Bank of England cuts rates in spite of services inflation

Executive summary:

- The MPC has decided to reduce the bank rate from 5.25% to 5.00% despite high June services inflation reaching 5.7% year-on-year.

- A majority of five members opted for a cut of 25 basis points, while the remaining four advocated for unchanged interest rates.

- Although the decision was expected by most analysts, bond markets still reacted to the announcement at noon today. The yield of 10-year UK gilts fell to a low of 3.91% after the decision.

Today, the MPC decided to reduce the bank rate from 5.25% to 5.00% despite high June services inflation of 5.7% year-on-year (partly driven by prices for hotels and live music) that some observers had attributed to Taylor Swift’s “Eras” tour coming to the UK that month.

A majority of five members1 opted for a cut of 25 basis points, while the remaining four advocated for unchanged interest rates. At the previous meeting in June, the MPC had voted 7-2 to hold rates steady. Today’s decision was expected. Of 60 economists surveyed by Reuters, 49 had predicted the cut. Money market traders had been somewhat less confident, projecting a 60% likelihood of lower rates ahead of the decision.

Recent retail sales and business confidence data revealed sluggishness in UK economic activity, tipping the balance towards a rate reduction. With today’s move, the European Central Bank and the Bank of England (BoE) have started their rate cutting cycles ahead of the U.S. