Executive summary:

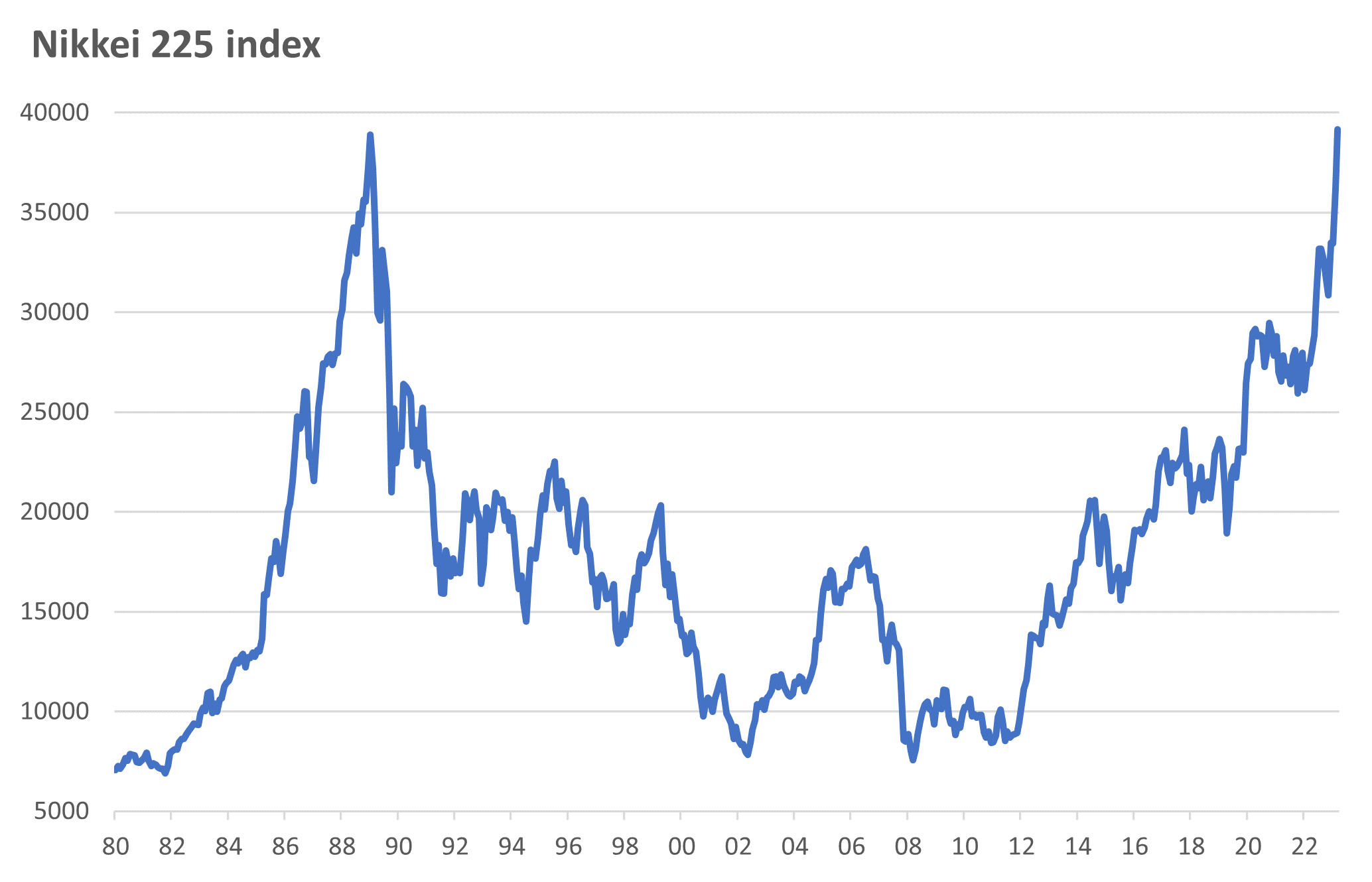

- Japan’s equity benchmark, the Nikkei 225 Index, has been on a tear in 2024, eclipsing its previous high set back in 1989. As of early April, the index is hovering near 40,000.

- Solid economic growth, a revamp in the country’s tax-free stock investment program and corporate governance reform have helped propel Japanese equities to record highs.

