A sharper focus on the value of advisers.

How can financial advisers reassess their value? Read our 2021 Value of an Adviser Study to learn more.

Read the full study

How can financial advisers reassess their value? Read our 2021 Value of an Adviser Study to learn more.

Read the full studyWe believe advisers provide real value to their clients. Much of the work of an adviser is complex and happens behind the scenes, though, making it hard for clients to appreciate. Our Value of an Adviser programme is designed to help advisers and investors articulate and understand the full value of an adviser’s services.

Without regular rebalancing, a client’s portfolio could become overly heavy in large capitalisation U.S. equities.

Over longer periods of time, this sort of shift can meaningfully change the risk and return potential of a portfolio. For example, if an investor had purchased a hypothetical balanced portfolio of 60% equities and 40% fixed income in January 2009 and it had not been actively rebalanced since then, by the end of 2020, the risk profile of the portfolio would look very different. That original balanced portfolio would have become a growth portfolio, with 80% invested in equities and only 20% in fixed income. That would expose the investor to risk they didn’t agree to and could be a concern if equity markets suddenly reversed, as we saw in early 2020.

When balanced becomes the new growth

The potential result of an un-balanced portfolio

Source: Hypothetical analysis provided in the chart & table above is for illustrative purposes only. Not intended to represent any actual investment. Source for both chart & table: U.S. Large Cap Growth: Russell 1000 Growth Index, U.S. Large Cap Value: Russell 1000 Value Index, U.S. Small Cap: Russell 2000® Index, International Developed Equities: MSCI World ex USA Index, Emerging Markets Equity: MSCI Emerging Markets Index; Global Real Estate: FTSE EPRA NAREIT Developed Index, and Fixed Income: Bloomberg U.S. Aggregate Bond Index.

Featured insights from our experts:

There is no question that 2020 was a wild ride. Many investors were tempted to flee for the exit in mid-March when the FTSE All-Share Index registered its largest weekly decline since 2008. In fact, between 17 January 2020 when the index closed at a record high, and 23 March 2020 the FTSE All-Share fell by 35.9%.

This is where the value from your behavioural guidance really comes into focus. Investors who remained invested would have seen the index rebound 27.8% in the subsequent three months.

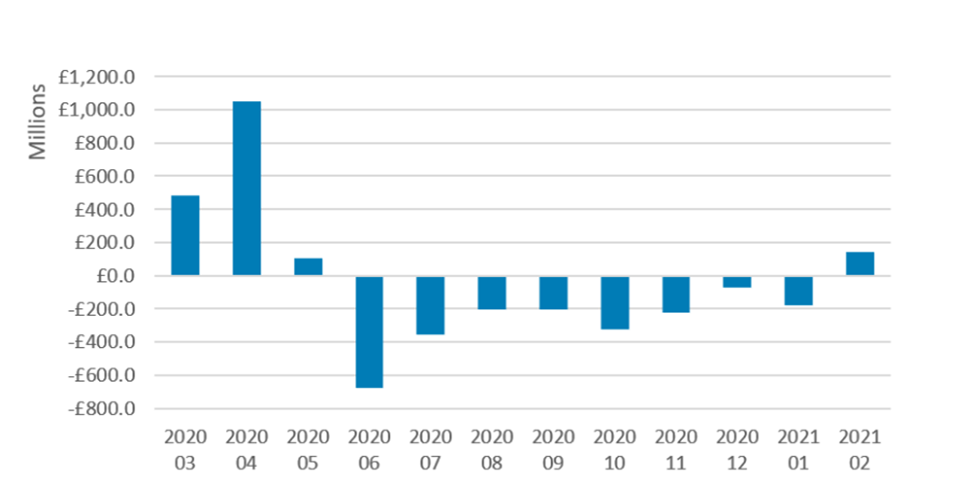

Without an adviser’s guidance, many investors could have sold following the coronavirus induced market sell off in March 2020. In fact, investors redeemed a total of £2.2bn from UK equity strategies between May 2020 and January 2021 according to Calastone1. It was only until February 2021 this year where UK equities witnessed a net inflow of £145m. This means many investors have had to buy high as the markets recovered throughout the remainder of 2020. Or they would have been forced to remain in cash until a better entry point appeared - a risky and unpredictable strategy.

