Quarterly Trading Report – Q4 2023: Rally time

Executive summary:

- A renewed sense of optimism emerged during the fourth quarter, sparking an increase in U.S. equity trading volumes and a rally in risk-on fixed income assets

- S&P 500 Index options set a new single day volume record during the quarter, while U.S. Treasury futures and options and quarterly equity index options set a quarterly average daily trading volume record.

- As expected, trading volumes slipped and liquidity declined in December due to the year-end holidays—but have since rebounded in 2024.

The final quarter of 2023 may have started off on shaky ground, but there’s no question it ultimately found its footing.

Uncertainty over the end of monetary tightening and a potential U.S. government shutdown at the beginning of the fourth quarter waned as the quarter progressed, sparking a market rally and a renewed sense of optimism among the four major asset classes we trade: equity, fixed income, foreign exchange (FX) and derivatives.

As the quarter hit its stride, we saw a notable increase in U.S. equity trading volumes, a decrease in European intraday equity volatility and a rally in risk-on fixed income assets. Meanwhile, liquidity conditions improved in currency and derivatives saw record volumes. Predictably, trading volumes and liquidity declined with the approach of the year-end holidays in December—but have since rebounded to start the new year.

At Russell Investments, our experience executing trades for a broad range of clients gives us unique access into the latest market trends and insights. We trade approximately $2.3 trillion on an annual basis through our multi-venue trading platform, and maintain a 24-hour global trading desk with access to over 100 countries across all asset classes. Here are key observations from the fourth quarter of 2023, in addition to our insights into what may lie ahead for 2024.

EQUITIES

Global

During the fourth quarter, we witnessed a continuing trend of increased equity trading volumes during the last 15 minutes of the trading day, primarily based on closing auction volumes. This consistent trend was driven by increased passive index flows.

As the end-of-year approached—especially during the last two weeks of 2023—market volumes dropped and order sizes also decreased as many market participants took time off. Notably, these trends were more prevalent in North America and Europe.

U.S.

Looking back at 2023 overall, the average daily volume was $515 billion and 11.0 billion shares, which was lower by -10.1% and -7.6% versus 2022.

The S&P bounced back from its worst year in over a decade and finished 2023 with a gain of 24%. Meanwhile, the Nasdaq 100 Index logged an eye-catching 44% return, driven by the Magnificent Seven mega cap tech stocks: Apple, Amazon, Alphabet, Nvidia, Meta Platforms, Microsoft and Tesla.

Looking ahead, in May 2024, the United States, Canada and Mexico will move to a shortened settlement cycle for security transactions. Starting in May, transactions in those markets will settle on a T+1 basis. The impacts of this change will be felt well beyond those markets, given the size of the global investor base in U.S. securities.

In addition to this, both the UK and European Union are reviewing their settlement cycles with a goal of aligning with the United States. This is a complex task based on the number of markets in Europe and the upcoming global settlement misalignment on a global basis.

Click image to enlarge

Asia

During 2023, within Asia, flows clearly rotated toward Japan ($29 billion), India ($22 billion) and Korea ($9 billion). Northbound Stock Connect flows of approximately $6 billion were the lowest annual flows since 2016.

In 2023, Japan’s Nikkei 225 Index closed the year up +28% in local currency, with the annual trading value for the Japan prime market (domestic common stocks) hitting an all-time high of JPY 943.7637 trillion. Notable observations include the continued increase of closing auction volumes driven by passive indexes. Market structure changes included reduced bid/ask spreads and an announcement that the Tokyo Stock Exchange will extend its trading day by 30 minutes starting in November 2024.

In India, the NIFTY 50 Index closed the year up +21%—its eighth straight year in positive territory. The Index has only ended the year negative once in the past 12 years.

The strong positive returns in Japan, India, Taiwan and Korea were offset by continued weakness and rotation from China/Hong Kong. For the first time in over two decades, China’s market ended lower for the third consecutive year.

