Executive summary:

- Enrollment is projected to continue decreasing at many small universities, leading to a decline in funding. To offset this loss, many smaller colleges will likely need to seek higher returns from their endowments.

- We believe one way to achieve this is by increasing the allocation to private markets. We think endowments should consider increasing their exposure to private equity, private credit, private real estate, and hedge funds. Doing this allows for greater diversification, enabling smaller universities to enhance their returns in a meaningful way while being mindful of risk.

- By working with a skilled investment solutions provider, endowments can ensure that they maintain a tolerable level of risk and that these diversified private market strategies, which are often complex, are implemented efficiently.

With enrollment on the decline at many small universities, some are considering aiming for higher returns from their endowments as they prepare for the so-called enrollment cliff. The enrollment cliff is the expectation that due to demographic trends, the annual number of students that graduate from high school will decline by 13%1 by 2041.

Simply put, fewer high school graduates means fewer college enrollees. This is on top of a 15% decline in enrollment that already happened between 2010 and 2021.2 Falling enrollment means fewer tuition dollars to fund operating budgets. And that’s a problem, because universities with smaller endowments have historically funded a smaller proportion of their operating budget from their endowment than those with large endowments.3 The issue is clearly top-of-mind for many universities, as shown in the 2024 NACUBO-Commonfund Study of Endowments, where student enrollment was ranked as the number-one concern among a host of issues. This overall result was driven by smaller endowments ranking it as a top concern, while it seems like less of a concern for those with large endowments.

So, what can small colleges do? Along with looking to increase their spending rate to allow greater contributions to the operating budget, they might also decide to enhance scholarships and financial-aid packages to attract more students. The NACUBO survey indicates many are weighing this option, with the topic of increases in student aid ranking as the third-highest concern among universities (and second among private institutions). Doing this, however, would further drive up the required spending rate from the endowment. Because we do not expect endowments to give up on one of their key objectives— maintaining purchasing power in perpetuity—this would likely result in a need for overall higher returns. Is there a way to achieve this while maintaining a tolerable level of risk?

Private markets to the rescue?

Data from the NACUBO (National Association of College and University Business Officers) shows that the typical smaller endowment generates most of its returns from public equities, with a bias to U.S. equities. Portfolios with high allocations to public U.S. equities have done extremely well over the past few years. However, as they’re re-positioned for higher growth going forward, we think it would be a good idea to take advantage of the growth opportunities in private markets by increasing exposure to private investments.

What might such an allocation look like? We see private equity as playing a key role, but also believe that allocations to private credit, private real assets, and hedge funds make sense in order to achieve greater diversification. Diversifying the sources of return and gaining access to illiquidity premia can allow smaller universities to enhance their returns in a meaningful way, while being mindful of the risk they take.

