Listings of SpaceX, Anthropic, and OpenAI could mark a new phase in the relationship between private and public markets. These IPOs may improve liquidity and market access but could also increase market concentration and create benchmark-driven volatility as passive investors absorb newly listed shares.

Over the past six months, investors have seen markets repeatedly pressure tested by geopolitical tensions, policy uncertainty, and shifting economic expectations. Yet the underlying foundations of the global economy have remained intact. While the conflict with Iran tested markets, the S&P 500 recovered its initial decline in less than three months and went on to reach new highs.

Record corporate earnings, improving manufacturing activity, a labor market that remains healthy, and early signs of AI-driven productivity support our constructive view on growth, even as we remain attentive to evolving risks.

In our Mid-Year Outlook, we examine these forces driving market resilience and the key watchpoints we believe will shape markets through the remainder of 2026.

Mid-year report

Supercharged global earnings

Despite geopolitical pressure, the current supercycle for corporate profits is pushing global equities to new all-time highs. Over the past three years, S&P 500 forward earnings compounded roughly 16% annually—a pace exceeded only by post-recession rebounds in recent decades.

Yet, while earnings have remained strong, leadership has narrowed again after the onset of the Iran conflict. Price and fundamental momentum rotated back to the artificial intelligence (AI) theme—most notably among the tech heavyweights in South Korea and Taiwan. Strong corporate earnings have also helped set the stage for mega-cap IPOs and increased private market activity over the next six months.

From accelerating growth, back to resilience

The strong global market has largely been underpinned by U.S. growth. In our annual outlook we saw potential for the U.S. economy to inflect from resilience to acceleration, with tailwinds from fiscal stimulus, the AI buildout, and loose financial conditions. Six months later, higher gasoline prices are likely to rein in some of this upside potential.

Despite the pressure, we see a strong U.S. economy and encouraging progress in two areas:

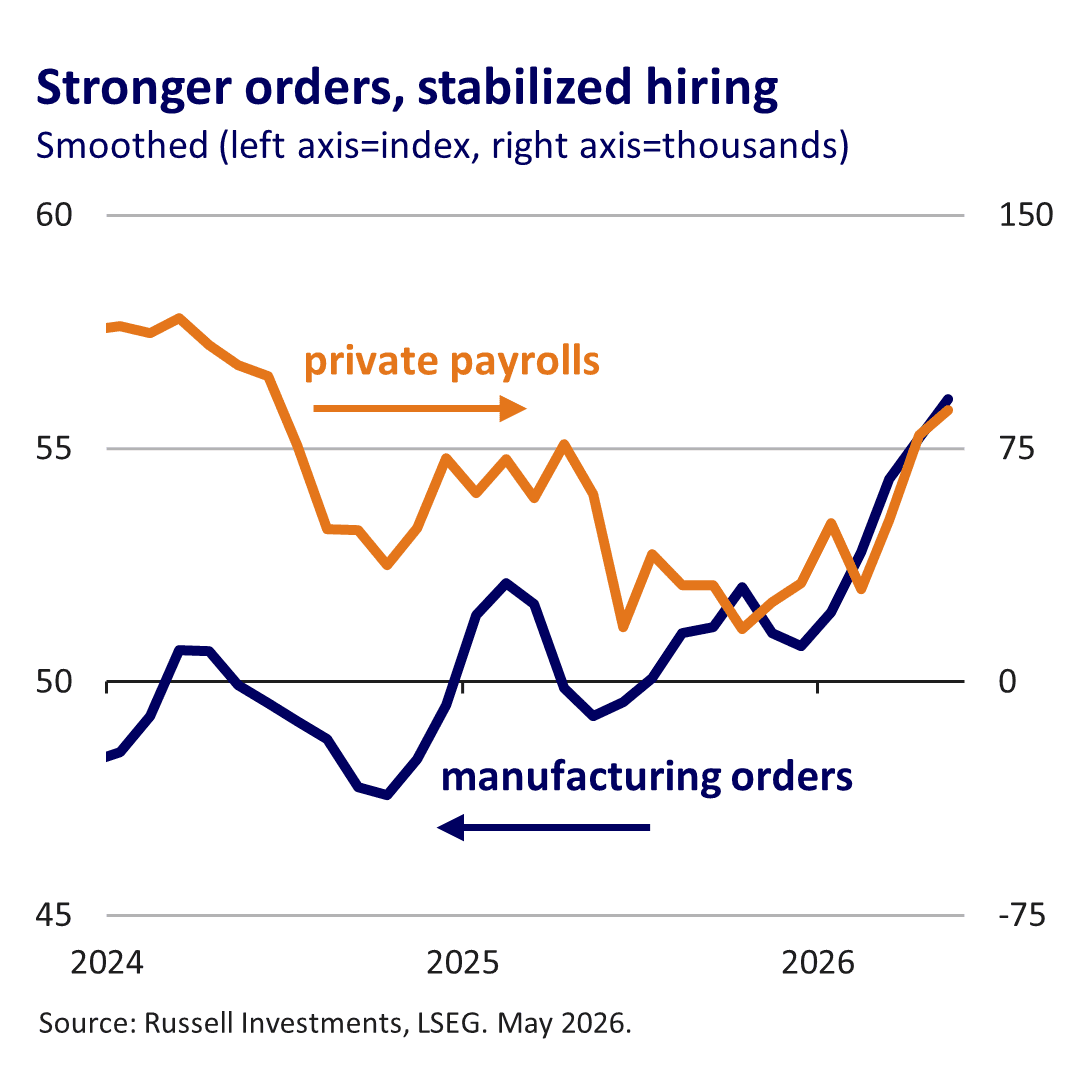

- Manufacturing activity is improving. After years of stagnation, we expect the sector to recover on favorable capex provisions from the One Big Beautiful Bill Act and robust data center demand. Industrial production and the order books for manufacturers are on an uptrend.

- Labor market conditions have stabilized. Private sector hiring slowed sharply in 2025, but our analysis suggested that more than 80% of the slowdown reflected public policy uncertainty rather than private sector distress. For the first half of this year, layoffs remained low and payrolls stabilized at healthier levels in recent months. Job growth also improved. Despite growing concerns about AI's impact on employment, we continue to see stronger evidence of productivity gains rather than broad-based labor market disruption. So far, the effects appear concentrated in early-career hiring rather than widespread job displacement.

