An investor's guide to potential U.S. policy changes in 2025

Executive summary:

U.S. policies are set for a major reshaping as full Republican control takes hold in 2025. To navigate the investment opportunities and challenges ahead, we explore how key policy changes may impact economic growth, inflation, corporate earnings, and interest rates.

Ultimately, we believe the major initiatives investors should watch closely are in areas such as tariffs, immigration, taxes, and deregulation, as these policies take center stage and shape the economic landscape.

These policies are likely to be:

- Neutral for economic growth with tailwinds and headwinds roughly offsetting

- Modestly inflationary (+0.3 percentage-point increase for the core personal consumption expenditures price index)

- Positive for corporate earnings (+4 ppt increase for S&P 500 Index earnings-per-share, or EPS, growth in 2026)

- Mixed for U.S. Federal Reserve (Fed) policy (we expect gradual 25-basis-point cuts into the second half of 2025 to a new normal policy rate of 3.25

- Likely to lead to higher longer-term interest rates, although much of this is already priced in

This is a live document that we will update as policies and priorities become clearer in the months ahead.

Source: Russell Investments expectations as of December 2, 2024

Source: Russell Investments expectations as of December 2, 2024 Trade policy

Key takeaways

- We assume actual tariff increases will be smaller than President-elect Donald Trump's public statements.

- A 4-ppt increase in the effective tariff rate would likely:

- Cause a one-time boost to core PCE inflation of roughly 0.3 ppt

- Be a drag on real GDP growth of roughly 0.5%

- Dent S&P 500 Index earnings growth by roughly 1 ppt

- Not impact the Fed. If the economy slows materially the Fed would cut as it did in 2019

Tariffs: How much higher?

At times, President-elect Trump has proposed a 60% tariff rate on all imports from China and a 20% tariff rate on all other U.S. trading partners. Taken literally, these steps would lift the effective tariff rate in the United States by 15 ppt (orange dot)—a historically large increase that significantly exceeds the trade restrictions from his first term.

KEY WATCHPOINT: How aggressively President-elect Trump follows through on his tariff proposals into 2025 and beyond.

First, during Trump's first term, the administration did not deliver the full extent of tariffs that were discussed on the campaign trail, suggesting that significant weight should be placed on the idea that tariff threats were used as a tool for negotiating trade deals, and U.S. trading partners were willing to seek deals to avoid damaging their economies.

Second, President-elect Trump championed the strength of the economy and stock market during his first term, and an aggressive trade war that risked both would conflict with some of his past priorities. As such, we expect a more measured strategy moving forward (green dot above).

Impact of tariffs on inflation

Tariffs can impact inflation through a range of channels including:

- The direct impact of higher import prices on core consumer goods

- Decisions by unimpacted U.S. producers to opportunistically raise prices

- Higher production costs from tariffs on imported intermediate inputs to U.S. production

- With these factors partly offset by disinflation from weaker aggregate demand

- And disinflation from U.S. dollar (USD) strength1

Bringing it all together, our baseline for trade policy lifts the year-ago core PCE inflation rate by roughly 0.3 ppt in 2026 (green vs. blue lines below).

