Executive summary:

- The 2017 Tax Cuts and Jobs Act is set to expire at the end of next year, which could mean potentially higher tax bills

- If extended by the new administration, that will likely lead to a higher budget deficit

- The deficit will have to be paid for eventually, which could also mean potentially higher tax bills

While new tax proposals are grabbing election headlines, it’s important to remember that campaign rhetoric is not necessarily future policy. A case in point is the 2017 Tax Cuts and Jobs Act, which is set to sunset at the end of next year. If its key provisions are extended, that could lead to reduced government revenues and a higher federal deficit. This could lead to higher taxes in the future. If the key provisions are not extended, that could result in higher taxes immediately.

In this blog I am going to look at the implications of extending (or not) the tax provisions of the TCJA and how you can help your clients prepare for the potential for higher taxes either now or in the future.

The pending expiration of the 2017 Tax Cuts and Jobs Act

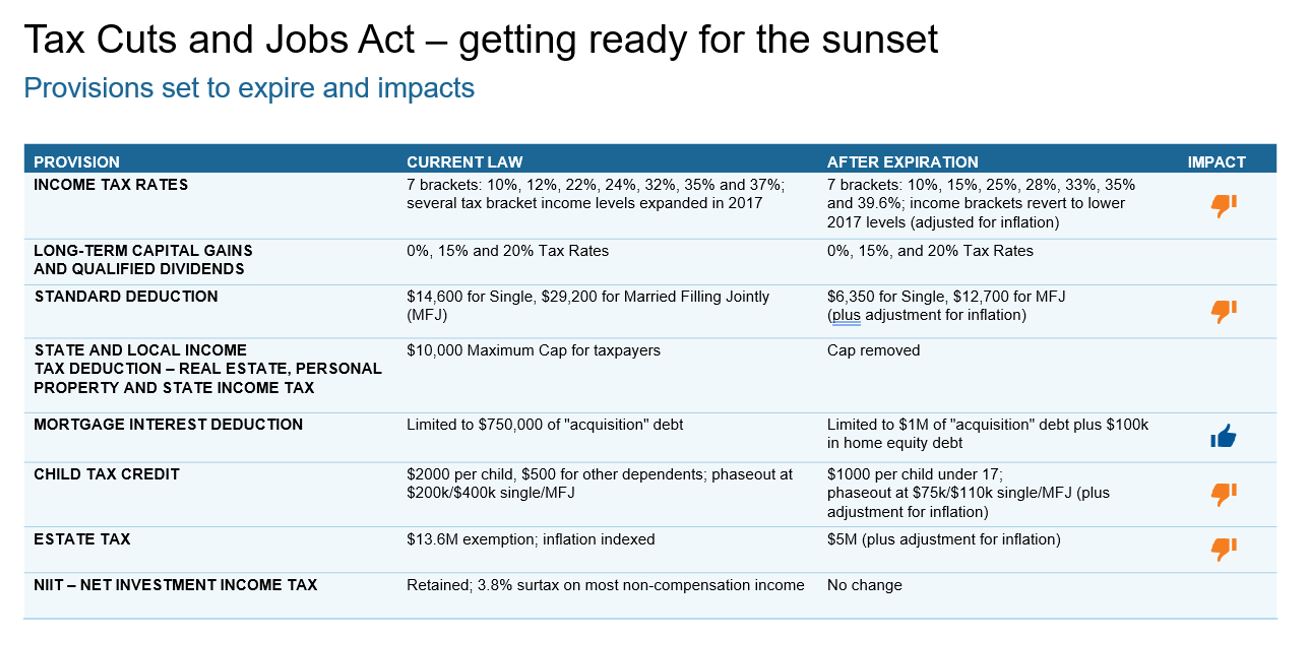

First, let’s make clear that no matter who takes office next year nor which political party holds the majority in either the legislative or executive branches of government, it is highly unlikely that the TCJA will get extended past its 2025 expiry date with no modifications. This is because the original bill was full of tax-related adjustments and provisions that 1) have already expired and 2) were directed at specific corporate entities and industries.

That being said, the provisions that draw the most eyeballs, and the most questions, are related to individual income taxes, investment taxes, specific tax credits that benefit individuals, and estate taxes. Assuming there is appetite within the different branches of government to extend some or most of the TCJA provisions next year, it will be done via a new bill. It’s safe to assume there will be additional provisions included. As for the specifics, we are watching and listening carefully, so stay tuned as things come into focus.