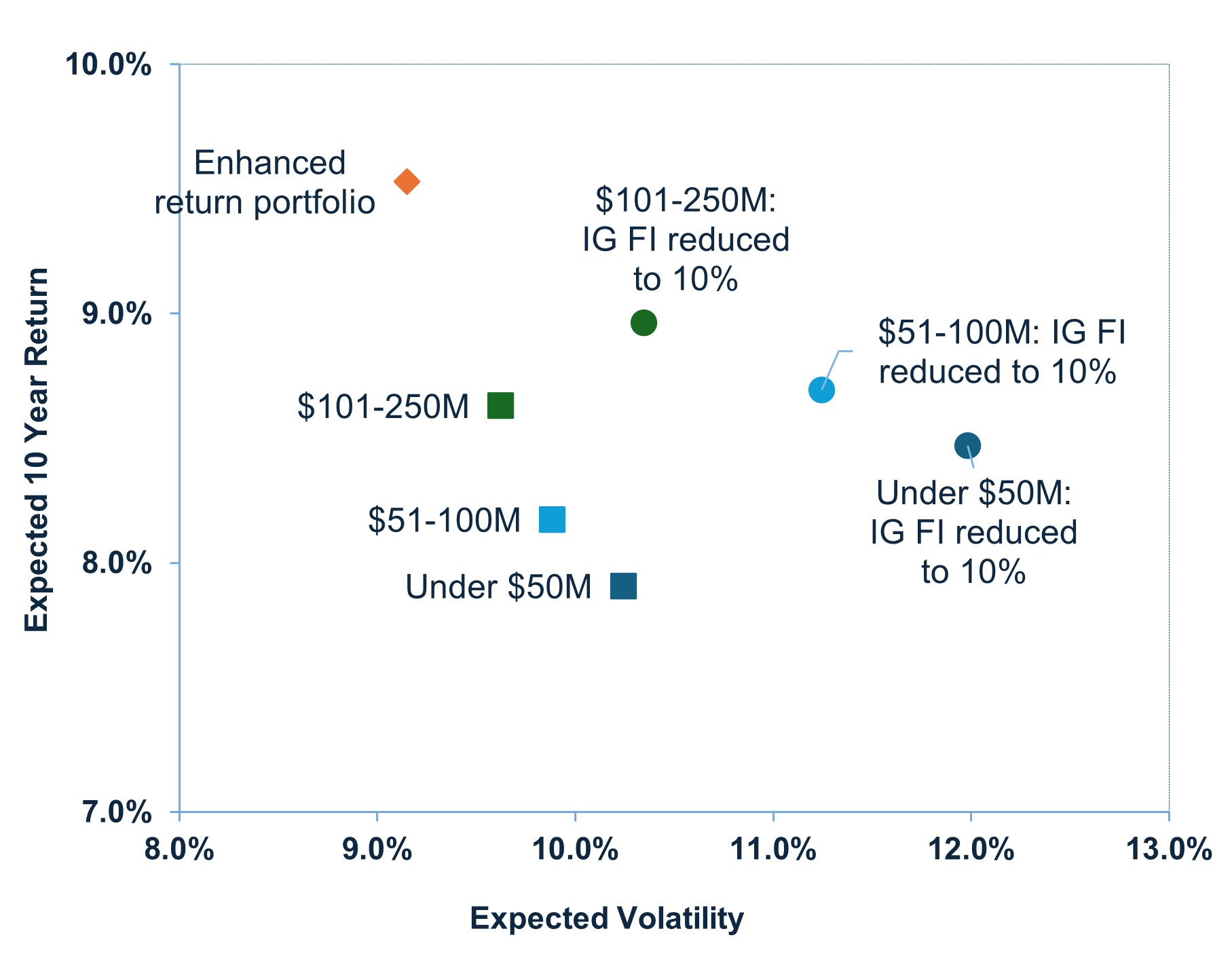

The below exhibit demonstrates this by showing:

- The expected return and volatility for the average allocations of the three smallest NACUBO endowment categories (green, light blue, and dark blue squares)

- What happens if these endowments try to increase returns—while maintaining their current composition of assets—by merely reducing their proportional allocation to investment grade fixed income and cash (green, light blue, and dark blue circles), and reallocating that to their existing growth assets (public and private equity, real assets, hedge funds, and private credit)

- A sample portfolio with a higher allocation to growth assets vs. the three NACUBO universe subsets is represented by the orange diamond. This “enhanced” return portfolio is comprised of 47% public equities, 20% private equity, 1% public real assets, 4% private real assets, 8% private credit, 10% hedge funds, and 10% investment grade fixed income

Exhibit #1

The analysis demonstrates that without reconsidering the composition of the portfolio, any increase in expected returns will likely be accompanied by an increase in volatility, which may not be tolerable as the need to rely on the endowment for annual spending increases.

The value of working with a skilled investment solutions partner

As smaller endowments target higher returns, we believe that rethinking the asset allocation and including higher allocations to private investments and hedge funds will be essential to ensuring that the portfolio risk remains tolerable. From our vantage point, working with a skilled investment solutions partner that has the right systems to measure the risk and illiquidity of the potential changes is crucial. Importantly, the answer won’t be exactly the same for every endowment.

It's also important to understand that for these universities, updating their portfolio’s asset allocation to target improved returns and diversification is only one step. This is because as a portfolio expands more broadly beyond traditional asset classes, ensuring robust implementation becomes increasingly important. Why? Because there is a wider distribution of returns across managers in alternative investments than in traditional asset classes.

It's also important to note that larger endowments have relatively consistently outperformed smaller endowments within private equity.4 This shows that it typically isn’t enough for smaller universities to just increase their allocation to private investments in order to boost returns. These organizations also need to work with partners that can identify and access top-quartile managers.

Private investments also create additional cashflow needs in managing capital calls and distributions. Endowments that don’t have large internal teams will need to ensure that they have partners to efficiently manage those capital calls and distributions on their behalf. From our vantage point, managing this internally without sufficient resources typically leads to a bias to hold excess cash to reduce cashflow risk. This, in turn, can create a drag on total portfolio returns and undo the other changes that have been made to bolster returns.

The bottom line

Universities preparing for declining enrollment face many challenges ahead. Enhancing portfolio returns to allow for greater spending from the endowment is one important piece to solving the funding puzzle.

For endowments that have historically held more traditional portfolios, we think it’s essential to work with a partner that has deep knowledge of the impacts on risk and illiquidity of different asset allocation changes. In addition, we believe it’s table-stakes to work with a partner that not only has access to high-quality managers but is also able to efficiently implement these more diversified and complex strategies.

1 Based on a report from the Western Interstate Commission for Higher Education.

2 Based on data from the National Center for Education Statistics.

3 Based on the 2023 Nacubo Commonfund Study of Endowments.

4 Based on the annual NACUBO surveys from 2012-2023 there was only one year in which any of the three smallest endowment categories outperformed either of the two largest endowment categories for annual returns within private equity.