As the flows chart below shows, missing out on even a few days of good performance can have a detrimental effect on a portfolio. And how do you know which days those will be? That’s the catch - you don’t. Markets can be unpredictable. But their long-term trend has been up. In fact, the FTSE All-Share Index has finished the year in positive territory 68% of the time since 19622.

UK equities fund - net inflow/outflow

1Source: Calastone Fund Flow Index.

2 Source: Envestnet. https://www.envestnet.com/press/envestnet-moneyguides-latest-advisor-survey-finds-financial-planning-services-fees-rise

Featured insights from our experts:

If someone wanted a cookie-cutter, one-size-fits-all investing experience – at very little cost – they could use a robo-adviser. But a robo-adviser generally doesn’t provide a financial plan, ongoing service, or guidance; just the option for an investor to choose from a pre-selected list of funds, provide annual statements and a phone number to call in case of questions. This would be fine if all investors are alike.

Each investor has their own set of goals, circumstances, and preferences. And that is why we believe the customised client experience that an adviser can offer has significant value. At one time, an adviser was essentially a broker – selecting investments for clients. Now, most advisers are expected to provide holistic wealth advice for entire families. Indeed, between 2017 and the end of 2020, there has been a 39% increase in advisers providing comprehensive planning services3.

We have found that the value that advisers deliver through the customised experience is much higher than the cost of an automated service and cookie-cutter plan from a robo-adviser.

Featured insights from our experts:

If every investor has their own goals, circumstances and preferences, then it stands to reason that each will require a different mix of products. But how can you provide that customised client experience when there is only an average of 1700 work hours in a year? That’s based on 35 hours a week over 47 weeks. And that’s not accounting for illnesses, additional holiday, conferences, meetings and other events that can take a bite out of the time you have available. Impossible, right?

Besides, we’ve already discovered that investors value advisers for their personalised service and want more frequent communication. So, it makes sense for you to provide the wealth management services and outsource the investment management. This is where the use of models can really help you free up time while still ensuring each of your clients gets the customised client experience they value.

The time you would have spent researching funds, meeting portfolio managers and analysts, tracking those funds, and conducting ongoing research is now available for you to spend time with your top clients - giving them the personalised experience they crave.

And with that personalised service, you will gain deeper insight into your clients’ goals, circumstances and preferences - making it more likely that the model strategies you choose will more closely align with the outcomes they desire.

Let’s say you outsource investment management to a firm that provides a selection of model strategies or multi asset solutions. A recent study4 has found that by doing so, a financial adviser could save 7.7 hours a week. Multiply that by the number of weeks worked in a year and you end up with an extra 360 hours – time you could spend with your family, or growing your business, or with your top clients.

Now imagine having an additional 7.7 hours to work with your top clients on their specific needs and deepening the relationship they have with you. How would that impact your business? The value to you is significant, but so is the value to them. If we estimate an adviser’s average hourly rate is £60 (based on annual revenue of £100,000 a year and a 35-hour work week), then the value of that additional time for each of your top 50 clients is £460.00. Based on a £300,000 account, that’s an additional 0.15% of value you can offer them just by outsourcing.

Hypothetical scenario for illustrative purposes only.

4Source:https://static.twentyoverten.com/5e0f642709752828dbb0c6e0/-mjyNOiwG/Outsourcing-Money-Management-article4.pdf, AssetMark, 2019. Accessed on Feb 3, 2021

Featured insights from our experts:

This post-pandemic world could be the perfect time for advisers to reassess the full value they deliver and how they communicate that value to their clients.

We know that many advisers worked hard through 2020’s challenges to keep in touch with clients and keep them invested. Our formula shows that even if advisers were only able to help their clients avoid the behavioural mistakes that many investors make in the face of the significant volatility we saw, advisers have already provided value above and beyond their fee. Add to that their other services, the active rebalancing, customised client experience advisers give clients and ensuring their portfolios align with their specific goals, and it seems clear that the value advisers deliver is significant.

Continuing education credit opportunity

Earn continuing education credit while learning about our Value of an Adviser series.

For questions, contact Hani:

Hani

Kabbabe

/ ASSOCIATE DIRECTOR MIDDLE EAST