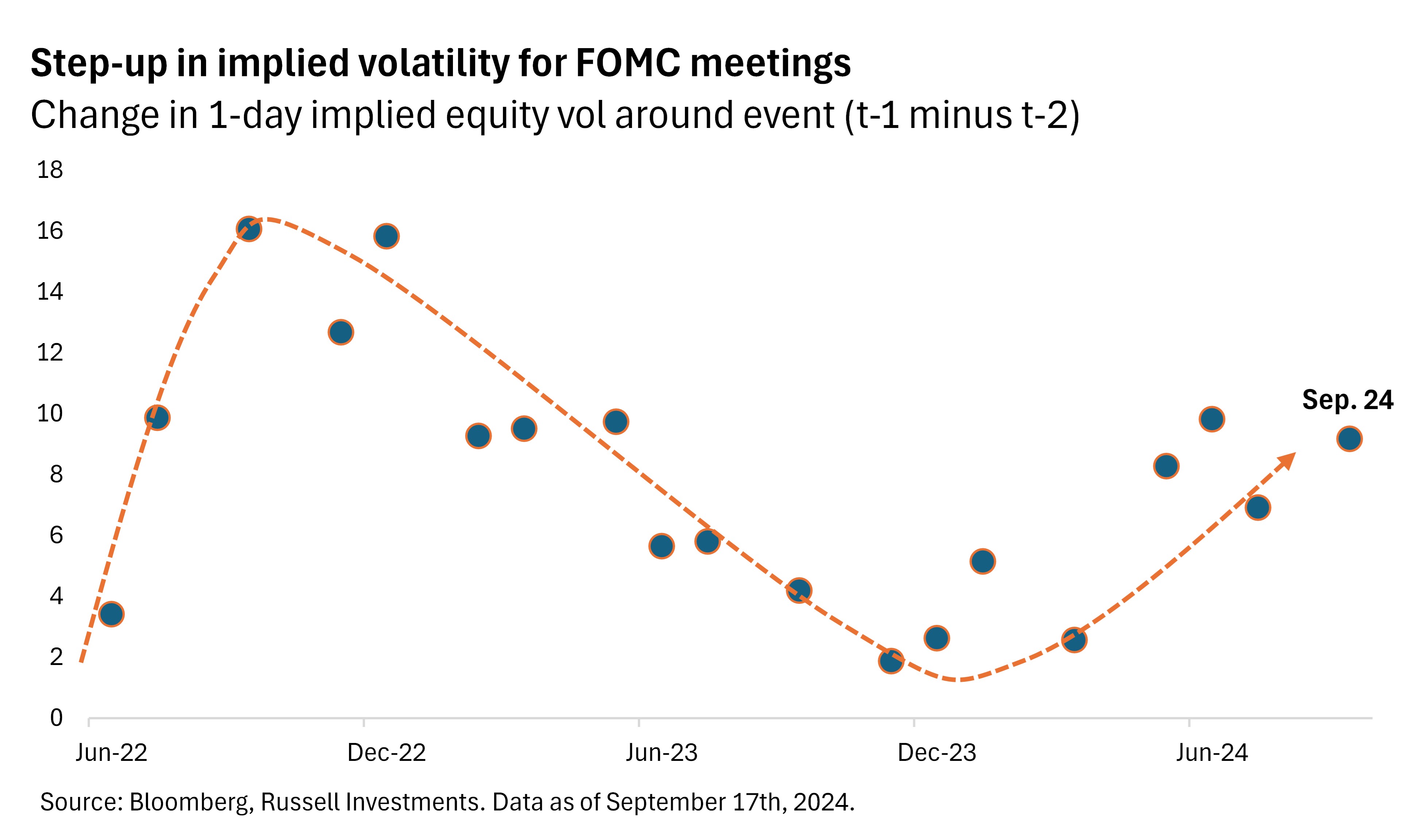

Second, the interest rate decision itself—whether to cut by 25 or 50 basis points (bps)—was MUCH more of a nailbiter than normal. Fed doctrine from Greenspan to Bernanke to Yellen to Powell has trended toward greater transparency in its decision-making and a preference to not surprise financial markets or the general public. Put differently, we almost always know what the Fed is going to do because it tells us what it's going to do. For a range of reasons that was not the case today, with financial markets pricing the 25 vs. 50 decision at an effective coin toss in the hours ahead of the decision—at 45% and 55%, respectively.