- We believe Japanese equities still have room to climb further due to a positive cyclical backdrop and improvements in corporate governance.

Japan has had two big moments in the last month, with the Nikkei 225 equity index breaking above the highs set in 1989, and the Bank of Japan (BoJ) raising interest rates for the first time in 17 years. We think that the Japanese economy is in a decent place and expect that the corporate governance reforms spearheaded by the Tokyo Stock Exchange will remain a tailwind. Moreover, we expect the Bank of Japan’s path forward for more rate hikes to be limited, given our view that many developed central banks are likely to start cutting rates in the second half of the year.

So, what’s behind the recent strength in the country’s economy and equity market?

Let’s unpack this all by starting with a step back in history to 1989.

What powered Japanese equities to record highs in the 1980s?

In 1989, George H. W. Bush had been sworn in as U.S. president, Baywatch and The Simpsons were airing on television for the first time, and golf club memberships in Japan were up by an estimated 190% from the year prior.1 Meanwhile, the Japanese equity market was coming off a run of very strong returns, having risen 465% from September 1982 to the end of 1989. This occurred amidst a rapid rise in asset prices more generally, spurred by rapid lending by Japanese banks. Toward the end of 1989, the Bank of Japan sharply increased interest rates, which triggered a rapid decline in asset prices (including equities) and led to two decades of weak economic performance.

(Click image to enlarge)

Source: LSEG Datastream, 20 March 2024

Source: LSEG Datastream, 20 March 2024

3 key factors behind today’s record-setting market

Fast forward to today, where the Nikkei Index is hovering around 40,000 after besting the 1989 record of 38,915 in late February.2 What’s fueling this? We believe there are three key factors at play. The first is Japan’s solid economic backdrop and the return of inflation expectations. The second is the revamping of the government’s NISA (Nippon Individual Savings Account) scheme, which is allowing Japanese individuals to invest in equities in a tax-efficient manner. Finally, there are signs that corporate governance reforms are starting to bear fruit.

