Market

Outlook

Market

Outlook

THE MECHAZILLA MOMENT

Successfully navigating markets in 2025 will demand more than relying on conventional wisdom about U.S. outperformance and global headwinds.

2025 Global Market Outlook – Annual update

An enduring image from 2024 will be the capture of the SpaceX booster rocket by the mechazilla robot arms on its return to Earth. This amazing achievement symbolizes a year where the improbable became possible, redefining expectations. Similarly, the U.S. economy has remained resilient despite aggressive Federal Reserve policies. Heading into 2025, we expect steady growth and a soft landing for the economy.

Three key macro watch points we think are important for the year ahead:

First, U.S. growth and policy shifts. We expect U.S. growth around 2% in 2025 as inflation cools and the Federal Reserve likely eases interest rates. Growth will be influenced by factors like trade policies, immigration reforms, tax cuts, and the outcome of the 2024 U.S. election. With Republicans gaining more control, tax cuts and deregulation could stimulate growth, while trade tensions or restricted policies may introduce more volatility.

Second, global economic divergence. Europe faces stagnation, Japan shows promise with controlled inflation, and China struggles with a cooling property market and trade restrictions. These regional shifts will impact global markets, requiring close monitoring.

Third, market sentiment and valuations. Equity valuations remain high, but the strong U.S. dollar adds complexity. We think volatility presents opportunities, particularly in sectors like artificial intelligence. Industries such as healthcare and industrials continue to benefit from technological advancements, offering significant growth potential.

So, what do these macro trends mean for portfolios in 2025? With shifting policies, global economic conditions, and evolving markets, we think careful portfolio construction is crucial. Here are three key considerations:

First, balancing U.S. growth amid policy shifts. The U.S. economy is resilient, but the future path depends on evolving policies. Tax cuts and deregulation could benefit small-cap stocks, creating opportunities for growth. However, uncertainty and geopolitical risk will require active management to navigate this volatility.

Second, private markets as a growth engine. Private markets, especially in infrastructure, private credit, and AI-driven startups, offer strong growth potential we think AI now makes up 27% of all venture capital deals signaling significant momentum in the market as interest rates stabilize private markets in Europe Japan and the Gulf States are poised for strong returns particularly in sectors like energy digital utilities and AI sectors.

Third, broadening market leadership. The dominance of mega-cap tech stocks is shifting as smaller, agile companies, particularly in AI, take the lead. This broadening out of market leadership reduces concentration risk and really starts to open up opportunities for alpha generation. Real estate and infrastructure investments are becoming more attractive, providing growth, income stability, and inflation protection.

2025 will be a year of navigating both uncertainty and opportunity. By balancing growth and risk management, we can stay ahead in a rapidly evolving market. We’ll continue to provide deep insights into these macro watch points and their implications for investment portfolios.

Andrew Pease

Chief Investment Strategist

“On balance, we see the policy mix of the new U.S. administration as supportive for business confidence, which is likely to drive a resurgence in capital markets and provide positive tailwinds for private assets.”

- Andrew Pease, Chief Investment Strategist

2025 Global Market Outlook:

The Mechazilla Moment

An enduring image from 2024 will be the capture of the SpaceX booster rocket by the Mechazilla robot arms on its return to Earth. This achievement served as a powerful metaphor for the year: the improbable not only became possible but redefined expectations.

Despite the tightest U.S. Federal Reserve (Fed) policy since the early 2000s and a deeply inverted Treasury yield curve, the U.S. economy defied expectations with above-trend GDP growth, robust job creation, a 25% surge in the S&P 500 Index, and double-digit earnings growth.

2025 will be another year of overcoming challenges and redefining limits against a backdrop of high U.S. equity market valuations, mega-cap dominance, and the uncertainty surrounding the policy agenda of U.S. President-elect Donald Trump.Key Economic Views

Looking into 2025, we anticipate a soft landing for the U.S. economy. Our assumption is that the new administration will ease its more aggressive stances on tariffs and immigration. With these dynamics in mind, here are our key economic views for 2025:

-

U.S. Growth and Policy Trade-offs

The U.S. economy is expected to grow at a trend-like pace of 2.0% in 2025 in response to the lagged impact of tight Fed monetary policy. Core personal consumption expenditures (PCE) inflation is projected to move closer to the Fed’s 2% target, while the central bank eases rates gradually, with the fed funds rate likely to reach 3.25% by year-end—aligning with its neutral level.

