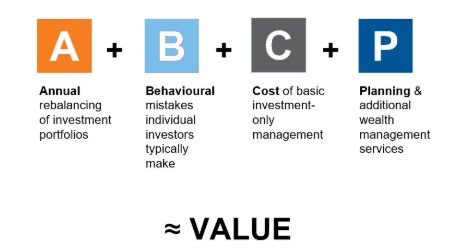

P is for planning. See why it's so valuable to investors.

This is the final post in the four-part series, discussing why Russell Investments believes in the value of advisers, based on this simple formula:

In this section, we’re talking about P, which stands for planning costs and ancillary services.

Planning has become table stakes in our industry, but I say that with a note of caution. When a financial plan feels like a box-checking exercise, it can be seen as a commodity. We believe that when a planning process is positioned to a client, it should be intentional and it is crucial to position the process as the bespoke service it is, rather than a box ticking exercise, to ensure clients understand the value. After all, as you know, planning, is not a one-time step. It’s an ongoing process that keeps investors on track.

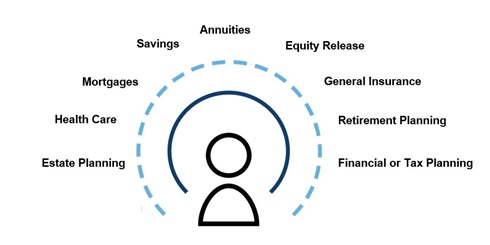

What’s in the plan?

The items in the chart below represent the areas that are covered in a comprehensive plan from a high-quality adviser. We believe that due to the more complex circumstances that clients are faced with, as well as the extreme levels of volatility in the market, creating a more comprehensive plan is integral. As per an article in the Financial Times, a standard retirement plan, transferring a £100,000 pension with guaranteed annuity rates, will cost approximately £2,000 in fees.

Planning is important to clients. However, the importance of planning is sometimes overlooked by the ongoing compliance and obligatory requirements.

A comprehensive plan not only enables the adviser to analyse the financial needs of the client but it is also used as a monitoring tool to establish the progress and demonstrate the value added. The plan is particularly crucial during times of uncertainty, planning for hurdles is just as important as planning to reach desired end goals.

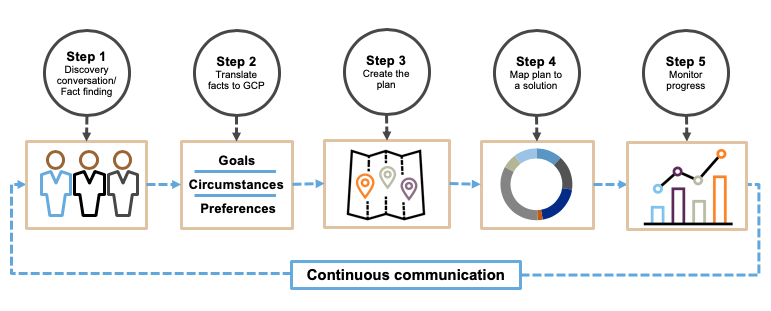

The planning cycle in five steps

Click image to enlarge

- Delivering wealth management begins with a deep client discovery conversation. This should be a conversation led by open-ended questions, the adviser will be listening and understanding the personal needs of the client. In some instances, for existing clients, this means going back and having a rediscovery conversation. Take the time to reflect with your clients by re-igniting a fact-finding process to ensure that all the activities and solutions are still driving toward the right outcomes.

- The next step is to translate that discovery conversation into goals, circumstances and preferences.

- Goals are the fundamental problem involving money and time that clients are trying to solve. The importance of goals must be defined by the client. It is then the adviser’s role to convert the stated goals into accumulation and spending milestones.

- Circumstances are the unavoidable facts that define a client’s situation. Under the heading of circumstances, we might include a clients’ investment-account balances, along with their stage of financial life; marital status and ability to save more or spend less.

- Preferences are more flexible. These are the aspects which clients desire in their investment solution, rather than need. Advisers have often simplified preferences down to a risk profile, to evaluate the risk level an investor is comfortable with. Furthermore, clients care about their portfolio drawdown potential, cash flow consistency, and illiquidity. These days, more and more investors also approach investing from a values point of view, with preferences on portfolio holdings such as; carbon, tobacco, munitions and other socially responsible issues. Advisers should prioritise meeting goals – whilst aligning the goals with preferences.

- The third step is to create the plan. In order to do so, we believe you must know the location of the client’s money. This includes transparency into insurance, wills, trusts, mortgages, etc. We believe this holistic and transparent approach is in the best interest of investors. Without it, the plan could be operating at cross purposes, with other hidden aspects of your investor’s financial picture. We’ve seen this happen many times over the years. It pays to get the complete picture so that you can build the right plan from the start.

- Step four requires you to map the plan to a solution. Many advisers use model portfolios for the majority of their investors, when appropriate to do so. They often use the same model portfolios as a core to build customised solutions for their suitable top clients, households and families.

- Finally, the framework should be wrapped in a process to monitor progress, with ongoing communication between the adviser and investor, as goals, circumstances and preferences evolve over time. As I said earlier, planning is an ongoing process, not a one-time thing.

The value of listening

The most brilliant conversationalists are great listeners, especially in the current day and age of media talking at us - being truly heard is a rarity. Listening is the quiet key to human connection and leads to deeper relationships with your clients.

We believe that despite the client’s communication, both verbal and non-verbal, advisers provide the valued, but sometimes underestimated skill, of listening. The ability to listen and understand a client’s financial needs is integral, it provides an opportunity for further planning and the articulation of ever-changing personal circumstances.

The bottom line

Advisers understand that having a robust plan might feel reassuring, but it’s only as good as the implementation. A plan is out of date as soon as it is finalised, due to continuous circumstantial changes. The value comes from an adviser who can adjust the plan to align with the client’s ongoing needs.

The value of planning should not be taken for granted, nor should it be given away during the prospecting phase.

In order to further support advisers with continual communication to clients, we have an array of materials and tools available, as well as a dedicated value of an adviser webpage.