Risk transfer potholes: How to avoid them or brace for impact

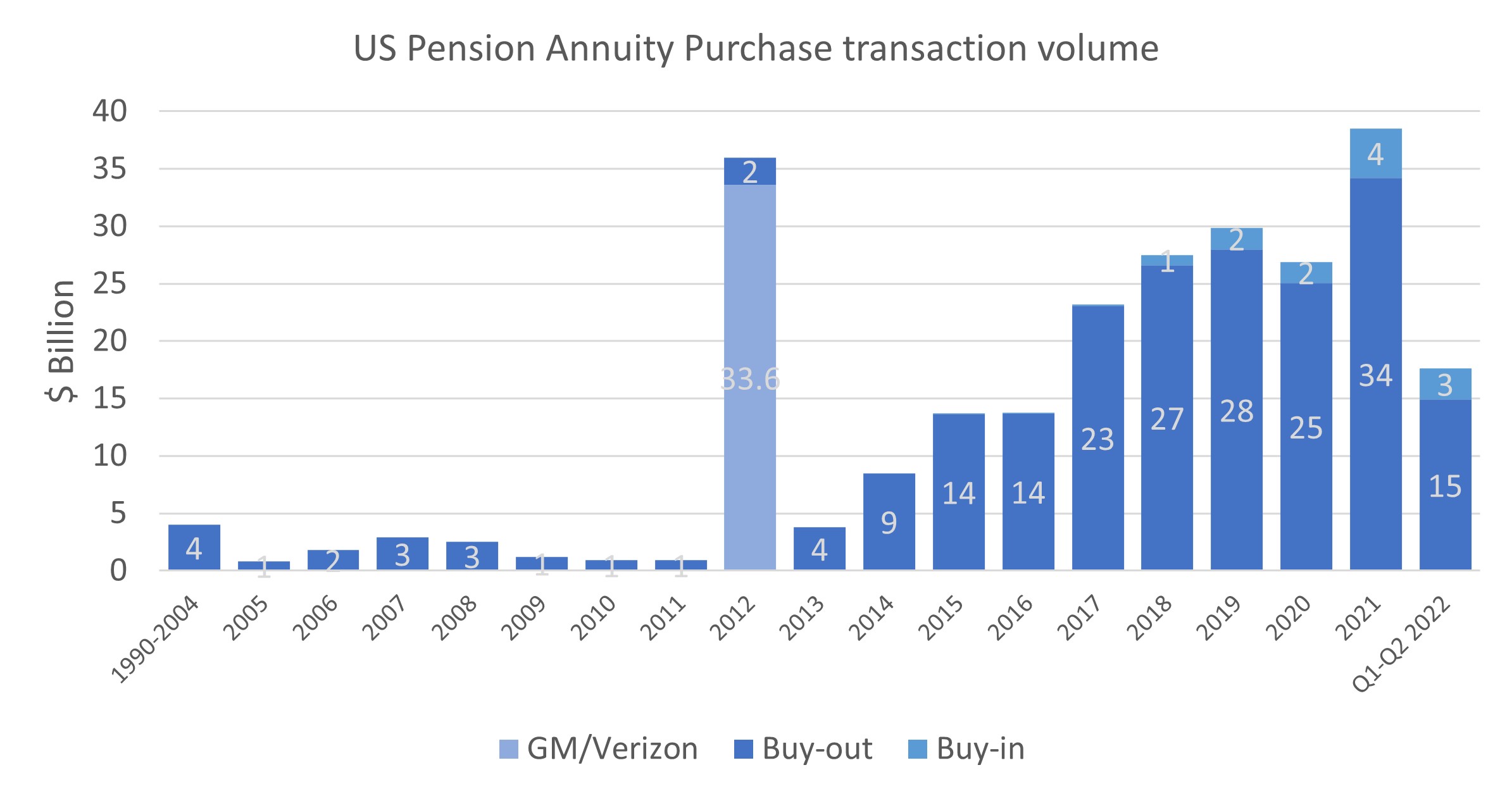

10 years have passed since the watershed year for pension risk transfer. In 2012, Ford, GM and Verizon all made landmark risk transfer transactions including lump sum cash outs and annuity purchases. Before that time, annuity purchases were rarely used, as shown in the exhibit1 below. Annuity purchases have since picked up significantly, with a record year in 2021 and 2022 set to be another record year, particularly with IBM’s recent announcement of a $16 billion transaction (not included in the exhibit below).

