Key takeaways

- UK gilt yields have risen sharply as investors demand a growing UK-specific risk premium.

- Political uncertainty and questions around long-term fiscal discipline are adding to market concern.

- Higher yields are tightening financial conditions but could improve long-term return potential for bond investors.

Rising gilt yields

For many investors, the recent volatility in UK gilt markets may feel sudden. UK borrowing costs are now sitting at levels not seen for decades, with 30-year gilt yields approaching levels last seen in the late 1990s, and 10-year yields moving above 5%.

Yet, despite the recent volatility spike, the move in gilts has been building for months, a trend with increasingly important implications for investors.

Looking beyond market volatility

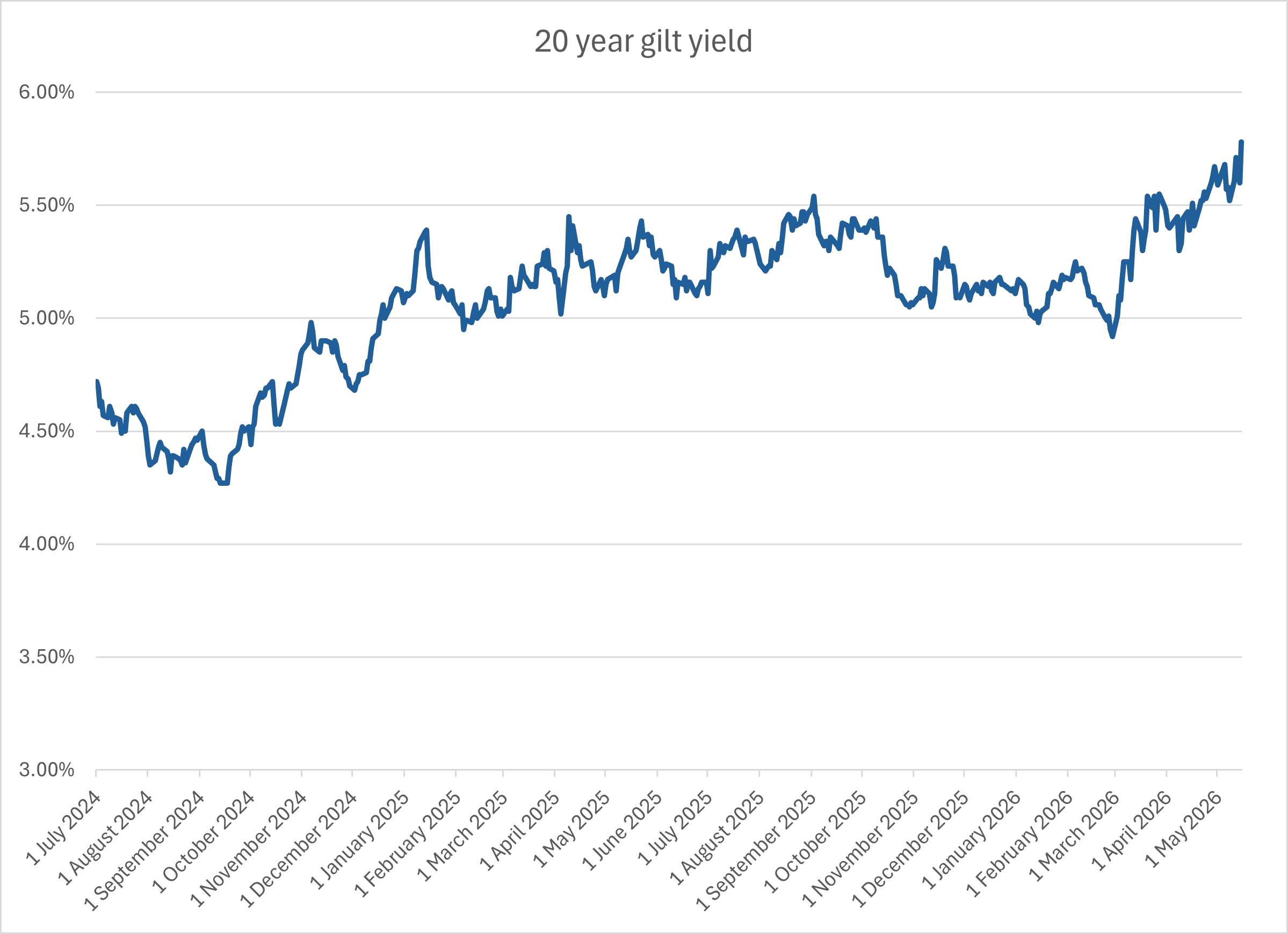

Pressure on gilts has been a long-term issue. Since mid-2024, long-term gilt yields have risen materially, with parts of the curve moving more than 1% higher (see blow chart for 20 year gilt yields). The October Budget reinforced concerns around structurally higher borrowing requirements and the long-term trajectory of public spending.

Source: Investing.com

Britain does not have the highest debt-to-GDP ratio among major economies, yet UK 10-year government bond yields have traded at the highest levels in the G7 since Labour’s first Budget. That suggests markets are increasingly demanding a UK-specific risk premium driven not only by debt levels, but also concerns around growth, fiscal credibility and long-term economic direction.

Market concern has also been exacerbated by the structural fiscal challenges the UK faces. This includes having a high share of inflation-linked debt, post-EU economic constraints, and relatively elevated foreign ownership of government debt.

Why political uncertainty matters

Although yields have risen by only around 20–30bps in recent weeks, the bigger issue for markets has been the speed of the moves and the level of political uncertainty. While part of the recent sell-off reflects global developments, particularly escalating tensions involving Iran, UK-specific political uncertainty has increasingly become a differentiating factor. This is reflected in the fact that 10-year UK gilt yields have risen more than those of any other G7 economy year to date, underlining the extent to which markets are pricing a growing UK specific risk premium.

Markets are already beginning to differentiate between possible political candidates which is likely to add further volatility as the political landscape unfolds. Figures such as Wes Streeting are generally perceived as more centrist and fiscally pragmatic, whereas Andy Burnham and Angela Rayner are viewed as representing a more expansionary and interventionist policy stance and potentially a looser fiscal approach.

Why this matters for the wider economy

Higher gilt yields increasingly feed through into the wider economy via higher mortgage rates, more expensive corporate borrowing and tighter financial conditions overall. The UK remains particularly sensitive to rising yields given its elevated debt burden, significant refinancing requirements and relatively short debt maturity profile compared with some international peers.

Mortgage pricing has already started to reprice higher as swap rates respond to gilt volatility. This risks further weakening growth at a time when the UK economy is already struggling with weak productivity, subdued investment and fragile consumer confidence.

What this means for investors

Despite the challenging backdrop, long-term gilts could become attractive from a valuation perspective and play an important role within multi-asset portfolios as both a diversifier and potential return driver.

While political uncertainty may place further upward pressure on yields in the near term, 20- and 30-year gilt yields are now trading at levels not seen for decades. Current yield levels imply significantly stronger long-term return potential than the ultra-low yield environment of the last decade.

For pension investors:

- Defined Contribution investors approaching annuity purchase may wish to consider hedging interest rate and annuity pricing risks.

- Defined Benefit schemes progressing towards buy out may consider increasing hedging levels while funding positions remain attractive.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.