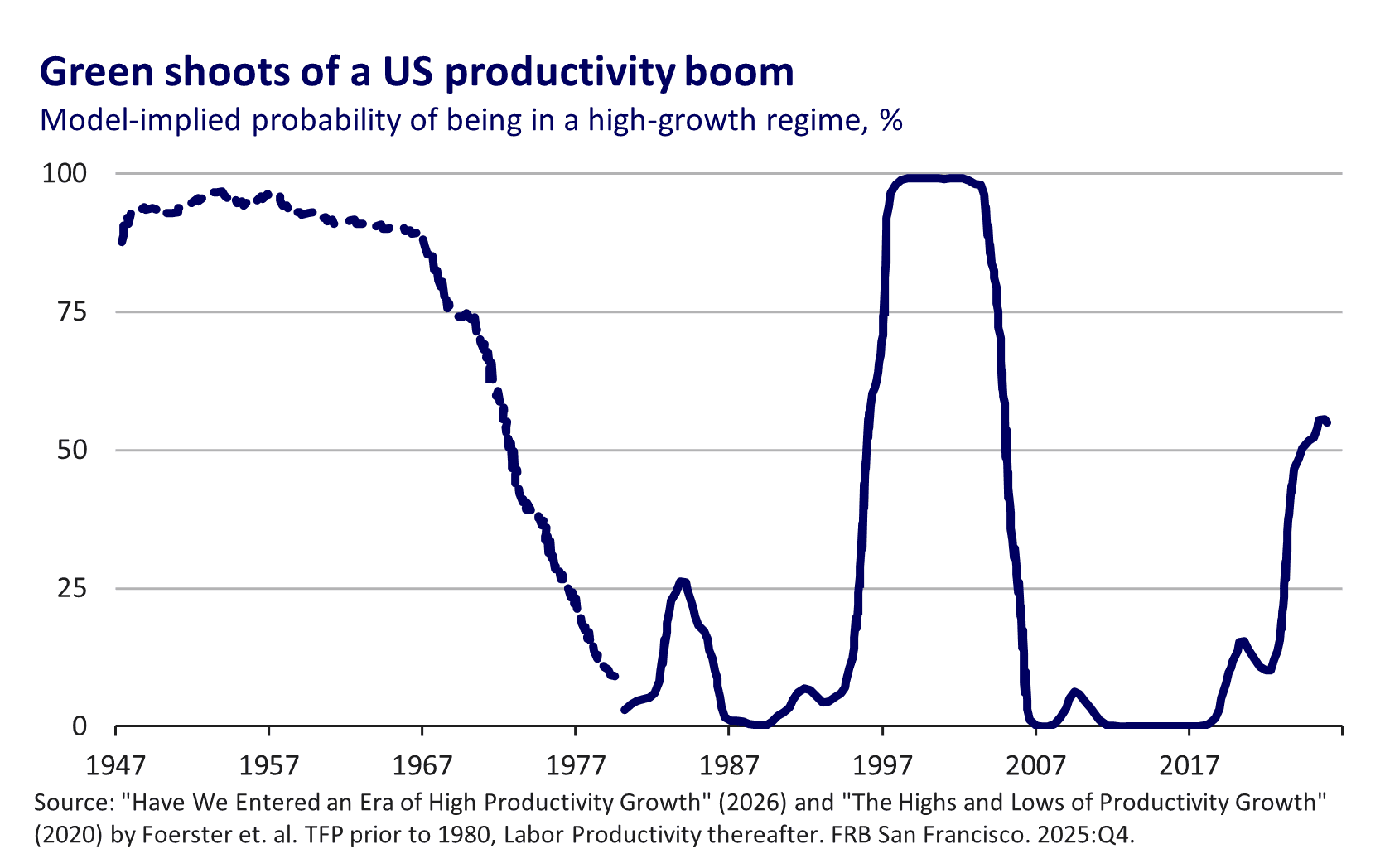

AI shows productivity benefits

Another core pillar of our constructive annual outlook for 2026 was the potential for generative AI to move up the productivity J-curve, bringing more tangible benefits for corporates. While this is likely to be a multi-year theme, six months into 2026 we continue to see encouraging signs of its impact on productivity. Frontier models are increasingly capable, end-user demand for generative AI is strong, and there are green shoots of a new productivity cycle in the macro and microeconomic data.

Economic pressure watchpoints

Halfway through 2026 and the economy remains on solid footing, though several key watchpoints lie ahead.

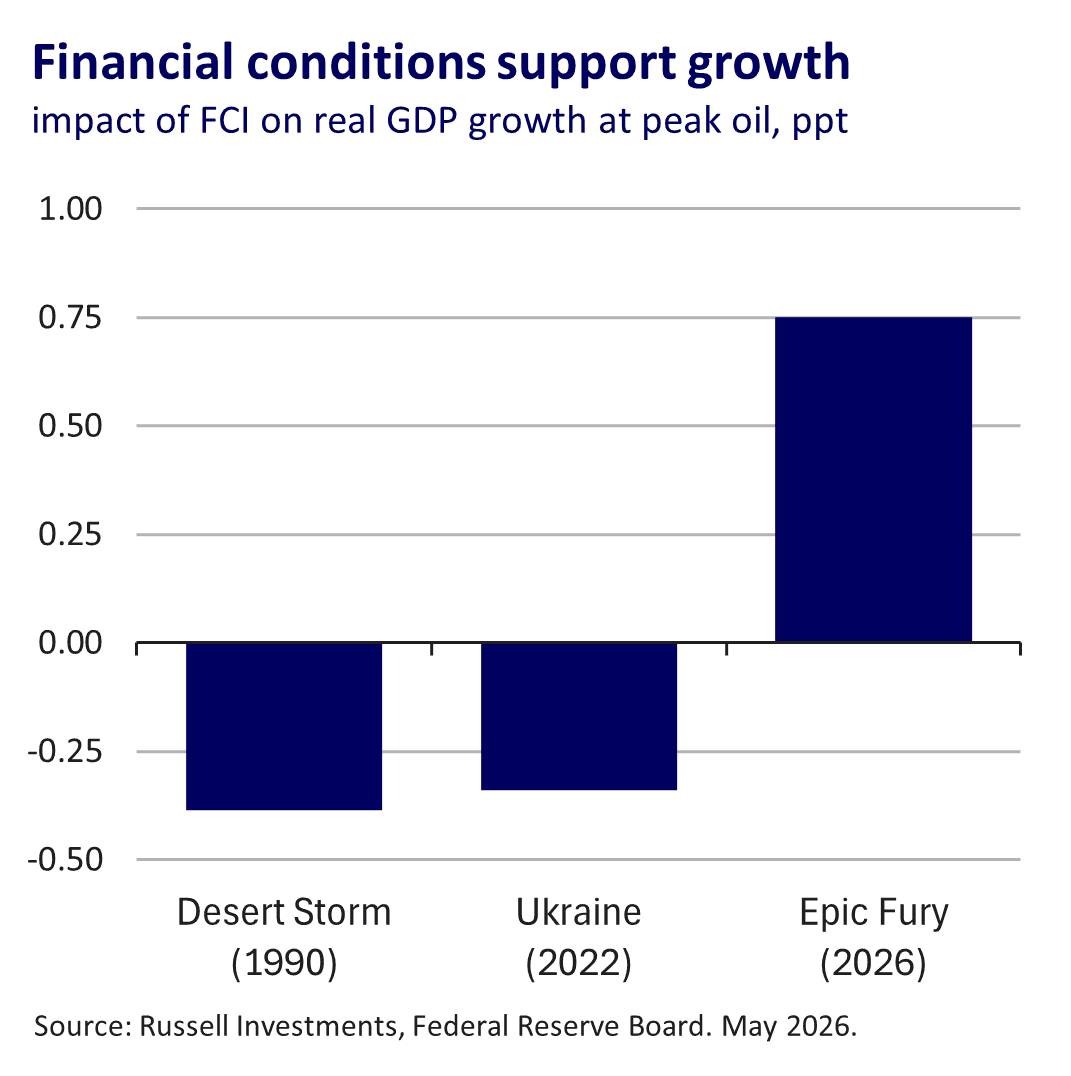

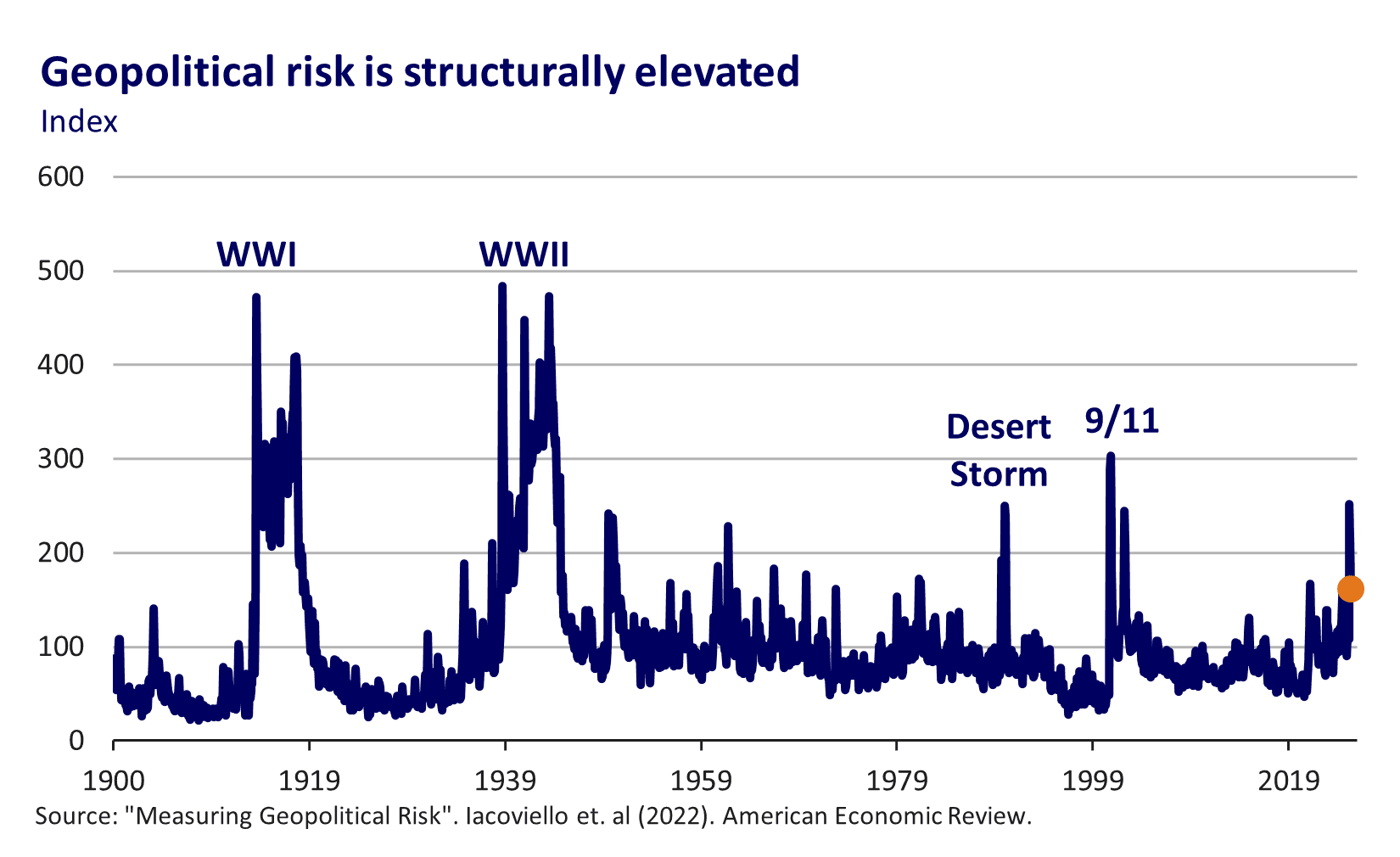

Watchpoint 1: Cyclical and structural implications of the Iran conflict

While a diplomatic resolution could lower recession risk, the timing of full resumption of commodity flows and whether or not conflict re-emerges could determine how markets and the economy evolve through year-end. When evaluating the risk posed, the distinction between market reactions and fundamental economic impacts remains important. The impact arising from the conflict is likely to filter through commodities, supply chains and inflation, and ultimately, growth.

Mitigating circumstances

Markets are pricing higher inflation risks from the Iran conflict alongside stable growth. So far, we see a combination of structural and cyclical forces as mitigators of the impact on economic activity:

- The global economy not being as exposed to oil shocks as it was in the 70s and 80s. The energy intensity of output and the wallet share of energy in consumption have both declined markedly.

- Oil inventories have been drawn down and consumer demand has rotated to less energy-intensive activities.

- Larger U.S. tax rebates from 2025 more than offset the hit to U.S. purchasing power this spring.

- “Financial accelerators” are not kicking in. In stark contrast to past major oil shocks, equity and home prices remain near all-time highs and credit spreads are tight.

Even in Europe, the economic drag, while real, could be less severe than 2022. Electricity prices remain well behaved across the continent due to robust wind and solar power generation. Moreover, leading economic indicators point to positive, albeit low gear, growth.

Risks remain

In an adverse re-intensification scenario, the economic effects of the conflict could become more pronounced in the second half of the year as fiscal support fades in the U.S. and inventories are drawn down globally. India may prove to be an important test given the country’s scale and energy dependence on the Middle East.

The Iran conflict could also have longer-term implications, particularly after a staccato of geopolitical shocks in recent years. Ramifications include more inflation volatility, higher stock-bond correlations, higher term premia, and a ramp in military spending, with consequences for portfolio diversification and opportunities across public and private markets.