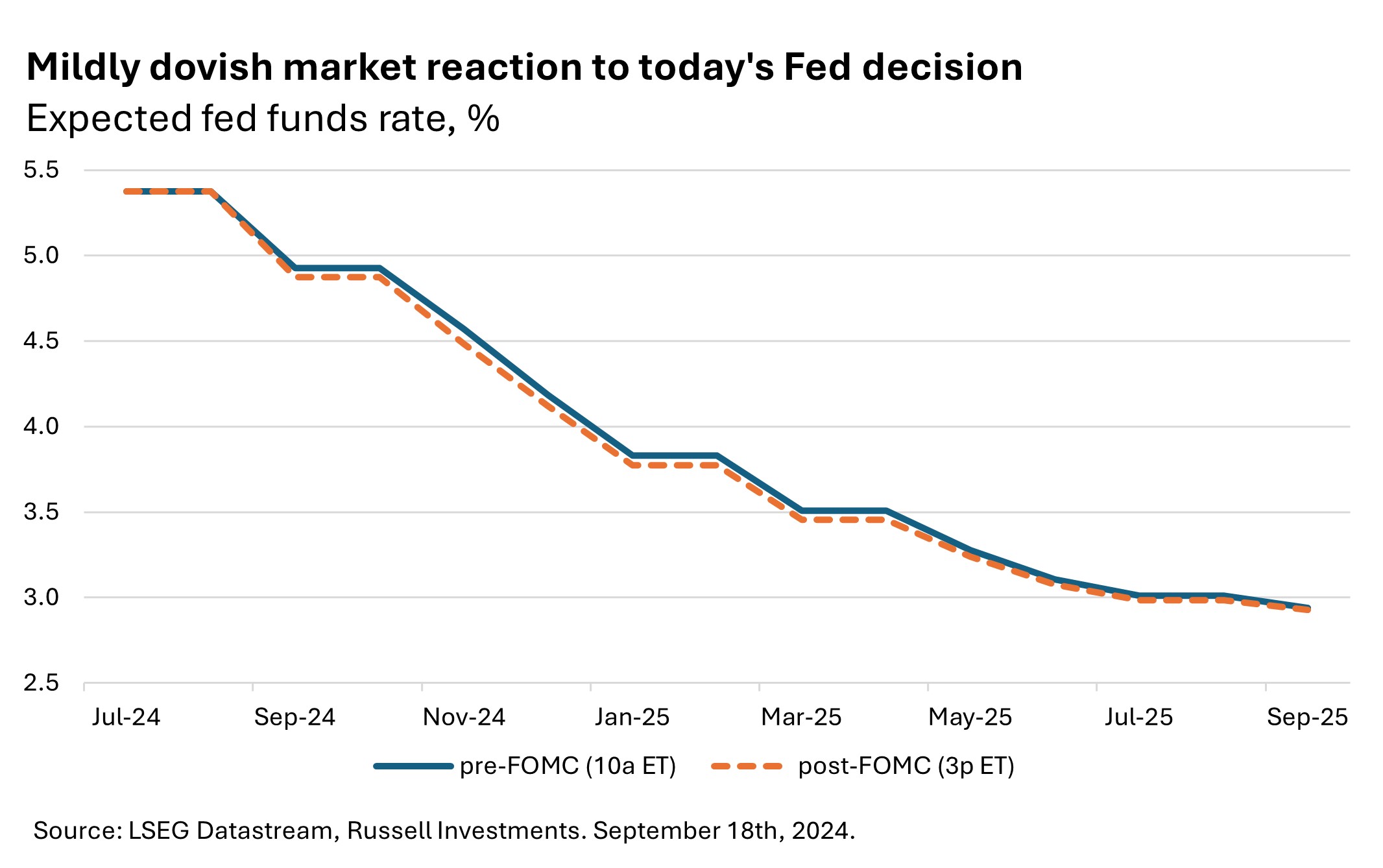

Ultimately, the Fed decided to go with a larger, 50-basis-point rate cut today. The move should help the Fed normalize rates more quickly and get ahead of the emergent slowing in the labor market. Notably, however, the Fed’s forecasts (the dots) don’t show a 50-basis-point pace continuing beyond September. Almost all of the FOMC (Federal Open Market Committee) participants baselined one to two additional rate cuts through the end of 2024. Note: there are two Fed meetings remaining on the calendar for this year. U.S. equities and Treasury yields were little changed on the news, likely reflecting the tension between the front-loaded rate cut and a path that was lower but slower thereafter.

Implications for the economic outlook

We believe that inflation is likely to moderate toward the Fed’s 2% target in early 2025. And on that basis, it’s time for the Fed to get out of the way of a sustained expansion. Today’s jumbo-sized cut was an important step in that direction. But the verdict is still out on whether the U.S. economy will slow toward a soft or hard landing. A key risk is the slowdown in hiring. While nonfarm payrolls are still positive, they have not been sufficient to absorb incremental labor supply in recent months (e.g., college graduates and immigrants) and the unemployment rate has risen notably, breaching the so-called Sahm Rule. But there are important areas of resilience, too. The services sector continues to chug along, layoffs remain low, and corporate earnings are improving and broadening. That fundamental resilience argues against a layoff cycle emerging in the months ahead, which is often what catalyzes a non-linear break in the labor market and consumer spending. Our economic outlook continues to be glass half full—optimistic into high uncertainty.

We expect the Fed to cut rates by 25 basis points at each of its remaining meetings in 2024 and to sustain that pace into 2025. This trajectory would get the Fed down to our estimate of the normal or equilibrium rate of interest of 3%-3.25% this time next year. Importantly, the bigger rate cut today echoes Chair Powell’s comments from Jackson Hole that the Fed will continue to respond forcefully to any additional weakness in the labor market going forward.

Implications for markets

Today’s decision was important for fixed income markets, as it helped resolve some of the uncertainty about the near-term Fed path. Empirically, we find the biggest excess returns to holding Treasury duration relative to cash come in the months BEFORE the Fed actually starts cutting rates. Consistent with this observation, we had an overweight preference to duration in most of our multi-asset and fixed income portfolio strategies in recent months, and have shifted toward taking profits on that positioning in recent weeks as market pricing moved on top of our more dovish expectations for the Federal Reserve. In the months after the Fed starts cutting rates, returns to duration have tended to moderate toward long-term historical averages. That is, at least in part, because the potential for markets to be surprised diminishes as the central bank builds a rhythm around its easing cycle. Similarly, we no longer view Treasuries to be a compelling overweight opportunity today with yields across the curve trading near our estimates of fair value.

The implications for Fed rate cuts onto equities hinges critically on the fundamental backdrop—namely, corporate earnings and whether the economy is slowing toward a soft or hard landing. While our baseline is for a soft landing going forward, we think high uncertainty across these scenarios argues for maintaining modest sector, style, and region exposures. If a soft landing can be achieved, we would expect the combination of lower rates and resilient fundamentals to benefit areas of the market like real estate and small caps. For small caps, in particular, we see a ripe environment for skilled active managers to identify quality businesses at more attractive valuations.