The Trump administration’s policies present a delicate balancing act. Tax reforms and deregulation are likely to stimulate growth, particularly in domestic and cyclical sectors. Tariffs and immigration restrictions, however, could trigger a stagflationary shock that might have the Fed contemplating a rate hike as the economy weakens.

Our working assumption is that the new administration will not aggressively pursue policies that create inflation risk. One clear message from the election is that U.S. voters were unhappy with the inflation of the Biden years. Tariffs and immigration controls are likely to be implemented, but their extent will be constrained by the inflation outlook. On balance, we see the policy mix as supportive for business confidence, which is likely to drive a resurgence in capital markets and provide positive tailwinds for private assets.

-

Global Headwinds and Policy Divergences

Outside the U.S., growth will likely remain under pressure. Trade policy uncertainty and tariffs will weigh heavily on Europe. The European Central Bank (ECB) is likely to cut its deposit rate to 1.5% by year-end to offset the tariff impact and the continued stagnation of the German economy.

The UK faces sluggish productivity growth, labour constraints, and inflationary impacts from higher taxes under the new Labour government. The Bank of England’s (BoE) capacity to ease is constrained, with the base rate likely to decline only modestly to 3.75%–4.0%.

Japan remains an outlier, supported by a virtuous wage-price spiral that will anchor inflation expectations near 2%, allowing the Bank of Japan (BoJ) to further normalisze policy. Rates could rise to a 30-year high of 0.75% by year-end.

China faces headwinds from the property market collapse, deflation pressures, and U.S. tariffs. The policy response continues to be reactionary, rather than one where proactive steps are taken to solve structural problems such as high savings and low household consumption. There are downside risks to consensus expectations for 4.5% GDP (gross domestic product) growth in 2025.

-

Market Sentiment and Valuations

Three defining features of the market outlook for 2025 are the elevated level of the S&P 500 forward P/E (price-to-earnings) ratio at 22x, the potential for further U.S. dollar strength, and the direction of the U.S. 10-year Treasury yield.

Elevated equity valuations make the U.S. market vulnerable to negative surprises, and further dollar strength will challenge emerging markets. Sustained U.S. Treasury yields above 4.5% could challenge equities, diminishing the earnings yield advantage stocks have enjoyed over bonds since 2002.

Key Portfolio Themes

Portfolio Considerations for 2025

As we navigate 2025, the interplay between the shifting policy landscapes and evolving market conditions calls for thoughtful portfolio construction. Building on the macroeconomic backdrop—defined by resilience in U.S. growth, potential disruptions from trade and immigration policies, emerging opportunities in AI (artificial intelligence)-driven productivity and growth in private markets—three strategic themes guide our approach:

Balancing U.S. Growth Amid Policy Shifts

The U.S. economy is resilient as it enters 2025, but the road ahead will be shaped by shifting policy dynamics. On the positive side, tax cuts and deregulation could provide a meaningful growth boost, particularly to domestic and cyclical sectors. Given lower valuations and improving sentiment, we are more positive on U.S. small cap equity than we have been in prior years. Large cap dominance in both earnings and price appreciation will require a catalyst to shift returns in the small cap direction. Potential deregulation and lower interest rates could be such a catalyst. We believe companies leveraging AI technologies to enhance productivity—especially in industrials and healthcare—could see material improvements to operating fundamentals.

On the flip side, rising trade tensions and potential restrictions on immigration could disrupt labor markets and supply chains, creating risks to growth. This balancing act introduces greater volatility across markets, providing more opportunities for our active managers.