Europe

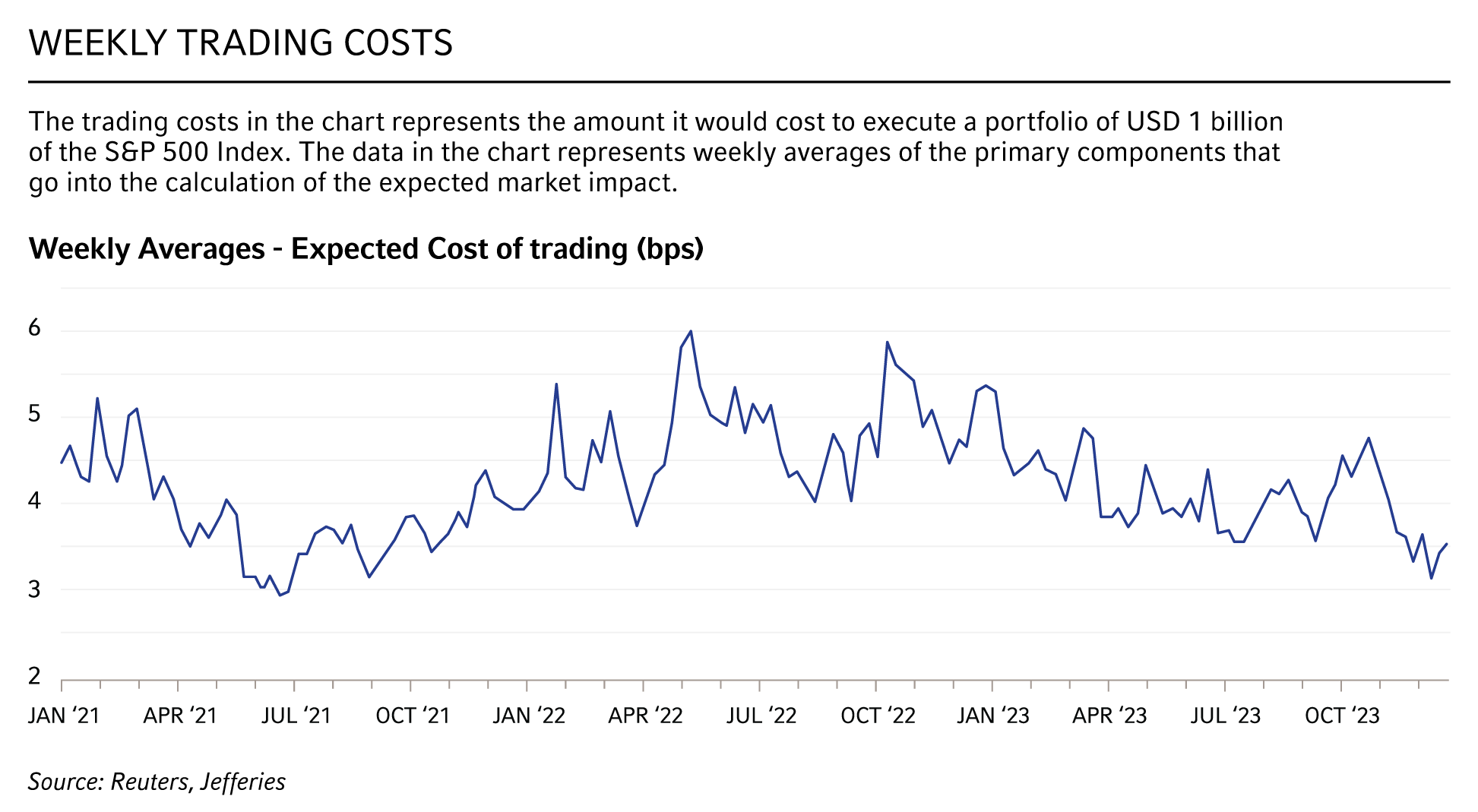

During 2023, Europe saw a lower cost of trading on reduced intraday volatility when compared to 2022. This was despite the third and fourth quarters seeing lower market volume. The lower volumes in the third and fourth quarters did raise the cost of trading to 15 basis points (bps) versus the 13 bps seen in the first and second quarters of 2023.

2023 average daily traded value (ADTV) was at ~€63.5 billion, 10.4% lower than in 2022.

European average daily trading volume rose to~€61.5 billion in December 2023, up 1.2% month-over-month (~€0.7 billion) vs. November 2023 and 6.7% higher than December 2022. The increase was driven by the quarterly rebalance on Dec. 15 with~€122 billion—the third-highest average daily trading volume in 2023. December 2023 was also the highest average daily volume month in the second half of 2023.