Lump sum offers were also relatively uncommon ten years ago. Due to a combination of changing lump sum conversion rules enacted with PPA, and the fact that the year 2012 was a falling rate environment (in addition to many other individual years since then), lump sum offers suddenly became mainstream.

After 10 years most U.S. corporate DB sponsors have pursued at least one form of risk transfer. The vast majority have seen proposals for additional risk transfer transactions put forward by their plan actuary or other advisors. Sponsors are often troubled with deciding when and if risk transfer makes sense. The decision is not inconsequential, nor is it always straightforward.

The trend toward annuity purchases is only accelerating (also shown in the exhibit above), and with improved funded status in 2021 more and more sponsors are considering ways to reduce the overall risk of the plan to the organization, and to reduce the plan’s footprint.

Here we hope to raise awareness of potential challenges and red flags sponsors may face when considering risk transfer. Since much of the low-hanging fruit of risk transfer has already been picked, we have observed that some advisors have become more creative and aggressive in pushing risk transfer when not necessarily warranted or in the long-term best interest of the sponsor. Having a broader understanding of what issues may arise will help plan sponsors know when risk transfer makes sense.

Low-hanging fruit

First, to be clear, risk transfer can have clear and tangible benefits in terms of cost savings and overall plan simplification. For example, sponsors can save significantly on PBGC premiums. Sponsors pay a PBGC flat-rate premium every year for each participant in the plan, regardless of the funded status. Due to a series of congressional acts, the flat-rate premium has increased from $35 per head in 2012 to $88 per head in 2022, and is still increasing with inflation.

Reducing headcounts via lump sums or annuity purchase in the plan directly brings down this cost, particularly for those with very small benefits where the cost to offload them is relatively low. There may also be reduced cost for managing a smaller participant base, less mailing cost for statements/notices, etc.

The risk transfer transactions most likely to pass muster involve well-funded plans considering an annuity purchase for a select group of retirees that will receive favorable pricing (e.g., retirees with low benefits), or a lump sum cashout in a favorable rate environment. These risk transfers rarely have adverse long-term consequences, which is probably why many have completed these projects already.

Pursuing risk transfer while underfunded

We cannot emphasize enough how detrimental risk transfer transactions can be for poorly funded DB plans. Risk transfer should be considered as part of either an endgame strategy, or a way to tidy things up a bit without causing the plan harm. Plans that are underfunded have not reached their endgame, and they need every available dollar to help generate returns to reduce their funding deficit.

Underfunded plans hoping to reduce cost with risk transfer should consider making a one-time contribution to offset the negative impact the risk transfer is likely to have, making sure that the funded status percentage is at least as high as it was prior to the transaction. In most cases, sponsors are better off waiting until their funded status has improved.

Here is a simple example. Plan A holds $80 million in assets with $100 million in liabilities—80% funded on a mark-to-market basis. Now, consider if Plan A completes a $20 million annuity purchase, and let’s assume they get at par pricing (i.e., the assets and liabilities are the same). The current portfolio is expected to return 7% per year. How will this transaction affect their funded status percentage, and how much more will it cost over the long-term to fully fund the plan?

The results are summarized below. These numbers take into account the cost savings for reducing PBGC head counts, and they include the one-time fee associated with pursuing this type of transaction.

| Pre-annuity purchase | Post-annuity purchase | |

| Assets ($M) | 80 | 60 |

| Liabilities ($M) | 100 | 80 |

| Funding deficit ($M) | 20 | 20 |

| Funded status | 80% | 75% |

| Expected return | 7.0% | 7.0% |

| Expected annual return ($M) | 5.6 | 4.2 |

| Estimated years to become fully funded | 13 | 14 |

| Estimated contribution requirements before fully funded ($M) | 6.2 | 8.8 |

| Total expected flat-rate premiums over the next 15 years ($M) | 1.4 | 1.1 |

While PBGC flat-rate premiums declined by 20% with the annuity purchase, the much larger contribution requirements increased by over 40%. In addition, the time to become fully funded increased by one year. This is because after the annuity purchase, the plan is still left with the same deficit of $20 million, but with lower return potential to fill the gap due to decreased assets. This gap is eventually filled with contributions.