We also expect more opportunities in the next 12 months to tactically calibrate total portfolio risks around a robust strategic asset allocation. For example, in July 2024, we reduced equity risk as our analysis indicated that markets were stretched, and investor sentiment was overly optimistic. When markets corrected in early August amid concerns about slowing U.S. growth, sentiment shifted, creating an opportunity to add risk back into portfolios. This disciplined approach serves as a model for navigating the dynamic market environment we anticipate in 2025.

What could potential U.S. policy changes mean for your portfolio?

Asset Class Implications:

Equity: We are focused on U.S. small caps, where post-election dynamics, improving earnings, and attractive valuations may create compelling opportunities. We also see growth managers targeting high-growth cyclicals like software, while value managers identify M&A (mergers and acquisitions) potential in financials and healthcare. Core managers are balancing cyclical exposure and managing risks in rate-sensitive sectors.

In addition, we expect increased market volatility from U.S. foreign policy actions to create opportunities for active managers to find quality companies temporarily impacted by headline risks.

Fixed Income: We see a steepening yield curve offering opportunities in short-term bonds, as short-term rates are expected to decline faster than long-term yields. Credit markets may have limited upside due to tight spreads, particularly in U.S. high-yield and investment-grade bonds. This creates an opportunity to expand fixed income exposure into areas with more attractive risk/return trade-offs, such as emerging-market U.S. dollar bonds and private credit.

Currencies: The U.S. dollar is expected to face upward pressure from tariffs, the strength of the U.S. economy, and a less dovish Fed compared to other central banks. However, its valuation remains high, and emerging market currencies have already been under pressure. Given this, we are keeping currency bets in portfolios limited for 2025, while staying alert to any opportunities and risks that may arise throughout the year.

Private Markets: The New Growth Engine

Private markets continue to play an increasingly vital role in the evolving landscape of capital flows, as the shift away from public markets accelerates with fewer IPOs (initial public offerings) and later-stage listings. This transformation is particularly evident in AI opportunities, where venture capital investments now make up 27% of deals and 41% of capital raised.1 In our view investors can benefit from broadening portfolios into private markets. The upcoming policy environment may also be more favourable for private markets, with stabilising interest rates, easing regulations, and rising M&A activity. However, the influx of capital into U.S. private markets has led to sourcing challenges, which makes international opportunities more attractive. In particular, Europe offers compelling middle-market consolidation opportunities in fragmented industries, Japan benefits from ongoing corporate reforms and asset divestitures, and the Persian Gulf states are emerging as dynamic investment hubs thanks to progressive regulations and large-scale development initiatives. Infrastructure also presents a key opportunity, as hybrid investment models that incorporate both private and public markets unlock substantial growth potential.

We believe a multi-manager approach is crucial in this landscape. By diversifying across specialized managers, particularly in real assets, investors can access a broader range of opportunities that blend public and private market investments. This strategy creates more resilient portfolios and allows investments in sectors such as data centers and warehousing, where combining private and public market exposures is especially productive for a total portfolio.

“The convergence of public and private markets is set to define opportunities, particularly in sectors like real assets, where integrating exposures can create diversified, resilient portfolios.”

– Kate El-Hillow, President and Chief Investment Officer

Market Implications:

- Private Equity: We are focused on private equity opportunities in European middle-market consolidation, along with continued growth in Japan and the Persian Gulf states. Managers with sector-specific expertise are outperforming generalists, and we believe that portfolios can benefit from this trend.

- AI and Tech: We believe private market ventures in AI, particularly those focused on scaling innovative technologies across industries, will continue to be key drivers of long-term growth. We are actively looking for investments in AI-driven companies that are poised to enhance productivity and reshape industries.

- Private Credit: We see private credit as a resilient asset class, particularly in the current higher-rate environment. With asset-based lending and European direct lending providing attractive relative value, we are broadening our fixed income exposures into these areas to capture higher yields and better diversification.

- Infrastructure: We are favourable to infrastructure as a long-term growth anchor and a hedge against inflation. The asset class has proven resilient during recent market volatility and benefits from long-term trends such as the energy transition, renewable energy, and digitalization. Increasing demand for sustainable and digital infrastructure continues to drive significant capital inflows. Additionally, hybrid models combining private and public market exposure are unlocking new growth potential.