Factor #1: Japan’s economic growth is boosting corporate earnings

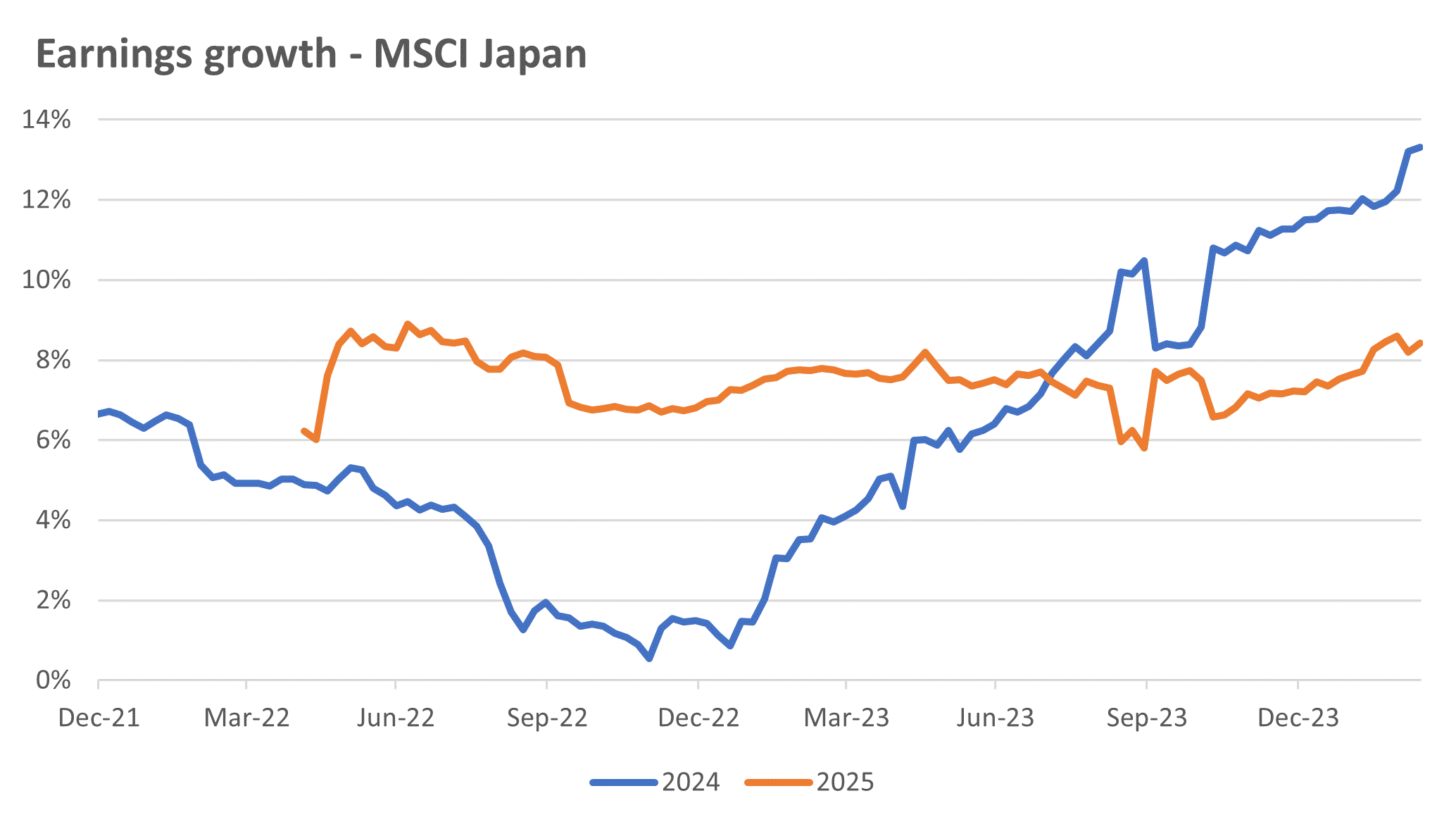

Let’s examine each factor, starting with the economy and how it’s flowing through to earnings growth. Japan has been growing above trend for the last year and is likely to continue growing above trend this year (it’s important to note, however, that Japan’s trend growth is lower than other developed markets). The recent Shunto wage negotiations saw an acceleration in wages growth for the year, which was the catalyst for the Bank of Japan raising the policy rate out of negative territory from -0.1% to 0-0.1%. The below chart shows analysts are looking for 8% earnings growth for the year ending March 2025 (see chart below), which we believe is achievable given the backdrop. The one risk to this is the potential for a stronger yen if the developed economy experiences a more meaningful slowdown.

Source: LSEG Datastream, 20 March 2024. Earnings growth are shown for financial year ending March

Factor #2: The NISA program encourages investing

The second factor, the NISA program, provides Japanese individuals with the ability to invest in stocks or mutual funds tax-free. This program, originally launched in 2014, was revamped in January. One of the key changes made was a doubling of the annual investment limit.

Factor #3: Corporate governance reforms

Lastly, let’s examine the impact of Japan’s corporate governance reforms. There is a long history of the Japanese market getting excited about potential improvements given the sluggish nature of corporate performance in Japan (for example, there has tended to be a high level of cross share-holding across major corporates). The Tokyo Stock Exchange has pushed forward this reform through publishing a list of companies that are deemed underperformers when it comes to corporate performance—they classify poor performers as those companies that are trading below book value.

