Key takeaways:

- The U.S. dollar’s dominance is slipping amid a highly concentrated stock market and shifting global alliances.

- While no single currency is poised to replace the dollar, we believe investors should consider diversifying their currency exposure.

- We think the Japanese yen offers potential safe-haven benefits.

For decades, the U.S. dollar’s dominance has rested on two pillars: America’s deep capital markets and its global security alliances. Today, both are under strain. Shifting U.S. foreign policy, rising geopolitical uncertainty, and an overextended stock market are making investors and policymakers reconsider their exposure to the greenback.

Fundamental forces have driven a stronger U.S. dollar (USD) in the last five years. After the Covid pandemic, the U.S. Federal Reserve (Fed) started raising interest rates earlier and more aggressively than most other major central banks, leading to an interest rate advantage for the USD. Energy prices spiked when Russia invaded Ukraine in 2022, putting energy importers in Europe and Asia at a disadvantage to the U.S. due to America’s energy independence. Lastly, the global dominance of the U.S. technology sector and outperformance of its stock market over other regions gave rise to the notion of “U.S. exceptionalism”.

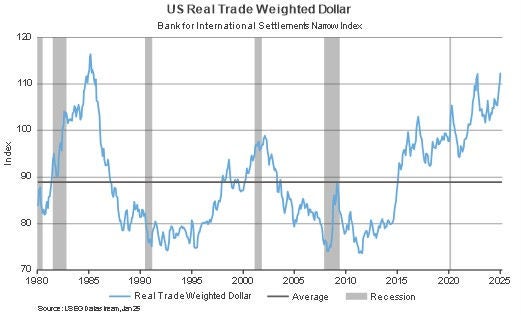

These forces have propelled the U.S. dollar’s valuation to a historically high level. Among the 10 most traded developed-market currencies, the USD is the second-richest relative to its purchasing power parity level1, only behind the Swiss franc. Another valuation metric, the real trade-weighted dollar index published by the Bank for International Settlements, suggests that the dollar is expensive compared to its long-run average (see chart). It was significantly higher only once in the last 55 years—in 1985, when the “Plaza agreement” between the U.S. and four major trading partners to deliberately push the value of the dollar down led to a multi-year dollar bear market.

USD valuation is stretched

Shifting alliances

The United States has long been the guarantor of global stability, a role that reinforced the dollar’s status as the world’s reserve currency. Berkeley economist Barry Eichengreen and his co-authors2 argue that security alliances play as important a role as economic fundamentals in the choice of reserve currencies. Countries that are reliant on the United States for military support hold more USD than is justified on purely economic grounds. Yet as Washington’s commitments appear more conditional—see the recent frictions between the U.S. and Ukraine over military support—its allies are reassessing their strategic and financial dependencies.

Last week, Germany’s incoming government decided to exempt defense spending from its deficit limits, paving the way for much increased military spending. Europe’s renewed focus on defense autonomy and China’s continued push for alternative payment systems underline a broader trend that has so far been developing gradually: diversification away from the dollar.

Where to hide?

Beyond geopolitics, another risk looms: the high concentration of U.S. stock markets. The S&P 500’s dependence on a handful of technology giants has created an increasingly top-heavy market, with the Magnificent Seven3 companies at times accounting for more than one-third of the market capitalization of the index. Concerns around high market concentration in U.S. equity markets could induce capital outflows. With roughly 60% of global reserves still held in dollars, even a modest reallocation would have significant consequences for exchange rates. However, no single currency or asset is poised to replace the dollar, but a more fragmented order is emerging.

Gold is one alternative reserve asset. Central bank purchases of gold have increased in recent years, signalling demand for hedges against monetary uncertainty. The World Gold Council estimates that central banks added around 1,000 tons of gold reserves in 2024. This is well reflected in high gold prices of $2,920 per ounce as of March 7, a rise of nearly 80% since November 2022.

We believe that the Japanese yen is a more attractive safe-haven asset than gold today, given its defensive characteristics. If global markets hit a rough patch, the yen’s undervaluation makes it one of the most attractive risk-off bets for investors seeking refuge. Over the period in which gold rose by 80%, the yen has fallen by around 5% against the U.S. dollar. In 2025, it has started to reverse that trend and is nearly 7% stronger year-to-date. We believe the yen can rise further, especially if market turbulence continues.

The new order

In hindsight, international diversification was not beneficial to U.S. investors in the last five years as U.S. stocks outperformed and the USD strengthened. The dollar’s supremacy has withstood repeated challenges, and it would be premature to predict its demise. Yet its era of unquestioned dominance is fading. We believe investors should adjust accordingly, accounting for currency diversification, geopolitical shifts, and a world in which international capital increasingly seeks alternatives.

Amid these shifts, investors should reconsider how they manage foreign exchange (FX) exposure. Currency strategies using a rules-based approach, focusing on Carry, Value, and Trend factors, offer return potential and diversification benefits. Thoughtful FX management is no longer optional. It’s essential in a multipolar financial system.

Adaptation, not complacency, will define the next era of global capital markets.

1 Purchasing power parity measures at which exchange rate the cost of living would be equalized in two different countries. It is a commonly used metric for the “fair value” of a currency.

2 See https://cepr.org/voxeu/columns/mars-or-mercury-geopolitics-international-currency-choice

3 The “Magnificent Seven” are Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia, and Tesla.