- Venture Capital: We see significant opportunities in AI-driven venture capital, particularly in early-stage companies with the potential to reshape industries. As the VC market stabilises, we are concentrating on firms with strong fundamentals, a track record of innovation, and a capacity to scale effectively.

The broadening out of Market Leadership

While mega-cap AI stocks have driven market returns in recent years, leadership is shifting to companies using AI to create real-world efficiencies. The new U.S. administration’s focus on deregulation and tariff-based policies may provide an added boost to smaller, domestically oriented companies, which are less exposed to international trade disruptions than mega caps with significant foreign revenue, such as Apple.

We see this shift reducing market concentration and opening the door for alpha opportunities. Active managers will likely play a critical role in identifying under-covered firms that are adopting AI to drive productivity and gain competitive advantages. As AI adoption accelerates, driven by falling costs, we expect companies leveraging these innovations to benefit from enhanced productivity and improved competitiveness. Additionally, with interest rates stabilising and valuations improving, real assets such as real estate and infrastructure are becoming increasingly attractive, offering growth, income stability, and inflation protection amid policy uncertainties.

Market Implications:

- Equity: Active equity managers have been challenged by the recent severe market concentration. Our research indicates that even a flattening out of these trends—which could be driven by policy shifts, or changing sentiment around earnings growth and valuations for mega caps—can be quite supportive for active manager outperformance. We and our active managers are focused on sectors where AI adoption is accelerating, such as industrials, healthcare, and consumer goods. We believe companies leveraging AI for productivity improvements are well-positioned to gain a lasting competitive edge and generate strong returns. Skilled active managers can seek out these companies, especially those in less-covered segments of the market.

- Real Assets: We see attractive investment opportunities in real estate and infrastructure, particularly in areas benefiting from stabilising long-term interest rates and favourable relative valuations compared to other growth assets. AI applications in real estate, such as data centres and healthcare facilities, are emerging as key growth areas. Additionally, infrastructure investments are gaining momentum from energy utilities and pipeline exposures, especially with the U.S. administration's focus on expanding LNG (liquified natural gas) production.

Fat tails and alternative scenarios

It’s a cliché to say that uncertainty is high, but the return of Donald Trump to the White House adds an additional layer of complexity to the 2025 outlook. Alongside the usual business cycle risks, there is the unknown of how the new administration’s policy priorities and sequencing will unfold. We don’t know how aggressively President-elect Trump will implement his campaign promises of sweeping tariffs, lower immigration, and forced deportations. An early focus on tax cuts and deregulation would likely be well-received by equity investors. However, if the first major policy moves target tariffs and immigration, investor sentiment could sour.