Before considering the cost savings from fee/premium reduction associated with risk transfer, make sure you have fully accounted for the long-term economic impact on the plan, and how well this aligns with your endgame goals. Alternatively, if the sponsors of an underfunded plan are strongly in favor of risk transfer, they could choose to contribute sufficiently to maintain the plan’s funded position without harming the long-term economics of the plan.

Misunderstanding plan termination cost

The plan termination process can be time-consuming and expensive. It is also riddled with uncertainties that cannot be clarified until late in the process. For example, a key factor in final pricing for a plan termination is how many non-retirees will elect to take a lump sum. A high take rate will generally lower the cost of plan termination, but a low take rate can force the sponsor to purchase more expensive annuities, raising the cost of the project.

Another example is the cost of an annuity purchase when the participant group has already been offered a lump sum, or certain targeted annuity purchases have taken place on the population. Any of these can increase the ultimate cost of plan termination.

Plan termination may be the goal for some plan sponsors, but they ought to go into the process with eyes wide open on the potential cost and resources required. Early in the process, plan termination cost will not have a specific dollar amount; it will have a range. While advisors may tout how low the cost may be, in reality the cost could be higher. The final cost may not be known until it is too late to stop the process of termination. The prudent approach, if pursuing plan termination, is to have extra cash on hand in case the cost is toward the high end of the range, to fill any outstanding deficit once the process is nearing completion.

Sponsors also ought to be cautious of estimates showing the cost of termination compared to the cost of maintaining the plan. This analysis will typically assess the present value of future costs, such as PBGC premiums, investment management fees and uncertainties like asset/liability mismatches. In reviewing this type of analysis, consider the following questions:

- Are active management fees netted out by expected outperformance of benchmarks?

- Are future expected investment returns taken into account to offset future costs?

- Has the impact of fixed income managers’ ability to partly or fully offset the impact of credit migration been taken into account?

- Is the impact of mortality assumption adjustments overstated?

- Is the liability estimate based on a discount rate using a broad market of bonds or a more selective group of bonds (which is typically harder to match with actual investments)?

While plan termination may be a key focus of the sponsoring organization, the additional cost in comparison to a maintaining/hibernating approach may be challenging to justify, when this cost is fairly represented.

Lump sums in a rising rate environment

For many plans, lump sum conversion interest rates are set for an entire year just prior to the plan year beginning. So, regardless of the interest rate experience during the year, lump sum amounts will not change. However, large lump sum cashouts typically trigger settlement accounting, which will value the transaction based on rates at the time of payout. This creates an interest rate arbitrage opportunity (from the sponsor’s perspective) when rates are falling.

When rates are falling, lump sums can be paid at a rate higher than the current market rate, which leads to an accounting gain (which increases corporate earnings). The opposite is also true, meaning that sponsors will likely experience a loss if they attempt a lump sum cashout in a rising rate environment, such as in 2022.

Since it is impossible to predict the future path of interest rates, sponsors considering a lump sum cashout should employ a wait and see approach for pulling the trigger on the project, depending on the path of rates. For those considering plan termination, which is likely to include a lump sum cashout, sponsors should understand the sensitivities of interest rate movements to their termination estimates and budget accordingly.

Settlement charges

As stated above, risk transfer transactions often trigger settlement accounting, which is basically a remeasurement taking into account the reduction in size of the plan. For plan using U.S. GAAP for accounting, when the sponsor is holding a large unrecognized pension loss, a risk transfer will generally force a portion of that loss to be recognized on the income statement immediately. This may have a sizeable negative impact on the earnings of the organization. For non-U.S. accounting, sponsors must immediately recognize just the gain or loss associated with risk transfer.