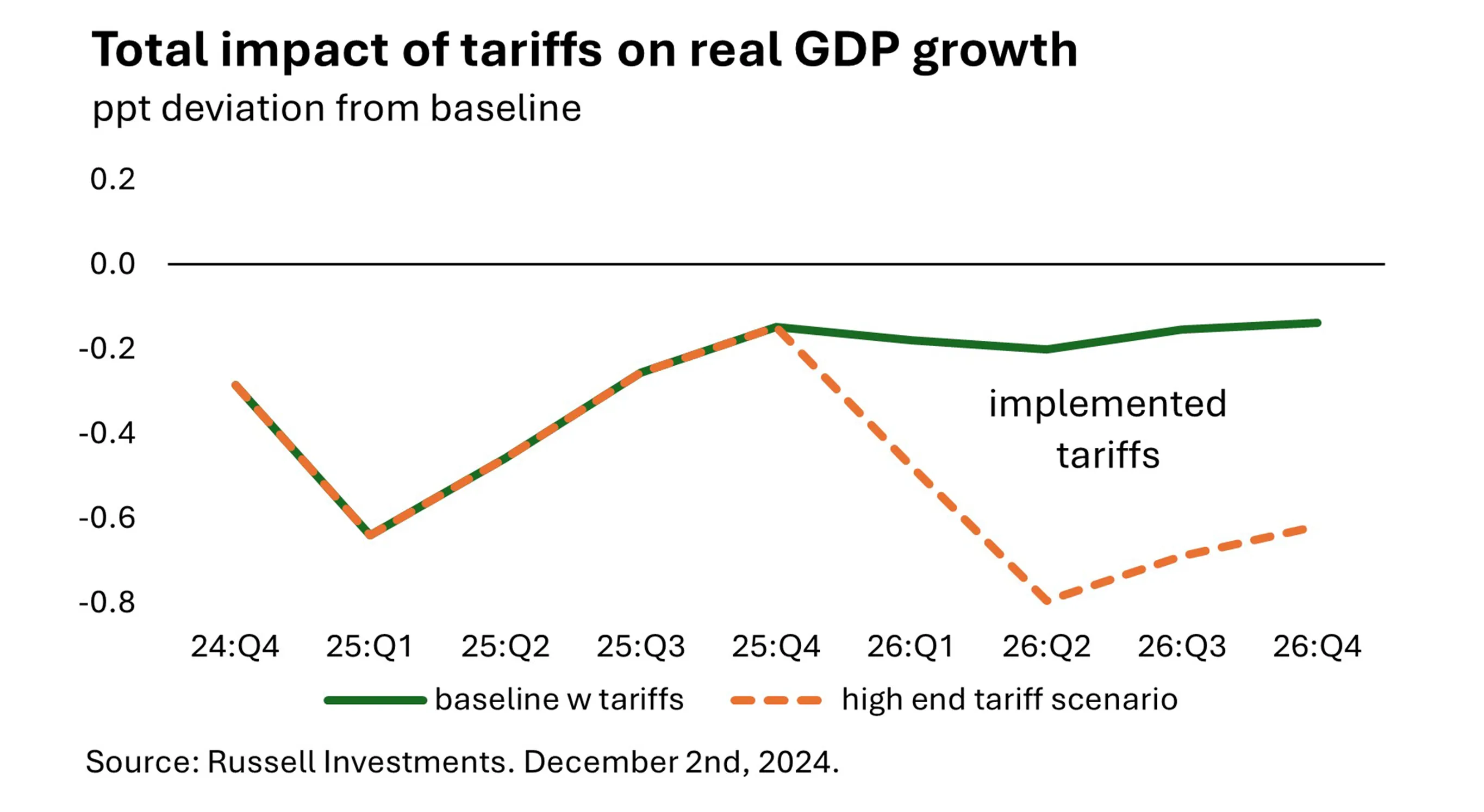

Economic growth consequences of tariffs

Nobel Prize-winning economist Paul Krugman famously noted "the dirty little secret of international trade economics is that moderate tariff rates don't have huge growth effects." This is especially relevant considering that the United States is a relatively closed economy with the import share of core personal consumption expenditures standing at only 10%.

- With that in mind, the direct and indirect effects of tariffs on economic activity can be broken down as follows: Higher import prices cause a reduction in real consumer spending power (a negative for GDP)

- Higher import prices cause consumers to shift demand away from imports (a positive for GDP)

- Other countries retaliate—often 1:1—against U.S. tariffs, hurting U.S. exports (a negative for GDP)

- Higher trade policy uncertainty can dampen business confidence and capital expenditures (capex) as firms await clarity before committing to long-term investment decisions. Note: this can be a headwind for the economy even before tariffs are implemented

- Financial conditions could tighten via a stronger dollar or negative wealth effects

On balance, we estimate a modest drag of a half percentage point on real GDP growth in 2025 and 2026. Note: the high-end tariff scenario could be worse than what is shown in the chart if trade policy uncertainty increases well beyond what is currently observed in the data.

Below shows how we’re tracking trade policy uncertainty and financial conditions. Trade policy uncertainty jumped through the end of November on news of Trump’s victory. Meanwhile, financial conditions eased following the U.S. election with Fed cuts, higher equity prices, and tight credit spreads more than offsetting dollar strength. For now, the headwinds from record high trade policy uncertainty are likely to outweigh easier financial conditions for the near-term growth outlook.

Below shows how we’re tracking trade policy uncertainty and financial conditions. Trade policy uncertainty jumped through the end of November on news of Trump’s victory. Meanwhile, financial conditions eased following the U.S. election with Fed cuts, higher equity prices, and tight credit spreads more than offsetting dollar strength. For now, the headwinds from record high trade policy uncertainty are likely to outweigh easier financial conditions for the near-term growth outlook.

How tariffs can affect earnings

Equity analysts2 have estimated that every 5-ppt increase in the effective tariff rate could pose a headwind of 1 to 2 ppt to S&P 500 earnings growth. We estimate a 1-ppt hit to earnings from trade policy.

Impact on earnings

| S&P 500 Index | 2026 EPS growth |

| IBES consensus (no tariffs) | 13% |

| With baseline tariffs | 12% |

| With high-end tariff threats | 8% |

Source: IBES Datastream, Russell Investments. December 2, 2024.

What the influence could be on Fed policy

Tariffs are a stagflationary impulse—generating both weaker growth and more inflation—and a complicated issue for central bankers. But given economists widely believe that tariffs only lead to a one-time (transitory) increase in the price level, Fed doctrine would be to focus on risks to growth and the business cycle. Put differently, tariffs are likely to create a dovish impact on policy rates.