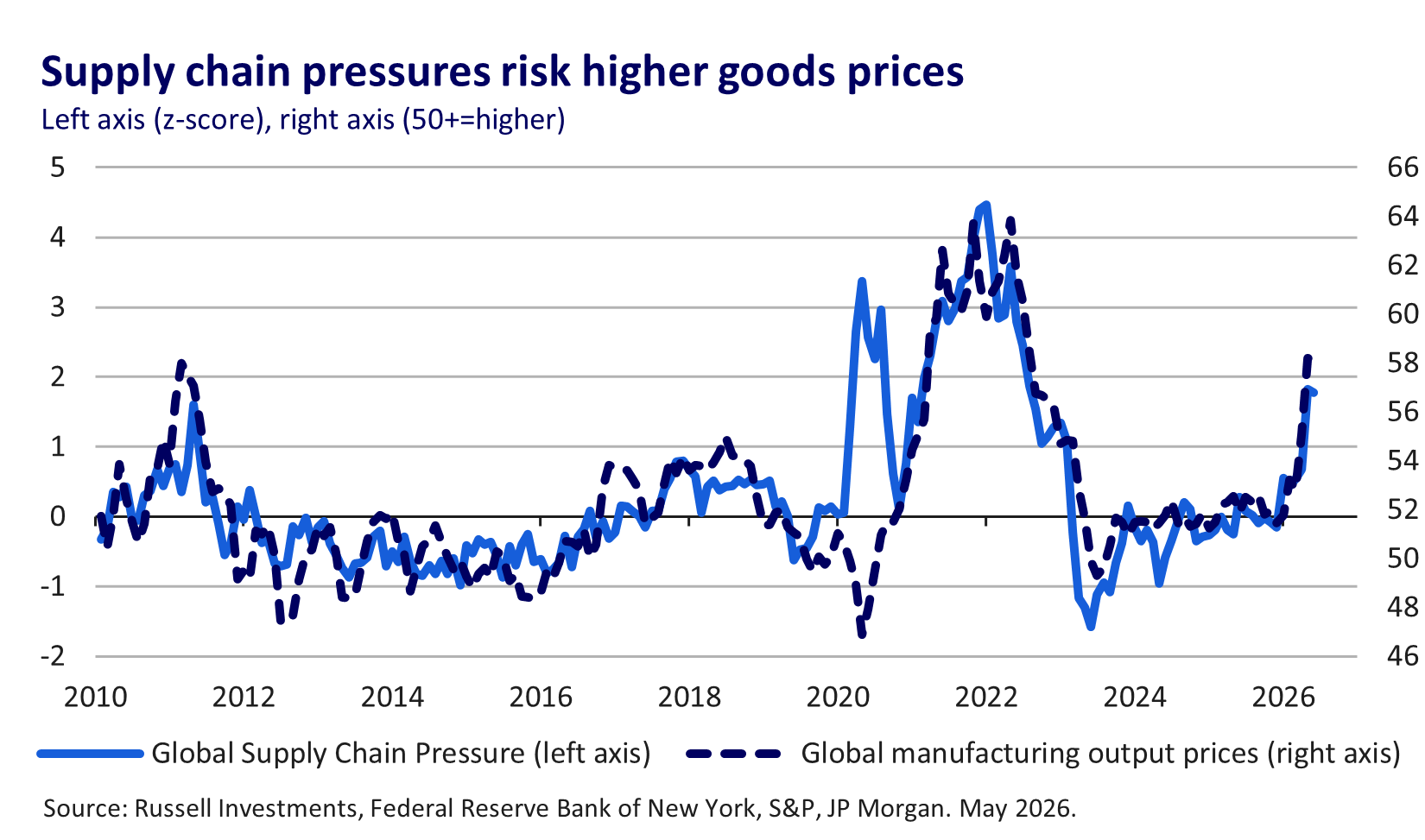

Watchpoint 2: Supply chains strain

The biggest yellow flag facing markets are the signs of emerging supply chain pressures. The Federal Reserve Bank of New York’s Global Supply Chain Pressures Index has spiked to its highest level since 2022. Similar disruptions from the COVID lockdowns contributed to the last inflation surge, and global manufacturers are raising goods prices at a relatively rapid pace again.

Watchpoint 3: Interest-rate volatility

The prospect of rising inflation has led market expectations for policy rates to swing sharply, pivoting from rate cuts to hikes at the onset of the Iran conflict. Our outlook for the Federal Reserve has been more consistent in favoring a protracted hold. While higher energy prices could lift headline inflation, the Fed remains focused on labor market conditions and underlying inflation. On these measures, the backdrop looks more benign. Inflation expectations are well anchored, shelter inflation continues to moderate, and wage growth is consistent with a balanced labor market.

The sharp rise in yields has reshaped the valuation of U.S. Treasuries. Whereas we viewed the front end of the yield curve as expensive at the start of 2026, two-year Treasuries now offer more compelling value. In Europe, inflation plays an even bigger role in monetary policy decisions and we expect hikes from the Bank of England and European Central Bank. Globally, we see good value in several developed market sovereign bonds, including UK Gilts and Japanese government bonds, where investors have priced in higher policy and political risk premia in recent months.

Investor implications

If the first half of 2026 has reinforced one lesson, it is that markets are more resilient than many anticipate. New sources of friction have emerged, including geopolitical tensions, supply chain pressures, and heightened interest-rate volatility, increasing the complexity of the risks facing investors.

Yet resilience has prevailed. Strong market fundamentals continue to support a constructive outlook. For investors, this environment reinforces the importance of maintaining portfolio durability through market regimes, balancing participation in growth opportunities with the diversification needed to withstand periods of stress.

Halfway through the year, the good news is that markets appear to have passed the pressure test. Now the focus is on sustaining it.

This outlook reflects our views as of June 18, 2026. Given the rapidly evolving geopolitical environment, including recent reports of a potential Iran agreement, market conditions and risks may change. We encourage readers to follow our Market Week in Review for ongoing updates and analysis.

Asset class preferences

This snapshot highlights our latest asset class views. Click on each box to learn more about the opportunities and risks shaping our perspective.

Regional snapshots

United States

The U.S. economy remains resilient, though its upside potential has moderated as higher energy prices and supply chain pressures complicate the outlook. We look for real GDP growth to hold above 2%, supported by improving manufacturing activity and labor market conditions, the AI buildout, loose financial conditions and fiscal policy. Corporate earnings are supercharged, helping markets advance, though price and fundamental leadership has narrowed back toward the AI theme. We continue to see encouraging signs that generative AI is moving up the productivity J-curve, with potential benefits for company revenues and profit margins over time. The Federal Reserve is likely to remain on hold as higher headline inflation is balanced against anchored inflation expectations, moderating shelter inflation and benign wage inflation. Risks include a protracted Iran conflict, interest-rate volatility and expensive valuations.

Canada

2026 so far has offered investors a reminder that Canada’s economy can look very different from its stock market. Despite the economy having entered a technical recession, Canadian equities are trading near their all-time highs, driven in part by higher energy prices. Earnings continue to hold up, as many Canadian companies derive a substantial portion of their profits from countries like the U.S., which have seen greater economic resilience. For the remainder of the year, we expect the Canadian economy to remain under pressure but remain more constructive on the financial markets.

Eurozone

After the war in the Middle East broke out, we scaled back our exposure to European stocks to neutral. As an energy importer, the eurozone was seen as susceptible to the energy price shock caused by the closure of the Strait of Hormuz. Another headwind for the economy and markets emerged as the ECB raised rates by 25 basis points in June and is expected to follow up with at least one more hike by the end of the year. By contrast, fiscal stimulus through 2026/27 and improving fundamentals for European corporates provide a positive counterweight. The recent agreement between the US and Iran to re-open the Strait of Hormuz, if sustained, could remove the headwinds faced by euro area stocks during the conflict.