(Click image to enlarge)

The cost of extending the TCJA tax cuts

To understand the implications of extending the TCJA tax cuts, let’s take a lesson from the 1600s, the nadir of the Age of Discovery. Sir Isaac Newton is known as one of the most influential scientists of that century. He is often referenced as “discovering” gravity when he got bonked in the head by an apple that fell out of a tree. But he is also well known for a phrase that is particularly applicable to the subject of tax cuts: “Every action has an equal and opposite reaction”.

Tax cuts have a positive impact on those receiving the benefit: reduced payments (i.e. fewer taxes paid is more money in your pocket). But tax cuts also mean less revenue coming into government coffers. We may take this for granted as we think about how to spend our newfound monies – but the Congressional Budget Office (CBO) does not. It calculates the fiscal impact of bills that are submitted for Congressional approval. Its big concern is: “How much is this going to cost?”

There is a cost, obviously, of extending the 2017 TCJA. If most of the major provisions, largely highlighted in the table above, were to be extended for an additional 8-10 years, the total cost would be an increased budget deficit of around $4 Trillion by 2034. This does not include borrowing costs in the form of interest payments on the debt that would need to be issued to fund that additional deficit. This is not a small number.

We are already in a sizable deficit situation as a country. The deficit currently stands at around $35.3 trillion, according to the U.S. Treasury,1 so which provisions get extended, expanded, or contracted and for how long will be dependent on the appetite in Washington, DC next year to increase the budget deficit.

Hanging in the Balance

What can we expect going forward?

Even if most of the 2017 TCJA provisions were to be extended next year, we all need to be prepared for a different reality: the increased probability of more and higher taxes in the future.

At some point ‘we will need to pay the piper’ as the saying goes.

The two charts below illustrate the issue. The budget deficit is the difference between outlays (spending) and revenues (income from taxes). The gap today is wide and expected to widen further over the next 10 years. By 2034 the gap is expected to be 6.1% of gross domestic product (GDP).2 This level has only been exceeded three times since the Great Depression: a short period after WWII (rebuilding the world), the Great Financial Crisis (GFC), and during the recent Covid pandemic. The main drivers of the deficit today and its projected expansion is spending on Social Security and Medicare, known as Mandatory Spending. Discretionary Spending, which covers almost everything else (i.e. defense, transportation, education, veteran’s health care, and so on) is declining as a percentage of spending and expected to continue declining. This estimate from the non-partisan CBO only considers what is known today – it does not consider an extension of the 2017 TCJA.

How are we funding this? With more debt. U.S. government debt is almost at 100% of GDP this year3, a level we have seen only once (post-World War II) since the beginning of the prior century. The CBO also projects that the debt to GDP ratio will increase through 2050 when it is expected to hit a new peak of 172% of GDP.

It’s doubtful there will be much of an appetite in Washington or elsewhere to cut either Social Security or Medicare. Hence, the two paths forward are likely to be that the budget deficit and debt levels continue to increase and/or tax revenues and taxes in general increase.

(Click image to enlarge)

Source: Congressional Budget Office (CBO) - The Budget and Economic Outlook 2024-2034. Figure 1-2, Federal Debt Held by the Public (% of GDP) and Figure 1-3 Total Federal Outlays and Revenues (% of GDP). GDP = Gross Domestic Product

How to prepare now for future tax increases

When taxes dominate the headlines, the increased chatter presents the perfect opportunity to showcase the value you bring by shifting the focus from uncertain tax policies to what you can control for your clients. Anytime taxes are in the news, it makes clients and prospects more receptive about the value you offer on these topics.

So how can you help investors today to prepare for tomorrow?

First, help investors understand how taxes impact their investments. We’ve got a guidebook to help you through these conversations.

Second, it’s important for investors to be aware of what they hold in their portfolios and the annual tax bill they pay on those assets. Our Tax Impact Comparison Tool can help you dig into the details and help you come up with a strategy to minimize the friction taxes are having on your clients’ investment returns. You can help your clients stay on a solid long-term investment path with tried-and-true tax managed investment strategies that can help them meet their long-term goals.

Third, whether tax laws change or not, investment taxes will continue to be a headwind for achieving successful investment outcomes. Positioning yourself as a tax-smart advisor not only differentiates your practice but also increases the value you offer clients and prospects alike.

Want to understand the potential impact on a client’s portfolio? Reach out to us—we can help you assess and implement tax-managed strategies that put you ahead of the curve.

1 Source: https://fiscaldata.treasury.gov/americas-finance-guide/national-deficit/

2 Source: Congressional Budget Office

3 Source: https://www.usdebtclock.org/