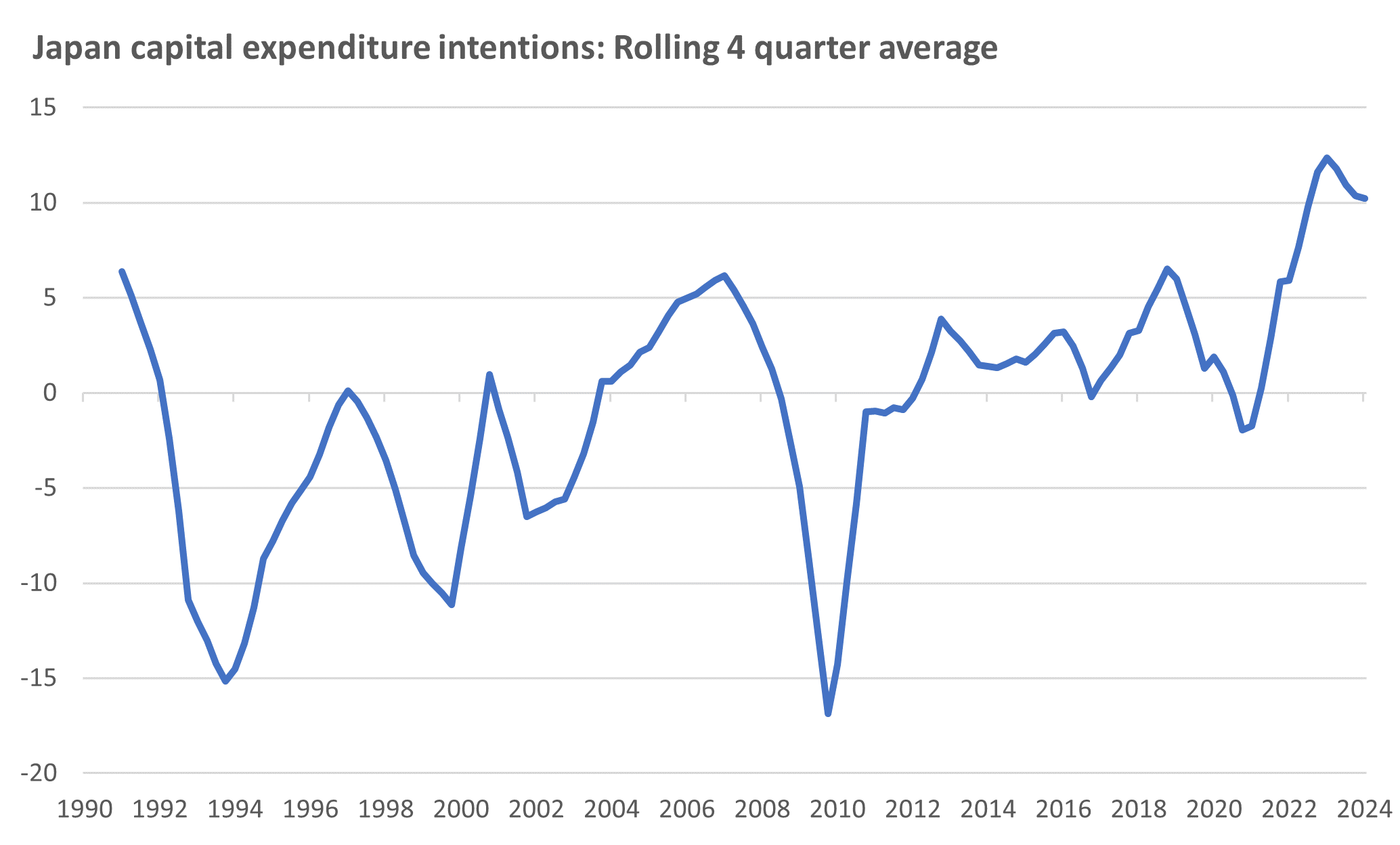

This focus on corporate governance, as well as the rebound in inflation, has seen Japanese corporates’ capital expenditure intentions increase, as the chart below shows. We expect that this trend will continue, especially given the longer-term dynamic of Japan’s worsening demographics (which increases the need for technological advances to sustain productivity).

(Click image to enlarge)