United Kingdom

Compared to the start of 2026, events in the Middle East have flipped the outlook for inflation and interest rates in the UK. From previously pricing rate cuts, money markets now expect the Bank of England to raise rates at least once by the end of the year. Like its European neighbors, the UK was seen as vulnerable to the energy supply shock, which now is likely to recede with the re-opening of the Strait of Hormuz. In addition, long-term UK gilts have embedded a significant risk premium due to the uncertainty around Prime Minister Starmer’s position and the fiscal outlook. As underlying economic growth is weak, we think that rate hike expectations are overdone, and gilts offer decent value despite the political unrest.

China

The second half of 2026 is likely to see a pick-up in government stimulus aimed at infrastructure investment, especially if the Middle East conflict extends. The consumer remains fairly subdued, with modest wage growth and lingering concerns about the state of the housing market. Despite this backdrop, we believe Chinese equities still offer good opportunities given cheap valuations and corporate earnings that look healthier than the economic backdrop.

Japan

We believe that Japanese equities look attractive, driven by a combination of corporate governance reforms and potential expansionary fiscal policy from Prime Minister Takaichi’s recent election win. A high stockpile of oil has meant that Japan has proven resilient to the increase in oil prices, but this remains a key watchpoint. The Bank of Japan are likely to raise interest rates once or twice over the next twelve months, while the Japanese yen remains one of the cheapest currencies in the G10.

Hong Kong, Singapore, Taiwan

Hong Kong

Hong Kong economic activity has been responding to the reduction in interest rates, while demand for exports has remained healthy. The property market is a key watchpoint, with early signs that it might have inflected back into positive territory – which could further improve consumer confidence and spending.

Singapore

We expect Singaporean growth to be robust over the next twelve months, with the Middle East tensions a key watchpoint. Singapore has not offered fuel subsidies like many other Asian economies, and historically we have seen oil prices impact the economy with a longer lag than the rest of Asia. Whilst the Monetary Authority of Singapore tightened policy slightly in April, we expect the hurdle for further tightening is quite high.

Taiwan

The Taiwanese economy continues to see significant support from the demand for semiconductor chips, while domestic demand has been improving through the first half of 2026. The Taiwanese equity market has begun to look expensive relative to other Emerging Markets, and we have observed a substantial increase in leveraged activity in the market given the excitement around AI and the demand for chips.

Australia and New Zealand

We are looking at a sub-trend growth environment for the rest of 2026 and into 2027 for the Australian economy. Consumer spending and confidence has fallen following the increase in interest rates from the Reserve Bank of Australia. Productivity remains a challenge for the economy, with the Reserve Bank reiterating its view that economic growth is effectively being constrained at 2%. As a result, corporate earnings are likely to look lackluster compared to global earnings. We believe government bonds in Australia still offer good value, while the Australian dollar is now close to our estimate of fair value.

The key focus for the New Zealand economy in the second half of 2026 will be monetary policy, given the Reserve Bank of New Zealand’s hawkish tilt at the May meeting. The economy is still experiencing tepid growth, inflation is not that far away from target and unemployment is relatively high, so an aggressive shift to interest rate hikes could risk a further step down in the economic situation. Equities appear expensive relative to global equities, while government bonds offer an attractive skew.

Feature topics

IPOs taking center stage

By Athan Dounis

Key takeaways:

- Landmark initial public offerings (IPOs) could signal a new phase where value accumulated in private markets begins to transition into public markets.

- Benchmark-driven buying may increase volatility as passive investors absorb newly listed shares.

- These IPOs could reinforce, rather than reduce, concentration in technology and AI markets.

Private giants move toward public markets

Entering 2026, investors expected a gradual reopening of the IPO market following several years of subdued exit activity. Six months later, that reopening appears to be accelerating, with SpaceX's public debut potentially marking the start of a new mega-IPO cycle that could also include OpenAI and Anthropic. The number of the IPOs this year might remain relatively modest, but the scale of the upcoming listings is unprecedented. When completed, these transactions will rank among the largest venture-backed IPOs in history.

After years in which capital accumulated inside private markets, these listings could test whether public markets are prepared to absorb the next generation of mega-cap growth companies and if they will broaden market opportunities or concentrate them further.

Over the coming months, investors should watch whether these IPOs improve liquidity and valuation discovery, how benchmark-driven demand influences trading dynamics, and whether they broaden market opportunities or reinforce existing concentration trends.

Portfolio implications beyond the listing

One of the defining features of the current investment cycle is the concentration of value inside private markets alongside a drop in IPO activity since 2021. Investors have waited years for meaningful distributions, while private companies continued raising capital at increasingly ambitious valuations. Estimates suggest global venture funding reached a record $330.9 billion in Q1 2026, driven largely by AI-focused companies.1

For investors with exposure through venture funds and growth-equity mandates, successful IPOs could improve liquidity, provide clearer valuation benchmarks, and support a broader reopening of the exit market. The transition from private to public markets may also transform years of accumulated gains into significant public equity positions, creating new concentration, benchmark, and implementation challenges.

Public market investors, meanwhile, may gain long-awaited access to companies that have historically been available only through private markets. Yet access alone does not guarantee attractive returns. Given elevated valuations, limited free float, and significant investor demand, share prices could become disconnected from fundamentals during the initial stages of trading.

As a result, the key issue may not be whether these companies list, but how they are valued and incorporated into portfolios. Large IPOs can reshape benchmark exposures, alter sector weights, and amplify concentration risks, particularly if passive demand accelerates shortly after listing.

Over the coming months, successful listings could encourage additional companies to pursue public offerings and reinforce confidence in AI-related investments. Equally, disappointing outcomes could slow the reopening of the IPO market and temper enthusiasm across both public and private markets.

Benchmarks as market movers

There is no single index inclusion date and historically newly listed companies often waited months before becoming benchmark constituents.

However, recently that timeline is shortening as index providers adapt their rules for larger IPOs, potentially bringing benchmark-driven demand into the market much earlier than investors have experienced in previous listing cycles.

Potential index inclusion timelines for mega IPOs

Source: S&P Dow Jones, FTSE Russell, NADAQ, MSCI. Data as of June 2026

This could create an unusual dynamic. The initial free float of SpaceX is expected to be relatively small despite its enormous market capitalization. At the same time, passive investors tracking major benchmarks would be required to purchase shares regardless of valuation.

Over the next six months, the interaction between constrained supply and benchmark-driven demand could become an important source of volatility. For active investors, this may create opportunities to exploit technical dislocations. For passive investors, it highlights an increasingly important reality: benchmark construction is becoming a larger driver of market outcomes.

New listings test market leadership

Investors are also looking at whether upcoming IPOs increase diversification or reduce it. Public markets have already experienced a period of extraordinary concentration, with a small number of mega-cap technology companies driving a disproportionate share of returns.

