Executive summary:

- U.S. import tariff policy remains highly fluid, with announcements of new levies against imports from Canada, Mexico, and China swiftly followed by delays in implementation. The U.S. is also expected to announce new tariffs on steel and aluminum soon.

- Active equity managers are broadly taking a wait-and-see approach given the uncertainty around tariffs, and are not materially shifting portfolio positioning until more concrete details around policy emerge.

- Managers are cognizant of potential risks to portfolios, identifying dominant Chinese component manufacturers, North American automotive supply chains, and smaller cap industrial cyclicals as market segments worth monitoring.

Background

As detailed recently by our Senior Investment Strategist, BeiChen Lin, over the first weekend in February, U.S. President Donald Trump announced the imposition of an additional 25% tariff on Canadian and Mexican imports into the US and a further 10% tariff on Chinese imports. On the following Monday, it was announced in separate statements that the implementation of tariffs against both Canadian and Mexican imports would be delayed for a period of 30 days, while tariffs on Chinese imports would be maintained. In apparent retaliation, China announced its own set of targeted tariffs against U.S. imports and select technology companies. In the latest development, the U.S. is also expected to announce 25% tariffs on steel and aluminum imports.

Why does this matter? Since the North American Free Trade Agreement (NAFTA) went into effect in 1994, the economies of the U.S., Canada, and Mexico have become ever more intertwined. Today, production facilities and supply chains are sprawled across borders and are reliant on the lack of tariffs and taxes between the countries to enable a highly optimized production and logistics effort. China joining the World Trade Organization (WTO) in 2001 wrought a similar, larger effect globally, with multinationals investing heavily in the country in subsequent years and now boasting supply chains highly dependent on continued unfettered access to Chinese production and assembly.

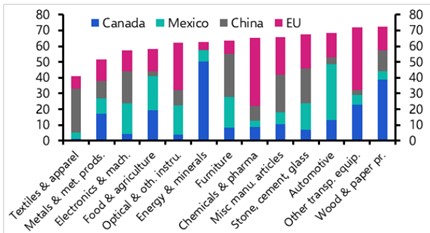

Source: Capital Economics

The chart above shows the share of U.S. imports across a range of industries broken down by origin. It can be readily observed that Canada, Mexico, China, and the EU (which has also been threatened with import tariffs) make up a significant—often a majority—share of U.S. imports across a wide portion of the economy. The introduction of tariffs, which are taxes, will increase costs across supply chains, leading to higher prices paid at each border-crossing step of the production and distribution processes.

In the short-run, companies that are ill-prepared for increased tariffs could see significant input cost increases, potentially leading to shortages of finished goods, which will further exacerbate price rises to end consumers. In the longer-term, if higher tariff rates persist, companies could face stark investment choices regarding reorienting production toward higher-cost geographies, which would likely contribute to a locking-in of the higher level of consumer prices.

Implications for manager positioning

At a high level, active equity managers are trying not to overreact one way or another to what has been characterized by one manager as a headline soup of competing and at times contradictory headlines, policies, and announcements. In our recent calls with managers, multiple portfolio managers were quick to note the measured, more industry-specific approach to tariffs sought by Treasury Secretary Scott Bessent, while also acknowledging the possibility of an across-the-board country-based approach sought by other personalities within (and outside) the administration.

As noted by our strategists, the tariff situation is expected to remain fluid over the coming weeks, months, and potentially years. Managers for the most part are avoiding large shifts in their portfolio positioning until more concrete details around tariff policy and its likely duration take shape. That said, managers are highly cognizant of the potential risks associated with increased tariffs being levied against the major trading partners of the U.S. and have worked to inoculate portfolios against possible downside risks. While not an exhaustive list by any means, we detail a few of the risks identified by managers below and note how they have adjusted portfolios accordingly.

- Large cap growth managers pointed to (at least) two major risks associated with China: 1) the country’s dominance of the global battery supply chain; and 2) a high degree of contract manufacturing for re-export, particularly within consumer electronics. EV-dependent automakers like Tesla could be at risk if battery components are subject to retaliatory tariffs. Likewise, large consumer electronics companies like Apple, whose iPhones are largely assembled in China, could see a hit to both demand and profitability. Consequently, managers have sought to trim holdings with large Chinese exposure.

- Large cap value managers spoke to risks within the highly connected North American automotive supply chain, where components are regularly manufactured in Canada, shipped to Mexico for final assembly, and then sold onto end consumers within the U.S. Tariffs on Canadian and Mexican imports would stymie the free flow of components and lead to both higher end prices and reduced profitability for automakers. Companies reliant on facilitating trade, like railroads and truckers, would also be harmed by any slowdown in trade. As a result, managers reduced their exposure to the space during the fourth quarter.

- Small cap managers, while acknowledging the potentially more insulated nature of domestic production and demand across certain verticals, nonetheless expressed caution given the high degree of uncertainty around the timing, magnitude, and duration of any tariffs. While higher-cost domestic production could stand to benefit from the imposition of tariffs in certain industries, the uncertainty around their duration and ultimate purpose gives many companies pause. Smaller cap companies in general are reluctant to build out new capacity if a reversal in tariff policy could render that incremental capital investment unprofitable and potentially lead to a stranded asset base. Smaller cap managers have tended to add to cyclicals primarily expected to benefit from reduced regulation, such as financials, rather than more industrial cyclicals.

The bottom line

The recent tariff policy of the U.S. remains highly fluid. Active equity managers, while conscious of the associated risks, are reluctant to materially shift portfolio positioning given the potential for dramatic policy shifts or even short-term reversals. At Russell Investments, we continue to think investors would benefit from staying disciplined and taking a long-term view. Over time, we believe skilled active managers can consistently add value above their benchmarks, particularly during times of elevated uncertainty where the dispersion of potential outcomes is wide.