FIXED INCOME

The U.S. Federal Reserve (Fed)’s pause in rate increases in late September 2023 created an intriguing fourth quarter for markets. Risk-on assets began to catch traction and rallied through the new year. Credit spreads rallied by 20-35 bps over the quarter for investment grade assets, led by financials and materials. Fixed income volumes were lower by 10-15% compared to previous quarters, mainly due to holiday schedules. This was not unusual, as December traditionally sees volumes that are 25-30% less than other calendar months. Starting in November, dealer inventories also reduced dramatically in the fourth quarter, ending up down 36% as traders closed out positions for the new year. This contributed to the strong rally with little paper available in the street.

Additionally, we saw a strong rally in U.S. Treasuries after the market tested 5% on the benchmark 10-year note in early October. Much of the rally can probably be attributed to inflation outlook changes, with the Fed forecasting consumer price gains to continue easing into 2024. Rates bottomed out at 3.8% on the 10-year note in late December and have since rebounded to just over 4%. Many analysts now anticipating a soft landing—where economic growth slows but a recession is avoided—with rates continuing lower into 2024. The large debate at this point is when the Fed will begin rate cuts, and how the U.S. elections will drive markets into November.

Click image to enlarge

Source: New York Fed

FOREIGN EXCHANGE

At the start of the fourth quarter in October, foreign exchange market liquidity remained relatively stable compared to September, despite the potential for another government shutdown. Likely due to numerous scares in earlier 2023 with similar events, the currency markets seemed more numb, with volatility remaining muted. Interbank average daily volumes (ADV) increased by a modest 0.5% in October 2023, which was in line with a slight uptick in volatility at +0.4%. Top-of-book spreads narrowed across G10 (Group of 10) spot, emerging markets (EM) spot and 1-M Asian non-deliverable forward (NDF) by an average of 1.5%. While average daily volume (ADV) in G10 spot increased (+4.6%), EM spot dipped for the second consecutive month. ADV for EM spot was down by 9.2%, despite top-of-book spreads tightening (+1.1%) and volatility dropping (+0.7%).

November experienced a modest market-wide improvement in liquidity conditions, as global equity markets saw a steady support heading into a year-end rally. Average daily volume increased by 1.6% month-over-month, while top-of-book spreads compressed by 1.6% on average and volatility held steady. G10 spot ADV dropped by 4.1% despite top-of-book spreads and volatility holding relatively steady (-0.5% and +0.5% respectively). EM spot ADV increased by 7.3%, buoyed by improved trading conditions: top-of-book spreads tightened by 7.8% and volatility decreased by 1.8%

