Bridging generational investing goals, circumstances and preferences

There is a significant body of research on the key generational differences in spending, saving and investing. While there is some disparity around which birth years define each generation, as a financial advisor, you are likely anecdotally aware that each generation—the Baby Boom generation (1946-1964), Generation X (1965-1980), and Generation Y (a.k.a. millennials [1981-1997])—may have distinct outlooks, financial goals, circumstances, preferences and tendencies when it comes to their finances. That’s natural, as each generation has been influenced by different economic events that have shaped their financial attitudes and beliefs.1

But how does this, or should this, impact your investment philosophy, client service model and your investment inventory?

Here are some of the investing trends across generations, including similarities and differences, as well as potential opportunities for financial advisors.

Generational similarities

A 2017 survey of investors of all ages by BMO Wealth Management found the majority of those surveyed choose to work with the assistance of a financial professional, with 28% using an advisor at a financial institution, 23% investing through an independent advisor and 18% investing with a full-service financial professional.

A separate 2017 study by Stash Financial, Inc., found that saving for retirement was the top investment goal among baby boomers, Gen Xers, and millennials. But why this is a high priority differs depending on the group.

- Baby boomers: In this group, many have entered retirement or will be doing so soon. They recognize the shorter time horizon they have for accumulating assets.

- Gen Xers and millennials: The younger generations have been inundated with information on the importance of self-funding retirement due to the phasing out of defined benefit pension plans, the increasing adoption of defined contribution plans and a general skepticism about the sustainability of government-sponsored retirement support (e.g., Social Security or the Canada Pension Plan).

Some generational divides

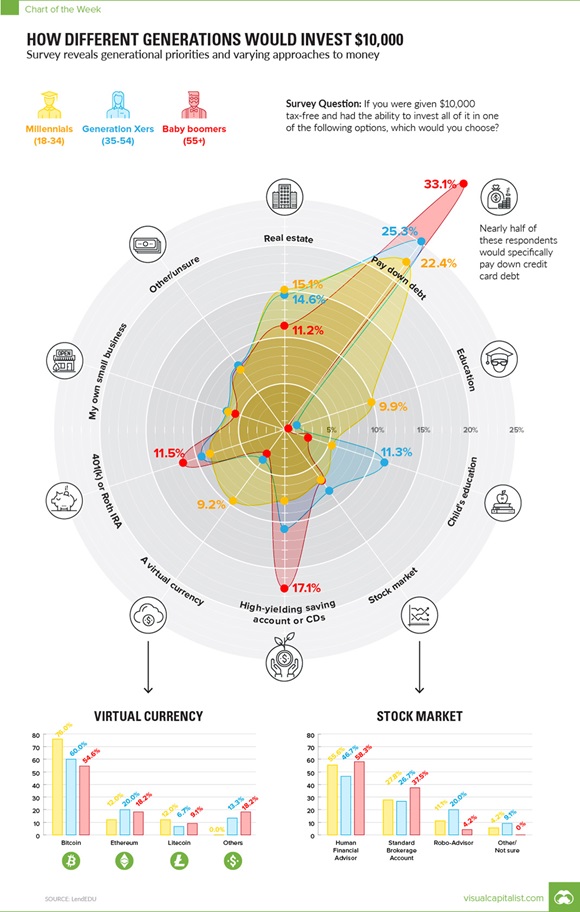

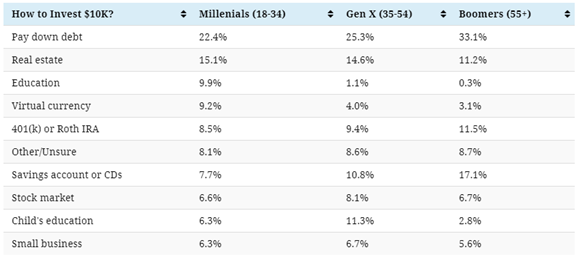

Visual Capitalist developed the below chart from a 2018 survey by LendEDU, which asked 1,000 Americans in March 2018:2, 3

Question: If you were given $10,000 tax-free and had the ability to invest all of it in one of the following options, which would you choose?

Source: Used with permission from Visual Capitalist: https://www.visualcapitalist.com/chart-different-generations-invest-10000/

Here are the responses by generation:

This survey made it clear that while debt is a burden for each generation, in fact, a higher percentage of baby boomers (33.05%) wanted to use the $10,000 to pay down debt than millennials (22.43%). However, the forms of debt for each generation varies. Each generation prioritized reducing credit card debt, especially baby boomers, whereas many millennials wanted to reduce their student loan debt first.

Another important difference in the generations is in their attitudes toward risk. In its 2017 Global Investment Survey, Legg Mason revealed the following about attitudes toward risk:

- Millennials: This group categorized its overall risk tolerance for long-term investing (defined as 10 years or more) as “very conservative” more frequently than Gen Xers or baby boomers did.

- Gen Xers: These individuals were more likely to categorize their overall risk tolerance for long-term investing as “somewhat conservative.”

- Baby boomers: Boomers were the most likely to identify with a “somewhat aggressive” overall risk tolerance for long-term investing.

These risk appetites are disturbingly misaligned with the generational time horizons and needed outcomes. For example, millennials can’t really afford to be “very conservative” if they want to reach their long-term goals. And baby boomers may need to tone down some of their aggressiveness given the time required to recover from a market event. As an advisor, you have evolved into the necessary role of behavioral coach: helping clients balance the amount of risk they WANT to take with the amount of risk they NEED to take (or NOT take, as the case may be).

For example

The 2017 BMO Wealth Management survey noted that one of the main reasons people are not saving or investing was that the process was too complicated. Almost one in five millennials (18%) cited this reason, more than double the frequency among baby boomers (at just 8%). Some of the reasons why millennials find investing too complicated include a lack of understanding of investment terminology, not understanding markets and not knowing about available investment options.

Several studies also found that although paying off debt and funding retirement are core priorities for every generation, integrated holistic wealth planning can help balance retirement planning with shorter-term goals, like buying a home or car or paying off student debt.

What might this mean for advisors?

One thing is clear: one investment model—and even one client service model—is not going to fit everybody’s needs. Delivering a customized client-centered wealth management experience takes time and capacity. It has never been more important for advisors to understand the value of their time—and how they can reach each client demographic by addressing their primary concerns—and appropriate risks.

Many baby boomers, Gen Xers, millennials, women and clients from varying cultures need help with overcoming their biases, retirement planning, investment education and asset allocation. If an advisory practice is going to be attractive to multiple generations and demographic groups, then deepening the advisory discovery protocol to better understand each individual is imperative.

There are different matters of urgency for different generations. For example, baby boomers may be looking for someone to provide order and structure around life events like business succession, inter-generational wealth transfer and planning for incapacity. Gen X’ers and illennials may be hoping you can act more like a behavioral coach to help them triage, prioritize and balance paying off debt while saving for longer term goals like educating children and saving for retirement.

Then, most importantly, implementing scalable investment models that reflect the client’s goals, circumstances and preferences is likely to lead to more satisfying outcomes for advisors and investors alike. Advisors will find they have created capacity in their day and in their business; clients will feel heard and understood. All generations are likely to sign up for a more personalized, emotionally connected advisory experience.

2Source: https://www.visualcapitalist.com/chart-different-generations-invest-10000/

3 Ibid.