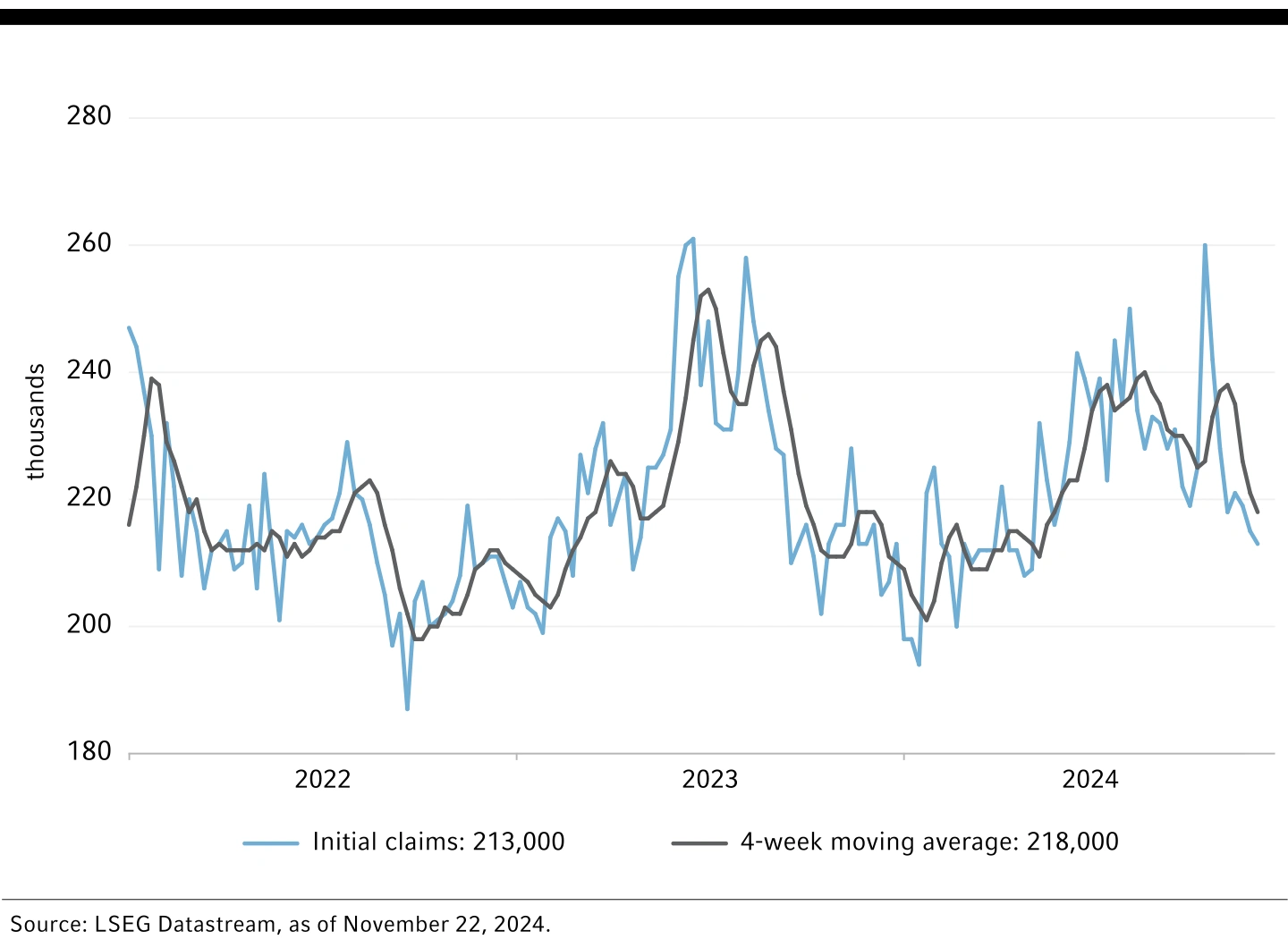

On the business cycle, we expect the U.S. economy to slow to trend-like growth as the lagged effects of Fed tightening take hold. The risk remains that the economy could tip into a mild recession, with job market weakness triggering a consumer pullback. We’re closely monitoring jobless claims—sustained claims above 260,000 per week would signal a more painful adjustment. Claims below that level would suggest the economy is resilient despite tight monetary policy.

“If U.S. initial jobless claims consistently exceed 260,000 per week, it would indicate a more severe economic adjustment. We haven’t seen that yet, and we expect the U.S. labor market to remain strong.”

- Paul Eitelman, Senior Director, Chief Investment Strategist, North America

Key indicator: U.S. weekly initial jobless claims

The other scenarios we will be monitoring are U.S. inflation risks and potential positive surprises for Europe and China.

U.S. inflation risks could arise from economic overheating fueled by tax cuts and deregulation, which may sustain stronger-than-expected demand and limit the Fed’s ability to ease policy. Additionally, tariffs and immigration controls could tighten labor markets and disrupt supply chains, driving costs higher. If these pressures keep inflation elevated, the Fed might raise rates rather than ease, pushing U.S. Treasury yields above 4.5%. This would challenge the equity market, as the S&P 500’s earnings yield of 4.5% has consistently exceeded 10-year Treasury yields since 2002. A sustained reversal of this dynamic would strain equity valuations.

Despite a pessimistic consensus on Europe and China, both regions present potential for positive surprises. Europe’s equity valuations are compelling, with forward price-to-earnings multiples at a 45% discount to the U.S. Aggressive ECB easing could revive eurozone demand, with improving bank lending—a key indicator—signaling potential outperformance.

