5 / 16

5 / 16

p / 5

RUSSELL INVESTMENTS

Unlike glide paths that are customized to a

population of employees, ARA provides a

solution customized to the profile of each

participant. Further, the system monitors

– via record keeper and plan sponsor

data feeds – the evolving characteristics

of each participant and responds with

customized asset allocation model advice

through time.

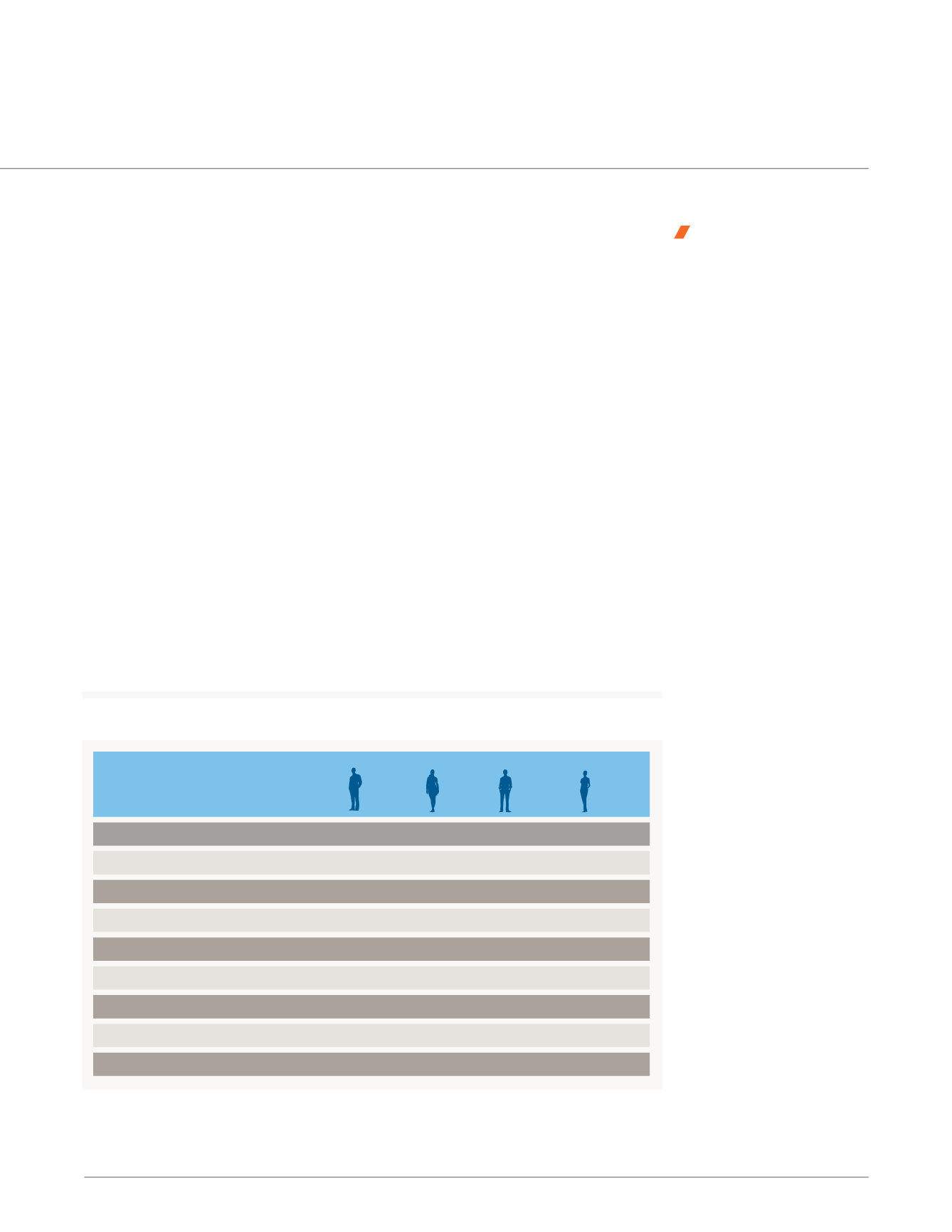

Let’s meet four pre-retirees all of

whom are 50 years old and 15 years

from retirement.

With TDFs, they all would receive the

same allocation – now and all the way

to retirement at age 65. Consider the

hypothetical information summarized

in Table 1, which is readily available from

the plan sponsor and plan record keeper

and could inform a better strategy for

each person.

This example does not take into account

all of the characteristics that could be

considered, such as assets held outside

of the retirement plan. The financial

health of each participant is a combination

of account balance and future 401(k)

contributions compared with the

retirement income to which each aspires.

3

It is clear that participants with large

retirement resources relative to their

retirement spending goals (whether due

to an early start on retirement savings or

being fortunate enough to be in the right

investment at the right time) are

in a better position.

Jack /

Has the highest salary and

presumably the highest retirement

income target. Social Security will be a

smaller portion of his retirement solution

suggesting that a higher replacement

rate must be supported by his retirement

account. Further, Jack’s deferral rate is

lower than either of the other three.

3

Using appropriate discount

assumptions, this relationship can

be summarized as a funded ratio.

Jack has the

highest salary and

presumably the

highest retirement

income target.

JACK TAMARA BILL

CRYSTAL

Age

50

50

50

50

Gender

Male

Female

Male

Female

Salary

$150k

$120k

$85k

$100k

Deferral rate

4% 8% 8% 12%

Current account balance

$425k

$475k

$475k

$686k

Target retirement income (annual)

$120k

$96k

$68k

$80k

Expected retirement income (annual)

$75k

$90k

$74k

$102k

ARA growth asset allocation

78% 69% 64% 83%

Target date growth asset allocation

68% 68% 68% 68%

Table 1: Asset allocation based on individual characteristics

Sample allocations are provided for illustrative purposes only and are based on assumptions provided.