Settlement accounting can be avoided by using a buy-in annuity purchase, which is treated like a fully-hedged investment of the plan without formally removing any liability. However, a buy-in does not reduce PBGC premiums, at least until the buy-in is converted to a buy-out.

At par quotes

It is becoming more common to settle retiree obligations at a cost similar to plan liabilities, but make sure to know what the quote represents. Is the premium being quoted relative to the accounting liability at a certain point in time? If so, is the discount rate basis selective, or representative of the total bond market? Also, preliminary cost estimates can change when final pricing is quoted, and sponsors should be prepared for this possibility.

Hedge ratio drops

When retirees are removed from the plan, the duration of the liabilities will likely increase. Absent asset allocation changes and assuming an immediate rebalance to investment targets, the hedge ratio of the plan will likely decline. In advance of and through the annuity purchase, make sure to adjust your LDI strategy to align with hedge ratio objectives.

Actuarial assumptions impact

Depending on the group that is offloaded from the plan, there could be impacts on actuarial assumptions in future valuations, such as on mortality. For example, if mostly blue-collar workers are impacted by the annuity purchase, the actuary may find it more appropriate to assume a white-collar version of mortality for the remaining participants, which will increase liabilities and lower funded status. Understanding this impact beforehand is important as the sponsor is assessing the overall impact of the transaction and its impact on future risk transfer opportunities.

Asset-in-kind discounts

At times, in certain situations, insurers will choose to take some assets in-kind as part of an annuity purchase, leading to a possible discount in the annuity purchase premium as trading costs are avoided. Successful in-kind payments require efficient coordination between the insurer, investment managers and transition managers. The larger the transaction, the more likely that some in-kind payments will be possible.

Sponsors should not assume their portfolio necessarily holds all the assets the selected insurer will want to take. Since the insurer is often not selected until just prior to the annuity purchase transaction, coordinating and selecting desirable holdings can be a challenge, particularly for smaller transactions. Sponsors can pursue in-kind payments but should not assume any discount will necessarily come until the insurer has agreed to it.

Investment strategy for the liabilities to be transferred

When plan sponsors engage in risk transfer, the time horizon for that portion of their liability changes. This can mean a shift from a long-term, return-focused total portfolio, to a highly hedged short-term portfolio for the selected group that will be transferred. Without changing the investment strategy, the impact of the risk transfer may be larger than expected due to an unexpected drop in asset levels.

For annuity purchases, the selected liability would usually be hedged with duration-matched LDI, while lump sums are best hedged with cash, once the payment amount can be estimated.

Blindly choosing the cheapest insurer bid

Price will (and should) be an important factor in choosing an annuity provider, but annuity contracts aren’t a homogenous commodity. Understanding and valuing the financial strength and proven reputation of the provider is important too. Consider if the insurer would be providing the safest annuity available under DOL 95-1, where it also states that plan fiduciaries are responsible for “conduct[ing] an objective, thorough and analytical search” when selecting an annuity provider. This search needs to include analysis of the insurer’s investment portfolio, among other aspects, which an independent expert can assist in evaluating.2

Sponsors ought to also be comfortable with the anticipated experience participants will have with the insurer, who will be solely responsible for administering benefits to the sponsor’s former employees.

Recognize the natural attrition of the plan

While risk transfer can accelerate the removal of plan participants, it is important to recognize that a closed and frozen pension plan is going to naturally get smaller on its own over time. In fact, our asset/liability projections routinely show that frozen plans can reduce in size by 30-40% over just a 10-year time period.

If sponsors allow the plan to run its normal course, they preserve assets in the plan and avoid paying for risk transfer above the associated liability. Given current funding relief, the risk of contribution surprises is lower, making the long-term management of a pension plan more tenable for the sponsor.

Final thoughts

Risk transfer transactions can help decrease future costs to the plan sponsor and reduce the footprint of the plan on the organization. Many sponsors have successfully pursued these strategies while others have been left worse off because of them. Given risk transfer is here to stay, sponsors should be aware of which risk transfer opportunities may be attractive, and which strategies to avoid as they work toward their DB plan endgames.

1 Source: LIMRA Secure Retirement Institute

2 See Department of Labor Interpretive Bulletin 95-1