Supporting this idea: during the last expansion, the Fed cut rates for the first time in July of 2019—with Chair Jerome Powell noting the cut was "intended to insure against downside risks from weak global growth and trade policy uncertainty."

Watchpoints

- Concrete details on timing, magnitude, and countries facing tariffs from the U.S.

- Retaliatory actions from other countries, like China

- Trade policy uncertainty and financial conditions indices (plotted above)

- Currency markets (e.g. USD-Mexican peso) as a gauge for pricing of trade risks

Fiscal policy

Key takeaways

- TCJA (Tax Cut and Jobs Act) provisions for households are likely to be extended beyond the end of 2025.

- …TCJA extensions have no impact on the economy as they are a continuation of current policy

- …but would raise the CBO's (Congress Budget Office) forecast of the debt/GDP ratio by 10 ppt in 2034.

- President-elect Trump has also talked about new tax cuts (e.g., social security, corporate, tips) and repealing the Inflation Reduction Act (IRA)

- It's unclear which, of any, of these can pass Congress. Corporate tax cuts seem the most likely.

- Lowering the corporate rate from 21% to 15% would boost S&P 500 earnings by 5 ppt…

- …with negligible positive effects for growth and inflation

- Term premia have risen notably on fiscal and other risks from the election results

- Our fixed income strategy team sees duration exposure attractive at 4.6-4.8% on the U.S. 10-year Treasury note

What new fiscal policies can we expect from a second Trump administration?

It's widely expected that President-elect Trump and the Republicans will extend measures from the Tax Cut and Jobs Act that were set to expire at the end of 2025. Most of these provisions were for households, including cuts to marginal income tax rates.

Source: Russell Investments, December 2024

Extending these TCJA provisions does nothing to economic growth or inflation. Households already benefit from them as current policy now. However, the moves would pressure the long-term fiscal trajectory of the United States. Most agencies—like the CBO—forecast deficits assuming policy evolves as legislated. If all TCJA provisions were instead extended, the deficit is projected to be $7.4 trillion larger through 2034—adding roughly 10 ppt to the national debt as a share of GDP.

Beyond the TCJA, President-elect Trump has talked about using tariff revenue to pay for an expansionary fiscal program. His fiscal plan is likely to evolve but currently has three pillars:

- Ending taxation of social security benefits

- Repealing IRA energy incentives

- Cutting the corporate tax rate from 21% to 15%

Can these proposals pass through a Republican-controlled Congress?

- Changes to social security taxes are not allowed under the budget reconciliation process. That means the move would require 60 Senate votes (i.e. Democratic Party support) and is therefore extremely unlikely to pass.

- While Republicans might support selective changes to the IRA a full repeal seems unlikely.

- Lowering the corporate rate might be the easiest measure to pass procedurally and politically

Cutting the corporate tax rate from 21% to 15% would provide an almost 1:1 boost to S&P 500 earnings growth.

| Scenario | 2026 EPS growth |

| IBES consensus (no tax cuts) | 13% |

| Cut corporate rate from 21% to 15% | 18% |

Source: IBES Datastream, Russell Investments. December 2, 2024.

From an economic perspective, corporate tax cuts would have negligible, positive effects on growth and inflation.3 an expansionary fiscal policy would be hawkish for Fed policy particularly given the economy is already strong.

Longer-term interest rates increased notably in advance of the red wave outcome, with higher term premia driving most of the increase since early September.

Could bond yields and term premia rise even further if fiscal sustainability, inflation risks, or Fed independence are challenged in the years ahead? Term premia now range between 50 and 100 bps on 10-year Treasuries and are approaching their highest levels in the post-Global Financial Crisis (GFC) period. However, past periods of elevated inflation risk (the early 1980s) or challenges to Fed Independence (the early 1970s) saw investors demand even higher risk premia for holding long bonds.

Into these risks, our fixed income strategy team judges duration exposure would look more attractive if the 10-year Treasury yield moved up to between 4.6%-4.8%.

Watchpoints:

- Tone from Republican leaders when debt ceiling reinstated on Jan. 2, 2025

- Details from President-elect Trump, Treasury Secretary, House and Senate majority leaders about fiscal plans

Immigration

Key takeaways

- Immigration flows into the U.S. are already slowing and are likely to revert to levels from 2017-19

- Weaker demographics would slow potential economic growth from roughly 2.5% to 2%

- A hit from immigration onto potential growth was already in most economists' projections

- immigration curbs are unlikely to be inflationary with wage pressures offset by weaker demand

The immigration policy agenda

President-elect Trump is likely to take executive action to limit immigration flows. We expect the contribution from immigration to U.S. population growth to rapidly downshift to levels not seen since the first Trump administration.

