Executive summary:

- Bond ladders were a staple of many investor portfolios until rates fell to historic lows after the 2008 Great Recession

- As rates rose in the past two years, the appeal of these laddered strategies grew

- There are a variety of ways to build a fixed-income ladder to meet a variety of investor needs

For decades, a key component of many investors’ portfolios was a fixed income ladder. It was intended to provide ballast to the more volatile equity allocation and help reduce interest-rate risk.

But things began to change in 2008 when the Great Recession forced the U.S. Federal Reserve to cut interest rates to historically low levels to stimulate the economy. Fixed income instruments that offered yield, like bonds, became less attractive. And bond ladders, which include bonds of various maturities, fell out of favor.

Things have begun to change again. Now that interest rates have returned to levels where investors can earn a reasonable yield on bonds, fixed income ladders are starting to make sense as part of a diversified portfolio.

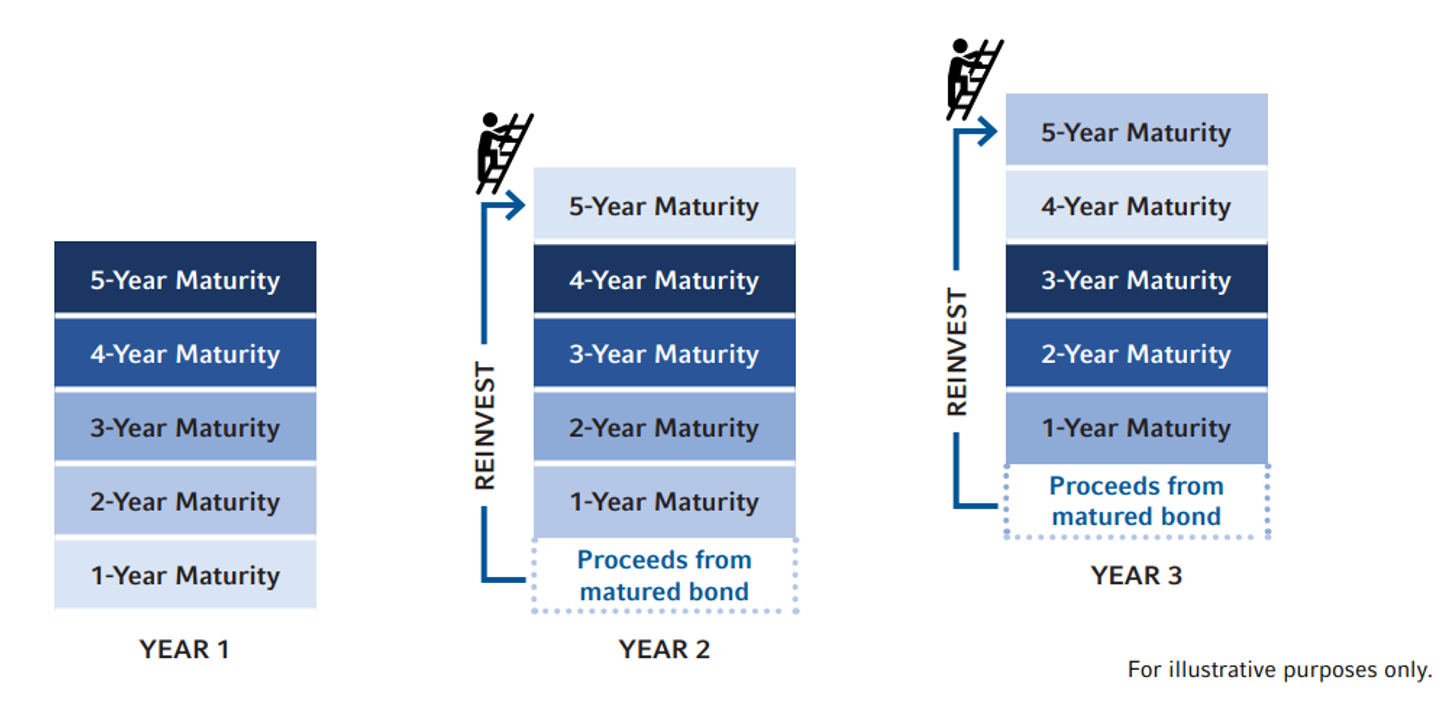

What is a fixed income ladder?

A fixed income ladder is an investment strategy with a series of fixed income securities of staggered maturities. The idea is that when the lowest rung of the ladder - the fixed-income security with the shortest term – matures, it is liquidated and replaced by a longer-term maturity. In this way the investor receives a regular income stream while hedging against any changes in interest rates as they climb the ladder.

How are bond ladders different than mutual funds and ETFs?

There are a few key differences between a bond ladder and a packaged investment like a mutual fund or Exchange Traded Fund (ETF). A bond ladder allows an investor to own the individual bonds themselves, and if they hold them to maturity, they will receive back their initial investment plus earn a predictable interest rate along the way.

Fixed income mutual funds and ETFs do not have set interest rates. Therefore, the yield and the value of the investment will fluctuate with the market. For example, if rates rise, the yield on the bond fund or ETF may increase, but the overall value of the investment may fall. Of course, the opposite thing happens if rates fall. This is a result of bond prices moving in an inverse direction to the yield.

With a bond ladder, if held to maturity, the value of the portfolio will remain the same, and the interest rate is locked in for each bond held.

What kind of bond ladders are there?

Just like you can have a wood ladder or a steel ladder, investors can build their ladders with different materials. A bond ladder can be built with Certificates of Deposit, with government bonds, corporate bonds or municipal bonds. Each has its advantages and disadvantages. For example, municipal bonds can offer tax advantages, investment-grade corporate bonds can offer potentially higher yields, while government bonds, or U.S. Treasury bonds, are backed by the guarantee of the U.S. government.

Are bond ladders suitable for everyone?

Bond ladders, mutual funds and ETFs all offer investors access to the fixed income market. Mutual funds and ETFs offer investors an opportunity to increase the value of their investment over time (if rates fall) or earn a higher yield if rates rise. Conversely, the yield on a mutual fund or ETF will fall if rates fall, and the portfolio’s value may go down if rates rise. Bond ladders hold the same value over time (If held to maturity) and the interest rate (or yield) is fixed.

A bond ladder is suitable for a portfolio if the primary focus is preservation of principal and a consistent yield. Mutual funds and ETFs also have lower investment minimums than bond ladders.

How do bond ladders fit into a portfolio?

As noted, bonds provide stability in a diversified portfolio. Bond prices rarely fluctuate in value to the same extent as equities so holding them can help smooth out returns.

Bond ladders not only provide that stability, but due to the staggered maturities, they can be a source of yield, making them a good choice for investors who need a steady stream of income.

Why incorporate a SMA for your bond ladder strategy?

Because the investor holds the bonds directly, rather than in a bond fund or ETF, they are potentially best suited in a Separately Managed Account (SMA).

SMAs allow investors to customize their portfolios to align with their individual risk profiles and goals. An investor can choose a specific type of bond ladder to fit their needs – perhaps one built with municipal bonds if they are looking for tax minimization, or one using Treasuries if they require stability. They can also choose the maturities of the bonds so that the ladder provides income for the length of time required. And because the bonds have a set interest rate, the ladder can protect the investor against the risk of rates falling from existing levels.

In conclusion, the more attractive yields offered over the past few years have prompted many investors to consider incorporating fixed income ladders into their overall investment portfolios. Maybe now is the time to have a fresh conversation with your clients about incorporating a bond ladder SMA into their fixed income strategy.