Source: Bank of Japan, LSEG Datastream, 3 April 2024

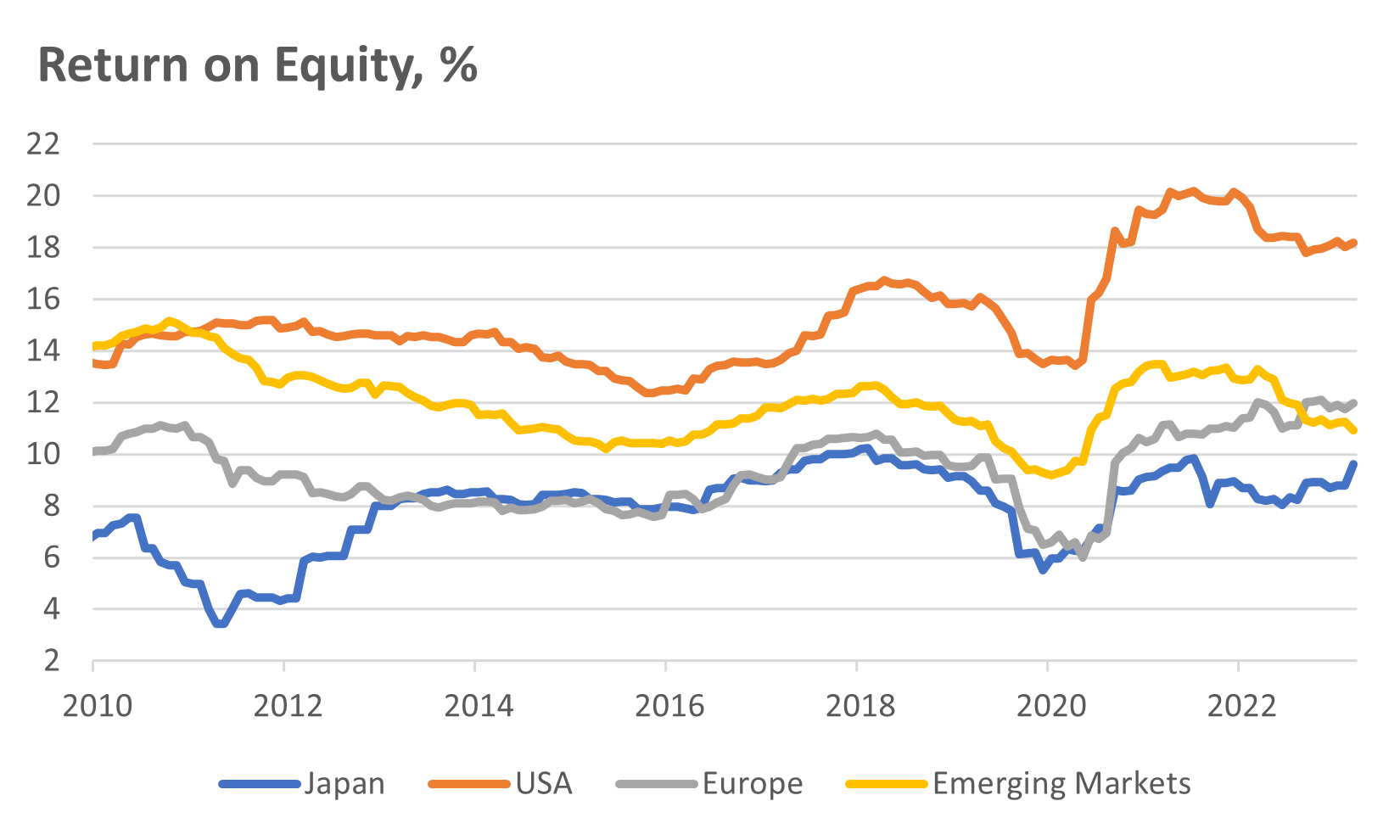

The chart below shows that we have seen early signs of an improvement in return on equity. Initially, we saw several companies announce stock buybacks in an attempt to push up the valuation on equities. That has since broadened out to more substantial measures looking at providing returns to shareholders, including increasing mergers and acquisitions activity.

(Click image to enlarge)

Source: LSEG Datastream, 29 February 2024

The outlook for Japanese equities in the months ahead

At Russell Investments, we evaluate markets through a lens of cycle, valuation and sentiment. While the cyclical backdrop in Japan looks decent, our various valuation models are suggesting that a lot of this good news is currently priced in. We estimate that the expected premium over bonds that Japanese equities can deliver has become quite tight. Another way to look at valuations is through a price-earnings growth model, which normalizes an earnings multiple for longer-term growth outlook. Here, we see that Japanese equities are priced in a similar vein to U.S. equities.

Finally, sentiment—the final pillar in our framework—is not showing dramatic signs that the market has become overbought despite the strong rally. This rhymes with what we are observing with U.S. markets, where sentiment is optimistic but has not reached euphoric levels.

The bottom line

Overall, we believe Japanese equities still have room to climb further due to a positive cyclical backdrop and improvements in corporate governance, although we note that a lot of the good news has already been priced in, given lofty valuations. In addition, a strengthening Japanese yen could prove to be a headwind to earnings and equities later in the year. While sentiment has not become euphoric, it will serve as a key watchpoint over the coming months.

2 Source: https://apnews.com/article/japan-nikkei-shares-record-economy-93003abeedbc99cf8f3dab78de78c298