At first glance, the arrival of new trillion-dollar companies appears to broaden the opportunity set and increase diversification. Yet the opposite may occur. The likely beneficiaries of investor demand, passive inflows and benchmark inclusion are the same companies already attracting the largest pools of capital in private markets.

Data shows that investment activity has become increasingly concentrated around a handful of AI leaders, while fundraising continues to favor the largest managers and franchises.

The next six months may therefore represent a continuation of an existing trend rather than a reversal. Instead of capital dispersing more broadly throughout markets, investors may witness a transfer of concentration from private markets into public markets.

Investor implications

The potential listings of SpaceX, OpenAI and Anthropic represent more than a reopening of the IPO window; they are a test of whether public markets can absorb the enormous value that has accumulated in private markets over the last decade.

The opportunities are clear: improved liquidity, stronger exit markets and broader access to some of the world's most important growth companies. However, valuation excesses, benchmark-driven volatility and greater market concentration remain key watchpoints. For investors receiving public shares through existing private-market holdings, overlays and other risk-management tools may help manage concentration and implementation risks as positions become liquid.

Irrespective of how the IPOs land, the next six months may usher in a new era for both public and private markets investors.

1 KPMG Private Enterprise Venture Pulse Q1 2026 Global Report

Finding opportunity in private credit

By Keith Brakebill

Key takeaways:

- The next phase of the refinancing cycle is likely to separate strong private credit managers from the rest.

- Structural outflows may create better lending opportunities rather than signal broad credit weakness.

- Software risks remain concentrated and are not representative of the broader private credit market.

- Investment grade private credit continues to stand out as an attractive source of yield and diversification.

Refinancing resets the private credit market

Private credit has attracted no shortage of attention this year. Headlines have focused on fund outflows, software exposure, and questions about the durability of returns as borrowers face a higher-rate environment. Yet much of the recent discussion has centered on pockets of the market rather than the broader opportunity set.

The private credit landscape in 2026 is largely shaped by the current refinancing cycle. Many borrowers benefited from low-rate pandemic-era financing conditions and now face materially higher borrowing costs. Between 2026 and 2029, approximately $1.9 trillion of U.S. leveraged loans and high-yield bonds are expected to mature1, creating a more selective environment for both borrowers and lenders. While this environment may create greater dispersion among borrowers, it may also create opportunities for disciplined investors to access stronger lending terms and potentially more attractive risk-adjusted returns. Over the next six months, we believe that investors should pay close attention to three developments that may create opportunities: semi-liquid fund outflows, concentrated software-sector risks, and the growing appeal of investment grade private credit.

Recent outflows may not signal weakness

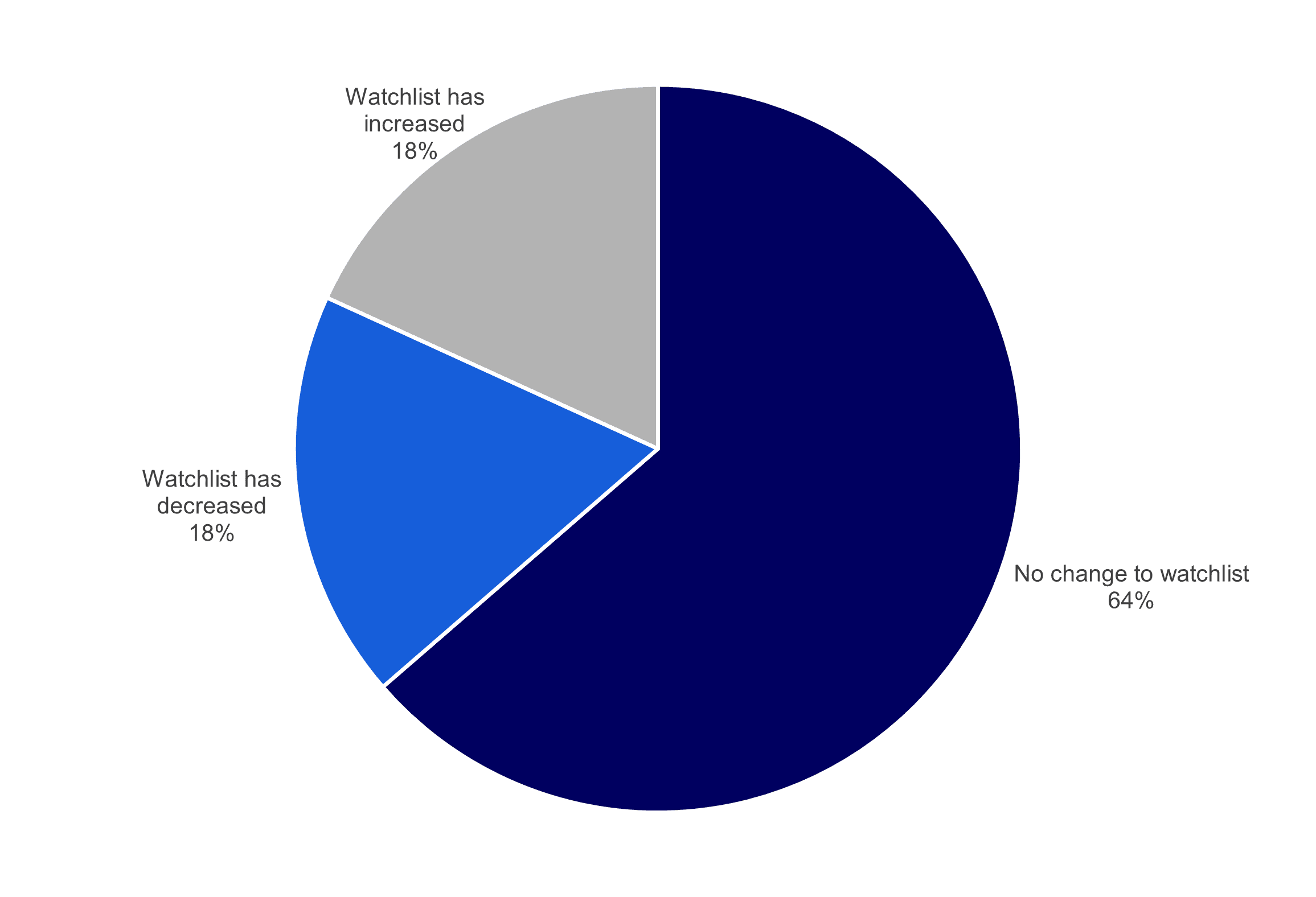

Recent headlines around outflows from semi-liquid vehicles, including interval funds and business development companies (BDCs), have fueled concerns about the health of private credit. Yet these developments in our view are the result of liquidity dynamics rather than widespread deterioration in loan quality.

Our manager monitoring data shows little evidence of broad-based credit deterioration. Nearly two-thirds of our monitored private credit managers experienced no change in watchlist status during the latest review period. Even with the outflows, most private credit vehicles have liquidity management tools designed to prevent forced asset sales. As a result, recent redemption activity says more about fund structures than underlying credit quality.