In China, policy shifts or improved corporate governance could deliver unexpected upside. Share buybacks have begun reversing years of dilution, enabling 11% earnings-per-share (EPS) growth in the year to November 2024, despite a struggling economy. With a low forward multiple of 10 times, another year of double-digit EPS growth could drive outsized returns for the MSCI China Index.

Conclusion: Overcoming the improbable requires discipline and strategy

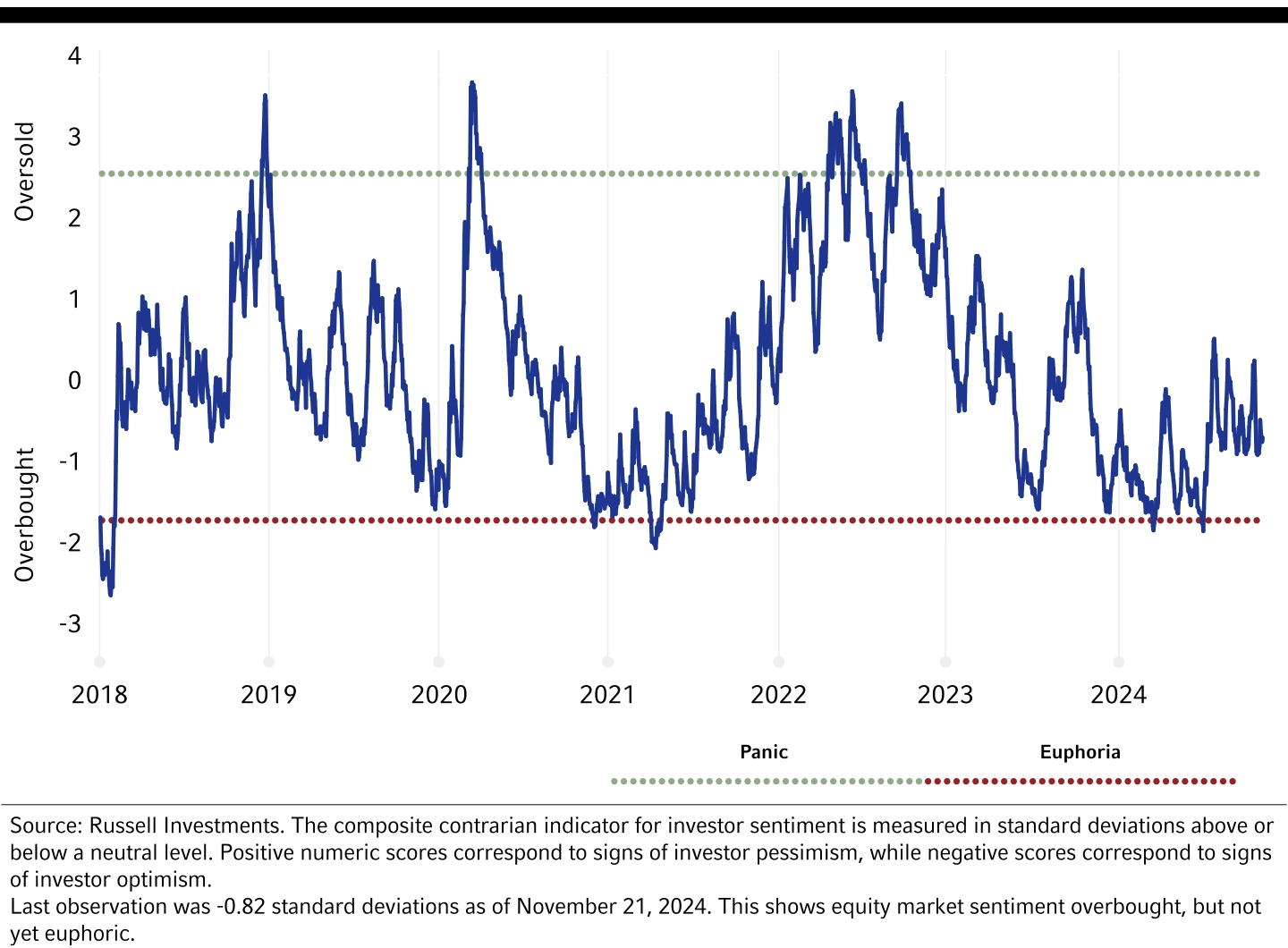

Markets in 2025 will demand more than conventional wisdom about U.S. outperformance and global headwinds. While our composite contrarian sentiment indicator signals investor optimism, it remains below critical correction thresholds. This creates a tactical opening for disciplined investors.