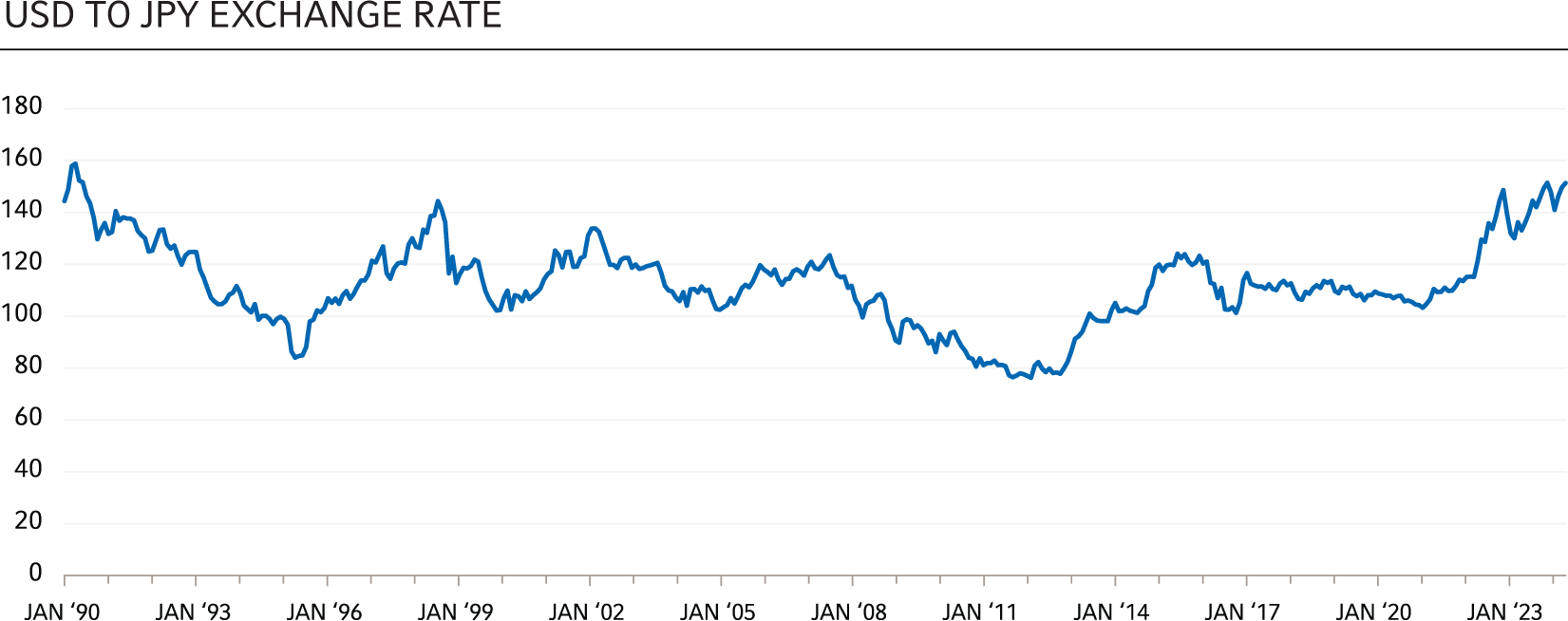

Unsurprisingly, liquidity conditions in December were vastly impacted by seasonal factors and the holidays. ADV was down 5.8% month-over-month, top-of-book spreads widened by 64.8% and volatility increased by 13.7%. G10 spot registered a slight uptick in ADV of 1.3% despite top-of-book spreads widening by 66.3% and volatility increasing by 13.6%. USD/JPY volumes were up 15% month-over-month on the increased possibility of a Bank of Japan (BoJ) December rate hike. EM spot ADV decreased by 15.8% while top-of-book spreads widened by 43.6% and volatility increased by 2.9%.

DERIVATIVES TRADING

Just hours before the start of the fourth quarter of 2023, the government narrowly avoided a shutdown by passing a funding bill late on the evening of Sept. 30. However, it was only a 45-day extension, and on Nov. 15 Congress—again and temporarily—averted a shutdown. Amid this backdrop the S&P 500 Index roared higher, posting a +11.2% gain.

As the last Fed interest rate move was in July, speculation of rate moves at the FOMC meetings on Nov. 1 and Dec. 13 came into focus. If uncertainty was the theme during the fourth quarter of 2023, it was certainly reinforced by the types of derivatives that witnessed record volumes. According to CBOE, S&P 500 Index options set a new single day volume record on Dec. 14. Similarly, at CME Group, U.S. Treasury futures and options and quarterly equity index options set a quarterly average daily trading volume record.

The fourth quarter trends were also indicative of patterns and growth of year-over-year activity. Whether hedging or expressing a view, derivatives can adequately deliver. Russell Investments’ listed derivatives gross notional trading volume for clients and funds increased +4.34% year-over-year.

Reflecting upon 2023, a popular topic was the proliferation of products in the short-dated options space (also referred to as 0DTE for zero days to expiration). These products are gaining in popularity. Short-dated options strategies can be used to manage event risk and sell premium as well achieve a variety of other objectives. While the market has been able to absorb and support these products ably, it is important to monitor the behavior of these products as market participants are expressing tactical views with their evolving liquidity.

The bottom line

As the new year unfolds, it’s unclear whether the investor optimism that emerged in the final months of 2023 will continue, or if a revival of recession fears and uncertainty over the U.S. elections will inject renewed volatility into markets. In either case, at Russell Investments, our 87-plus years of experience in trading makes us well equipped to manage risk and move money expeditiously for our clients, regardless of the market environment. We combat low volume with significant market depth through 400+ dealers to assist our clients with improved performance and minimal impact.

At Russell Investments, we’re committed to delivering scalable solutions that meet the trading and execution needs of asset owners and asset managers alike. We’re also dedicated to sharing our insights and observations from our global trading desk every quarter. Please reach out if you have any questions.