As capital becomes less abundant, lenders regain negotiating leverage for stronger terms, better pricing, and improved protections on new investments. The result is a more attractive opportunity set for investors than when fundraising activity and competition for deals peaked.

RI PC Managers: Changes to Watchlist from Q3 2025

Source: Russell Investments, April 2026

Software risks warrant a selective approach

Over the past year software and affiliated sectors accounted for more than 28% of total loan assets managed by BDCs and interval funds2, representing a meaningful concentration within parts of the private credit market. At the same time, advances in AI are creating uncertainty around the long-term durability of some software business models. Investors should avoid extrapolating these risks across the broader private credit universe outside the BDC world that has grown to $1.7 trillion globally3 . In our view, these developments reinforce the importance of selectivity, underwriting discipline, and sector expertise rather than signaling broad-based weakness across private credit.

Many software companies continue to generate strong cash flow and maintain recurring revenue streams that support their ability to meet loan obligations. As a result, investor focus is increasingly shifting toward long-term competitive positioning. The challenge is identifying which businesses can sustain pricing power and customer demand as technology evolves, and which may face increasing pressure on future earnings power.

This distinction will become more important as refinancing activity accelerates. Companies with durable business models are more likely to retain access to capital on attractive terms, while weaker issuers may face higher borrowing costs or more restrictive financing conditions. As a result, performance dispersion across borrowers and managers could become more pronounced, making credit selection an increasingly important driver of outcomes.

Investment grade private credit gains attention

Historically favored by insurance companies, investment grade private credit has expanded to roughly $300 billion and is attracting interest from a broader set of investors, including pension plans and healthcare organizations. As public investment grade spreads remain compressed, investors are increasingly exploring private markets as a potential source of additional income while maintaining a focus on credit quality.

The backdrop in public markets helps explain why. Generating meaningful incremental yield through public markets increasingly requires larger and riskier credit overweights. As of May 2026, U.S. investment grade spreads stood at approximately 0.74%, while European investment grade spreads were roughly 0.83%. Those levels are near 30-year lows and leave investors with limited compensation for taking additional credit risk.

Investment grade private credit may offer an alternative. Much of the market consists of asset-based loans backed by identifiable collateral and contractual cash flows, creating opportunities to earn an illiquidity premium while maintaining a high-quality credit profile. For investors seeking additional income within core fixed income allocations, investment grade private credit may provide an attractive complement to public markets without requiring a significant move down the credit spectrum.

Investor implications

Recent headlines have focused on outflows and concentrated sector risks, but the more important development is the refinancing cycle now underway. As borrowers return to the market, differences in business quality, capital structures, and financing needs are likely to become more apparent.

Rather than viewing current market developments as signs of broad weakness, investors may benefit from focusing on areas where disciplined underwriting, strong collateral structures, and experienced manager selection can help identify resilient sources of income and diversification within private credit.

1 https://www.moodys.com/web/en/us/insights/credit-risk/outlooks/mco-20-october-2025.html

2 https://www.spglobal.com/ratings/en/regulatory/article/bdcs-exposure-to-software-stays-high-steady-s101675136

3 https://www.preqin.com/insights/global-reports/2025-private-debt

Investing in the electricity buildout

By Michael Steingold

Key takeaways:

- U.S. electricity demand is growing at its fastest pace in decades, increasing the need for investment across generation, transmission, and grid infrastructure.

- Utility and infrastructure consolidation reflects the growing value of scale as operators seek to meet rising power and data center demand.

- Geopolitical uncertainty and energy security concerns could accelerate investment in renewables, particularly solar and storage.

- Meeting future electricity demand will require investment across the entire power ecosystem in both public and private markets.