For context, during 2017-2019, immigration added 0.2% to U.S. population growth. But immigration has been 4-5 times stronger in recent years (blue bars). As immigration downshifts, the pace of potential (non-inflationary) economic growth is likely to slow from around 2.5% to 2%. Most economists already incorporated this change into their forecasts as both Democrats and Republicans proposed reforms on the campaign trail.

Less labor supply could pose upside risks to inflation. But two important points cut against this. First, the U.S. labor market is not overheated right now. Second, if aggregate demand slows on the back of immigration restrictions, this would offset the impact of wages onto price inflation.

Interestingly, high -frequency data suggests that over half of the expected stepdown in immigration flows has already occurred.

Larger demographic impacts are possible. The second item on President-elect Trump's campaign platform4 calls for the U.S. "to carry out the largest deportation operation in American history". If, for example, a million individuals were deported, the direct contribution from immigration to population growth would change from +0.2 ppt (blue bar, chart above) to -0.1 ppt. And a Peterson Institute working paper found that if all of the estimated 8 million unauthorized workers in the United States were deported, it could push U.S. GDP 6 ppts below baseline into the mid-2030s.

Watchpoints

- Statements from President-elect Trump and incoming border czar Tom Homan on the likelihood and scale of mass deportations

- High-frequency data on immigration flows (above)

Deregulation

Key takeaways

- President-elect Trump has the power to appoint heads of federal agencies

- He also has the power to influence the regulatory landscape for businesses

- Deregulation and policy reforms are likely, particularly for the financials and energy sectors

The president's power to appoint heads of executive agencies is granted by Article II of the Constitution. This grants the president considerable control over the regulatory agenda and how strictly agencies enforce current law.

Two sectors have received the most attention for deregulation in a second Trump administration:

Energy:

- Reverse restrictions on greenhouse gas emissions

- Support more energy production, including for oil and gas development

- Expand U.S. liquified natural gas (LNG) exports

- EPA rulemaking to decline with implications for other sectors (e.g., relax vehicle emission targets)

- Pull the United States out of the Paris climate accord once again

Financials:

- Roll back Consumer Financial Protection Bureau (CFPB) rules and guidance5

- Pause the Basel III endgame proposal which would have raised capital requirements for regionals

- Allow more mergers and acquisitions, which could benefit the sector (and other sectors, like small caps)

Broadly, a more business-friendly administration is expected to support increased merger & acquisition activity going forward with tailwinds onto small cap equity and private markets.

A few other observations:

- The heads of independent federal agencies—like Chair Powell at the Federal Reserve—can only be fired for cause. Powell's term expires in May 2026.

- If he were to resign before 2026 or be replaced in 2026, investors are likely to focus on:

- The independence of the U.S. central bank and its commitment to the 2% inflation target. Perceived threats to Fed independence could un-anchor inflation expectations and push long-term interest rates higher. Challenges to Fed independence are not unprecedented in U.S. history. Presidents Harry Truman (early 1950s), Lyndon Johnson (mid 1960s), and Richard Nixon (early 1970s) covertly and overtly pressured the central bank.6

- Following SEC Chair Gensler’s announced resignation, it is expected that new SEC leadership will likely halt/pull the agency’s pending climate disclosure rules in 2025.

The percent of small businesses citing government red tape as the single most important problem declined markedly in the first Trump administration.

And, according to the George Washington University (GWU) Regulatory Studies Center, President-elect Trump put in place 40% fewer economically significant rules by year three of his first term in the White House than current U.S. President Joe Biden did.

Watchpoints:

- Challenges to Federal Reserve independence. Chair Powell's replacement in May 2026.

- NFIB (National Federation of Independent Business) data on the impact of red tape on small business, GWU data on significant rules (above)

- Company guidance: Q4 season starting Jan. 15, 2025

1 Macro theory suggests tariffs reduce demand for foreign goods (and foreign currencies), thereby strengthening the currency of the country imposing tariffs (U.S. dollar)

2 See, for example, "US Weekly Kickstart: Looking back on 3Q results and forward to potential effects from tax and tariffs under a Trump presidency." Goldman Sachs. Published November 8th, 2024.

3 See, for example, "Comparing Fiscal Multipliers" published by the Committee for a Responsible Federal Budget in October 2020. The fiscal multiplier on corporate tax cuts is estimated to be very small – at between 0x and 0.4x. Cutting the corporate rate is estimated to be worth $700bn over 10 years or 0.2% of GDP. At a 0-0.4x fiscal multiplier that would imply a 0 to 0.08% boost to real GDP growth.

4 Source: https://www.donaldjtrump.com/platform

5 See, for example, https://www.mcglinchey.com/insights/trump-2-0-potential-cfpb-changes-in-2025/

6 See, for example, "21st Century Monetary Policy" by Ben Bernanke (2022).