We believe success will require nimble allocation across public and private markets, backed by rigorous analysis and unwavering investment discipline. A projected U.S. soft landing, coupled with expected policy moderation on trade and immigration, opens specific opportunities for well-positioned portfolios.

Just as robot chopsticks can catch spacecraft in 2024, it’s plausible that markets can remain resilient through policy uncertainty in 2025. A disciplined approach to building total portfolios will be critical to investor outcomes.

Composite Contrarian Indicator

Regional snapshots

United States

U.S. exceptionalism leads into year-end, with low layoffs and improving corporate earnings supporting a soft landing. The election results introduce uncertainty around tariffs, immigration, and market-friendly policies like tax cuts and deregulation, though we expect a balanced approach. A post-election bounce in business confidence is encouraging. The Federal Reserve is likely to implement gradual rate cuts to a new normal of 3.25%, with market pricing reflecting this. Our U.S. equity strategies focus on diversification and security selection, particularly in small cap cyclicals. U.S. fixed income and multi-asset strategies have reduced interest rate sensitivity, anticipating much of the recent yield rise to be justified by the evolving policy and fundamental landscape.

Canada

The Canadian economy lagged the U.S. in 2024 but avoided a recession. Inflation has dropped, and the Bank of Canada is expected to continue rate cuts into 2025. Despite this, Canada faces headwinds from elections, weak population growth, and trade policy uncertainty. We anticipate a fragile outlook into the new year.

Eurozone

The eurozone faces persistent challenges. Germany’s stagnating economy is burdened by poor productivity, high energy costs, and weak export demand, particularly from China. France is grappling with rising bond yields due to fiscal pushback. Tariff threats in 2025 could dampen growth as businesses delay hiring. The baseline outlook is for a weaker euro, sluggish GDP growth, and higher peripheral spreads. The opportunity lies in cheap equity valuations and aggressive ECB easing to support domestic activity.

United Kingdom

The UK faces low productivity, labor supply constraints, and inflationary pressures from tax increases by the new Labour government. It’s less exposed to U.S. tariffs than the eurozone but still faces trade policy uncertainty. Sticky inflation limits the Bank of England’s ability to ease, with our strategists projecting the base rate will only be lowered 3-4 times to 3.75-4.0% over the next year.

China

China continues to struggle with deflation, weak consumer confidence, and potential U.S. tariffs. Stimulus programs remain underwhelming. The focus for next year will be on policy announcements and consumer behaviour. Despite the challenges, Chinese equities are cheap, and return on equity has been improving. We expect modest depreciation of the yuan in 2025.

Japan

Japan’s inflation is likely to stay near the Bank of Japan’s 2% target, marking a key economic milestone. The economy is expected to perform well by Japanese standards in 2025, with the Bank of Japan gradually normalising policy. Japanese equities are supported by strong fundamentals but face modestly expensive valuations. Japanese bonds are less attractive, while the yen remains cheap and should benefit from narrowing interest rate differentials.

Australia and New Zealand

The Reserve Bank of Australia (RBA) is set to begin gradual rate cuts in 2025, supporting modest economic growth. With elections expected in May, a potential government change could trigger fiscal stimulus. Australian equities’ discount to global peers has narrowed, and government bonds offer a healthy spread over U.S. bonds. The Australian dollar may face volatility from tariff risks, especially given exposure to China.

In New Zealand, easing monetary policy is improving the outlook. Risks include China-related exposure and trade surplus, though we expect the Reserve Bank of New Zealand to cut rates more aggressively than the RBA.