Electricity demand outpaces available capacity

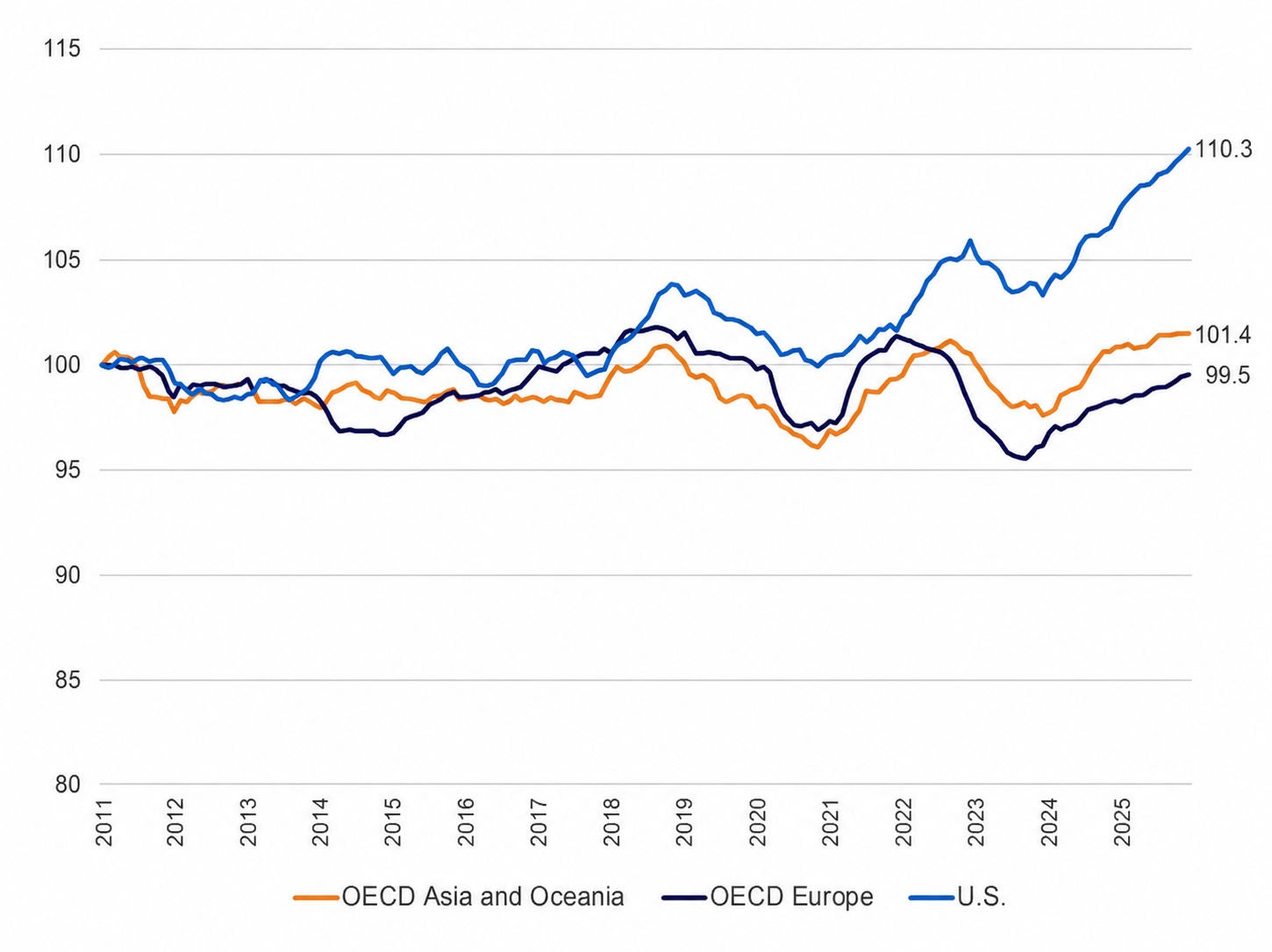

For years, infrastructure investors seeking growth in the energy sector were largely limited to oil and gas. Today, global electricity demand is entering a new phase of growth. In the U.S. alone, electricity demand grew roughly 3% last year, up from less than 1% annually before COVID. Growth is even more pronounced in areas where data centers and digital infrastructure are being built. PJM, the grid operator serving the Mid-Atlantic region and Northern Virginia's data-center corridor, projects electricity demand growth of approximately 5% annually over the next decade.

What distinguishes this cycle from previous technology-driven investment periods is that commercial demand is expected to surpass residential demand in 2027 for the first time on record1. At the same time, infrastructure capital expenditure is being deployed both to maintain the aging grid for existing demand and to accommodate projected growth in electricity consumption.

Total Electricity Consumption (indexed Jan 2011 = 100, trailing 12 months)

Source: International Energy Agency (raw data) and Russell Investments (rebasing)

The challenge is increasingly one of delivery. Building generation, transmission, and grid infrastructure takes time, creating a mismatch between the pace of demand growth and the industry's ability to add new capacity. As the second half of 2026 unfolds, investors should watch how the industry responds to that capacity gap. Two themes stand out: consolidation among operators seeking greater scale and continued investment in renewable generation.

Scale shapes the next phase of infrastructure investment

Before COVID, a large data-center lease typically required about 30 megawatts of power. Last year, the market saw multiple leases for 1 gigawatt, reflecting a dramatic increase in power requirements. Alphabet, Amazon, Meta, and Microsoft added roughly 25 gigawatts of new demand in 2025 alone, equivalent to approximately 2% of total U.S. power-generation capacity.

Yet only about 5 GW of capacity was built and energized over the same period, leaving a substantial buildout ahead across generation, transmission, and grid infrastructure. Recent utility-sector transactions suggest scale is becoming increasingly important as operators respond to rising power demand.

Growing M&A activity among utilities and infrastructure operators could emerge as a key driver of market activity. NextEra Energy's proposed acquisition of Dominion Energy, which is expected to close in the first half of 2027, would create the world's largest regulated electric utility business and one of North America's largest energy infrastructure platforms. Greater scale may become increasingly valuable as operators work to expand transmission networks and meet rising power demand. NextEra's plans to develop more than 30 energy centers across the United States2 highlight the magnitude of the investment needed to address future capacity requirements.

Energy security supports renewable investment

The Iran conflict has renewed attention on energy security. While the global economy is less exposed to oil shocks than it was in previous decades, geopolitical fragmentation continues to reinforce the value of diversified energy systems, domestic infrastructure investment, and resilient supply chains. Since Russia's invasion of Ukraine, Europe has accelerated efforts to diversify energy supply, supporting investment across renewables, storage, transmission, and grid modernization.

Renewables remain attractive as one of the lowest-cost sources of incremental generation capacity. The share of renewables in global electricity generation, led by solar, is expected to increase from 42% in 2025 to 50% by 20303. Simultaneously, intermittency challenges reinforce the need for a diversified power system in which renewables are supported by storage, reliable generation, and a stronger grid. Advanced nuclear and next-generation storage remain important long-term considerations, although supply chain, policy, and commercialization hurdles are likely to limit their near-term impact.

Investor implications

Meeting future electricity demand will require investment across generation, transmission, storage, digital infrastructure, and grid modernization. As utilities, infrastructure operators, and developers work to expand capacity, opportunities may emerge across both public and private markets.

Listed infrastructure provides exposure to utilities, transmission networks, and grid infrastructure, while private markets offer greater access to renewables, digital infrastructure, and other long-duration assets. Together, they provide exposure to different parts of the power ecosystem supporting rising electricity demand.

Infrastructure's inflation sensitivity and diversified sources of cash flow may become increasingly valuable if energy, supply chain, or capacity constraints place renewed pressure on prices.

1 https://www.reuters.com/business/energy/us-power-use-beat-record-highs-2026-2027-ai-use-surges-eia-says-2026-05-12/

2 https://www.cnbc.com/2026/05/18/nextera-nee-dominion-energy-d-data-center-ai.html

3 https://www.iea.org/reports/electricity-2026/supply

Common client questions

Supply chain pressures have increased to their highest levels since 2022, raising concerns about goods-price inflation. While today’s environment differs from the pandemic period, prolonged disruptions could increase production costs and place upward pressure on inflation, particularly if inventories decline further.

AI is increasingly contributing to productivity improvements across industries. Companies are adopting generative AI tools at scale, supporting efficiency gains and potentially enhancing revenue growth and profit margins. While concerns remain around employment impacts, evidence so far points more toward productivity benefits than widespread job displacement.

The current environment highlights the value of balancing growth opportunities with portfolio resilience. Diversification across asset classes, regions, and investment styles can help investors participate in long-term growth while managing risks associated with geopolitical events, inflation, and market volatility.

Key risks include the economic effects of the Iran conflict, rising supply chain pressures, and increased interest-rate volatility. These factors could influence inflation, growth, corporate earnings, and market valuations, making diversification and active risk management increasingly important.

Strong corporate earnings, improving manufacturing activity, resilient labor markets, and early productivity gains from artificial intelligence have helped support economic growth and investor confidence. While geopolitical tensions have created volatility, underlying economic fundamentals have remained healthy, enabling markets to recover quickly from periods of stress.

Interest-rate expectations have become more volatile due to inflation concerns. However, central banks remain focused on underlying inflation and labor-market conditions. Rising yields have improved valuations in several sovereign bond markets, creating opportunities for investors seeking income and diversification.

A large refinancing cycle is creating a more selective lending environment, potentially benefiting experienced private credit managers. Investment-grade private credit remains particularly attractive for investors seeking additional yield, strong collateral protection, and diversification beyond traditional fixed income markets.

Many companies have benefited from resilient consumer demand, investment in AI infrastructure, improving manufacturing activity, and supportive financial conditions. These factors have helped sustain profit growth even as geopolitical risks and policy uncertainty have increased.

Electricity demand is growing rapidly due to data centers, digital infrastructure, and broader economic electrification. Meeting future demand will require substantial investment in power generation, transmission networks, storage, and grid modernization, creating opportunities across both public and private markets.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.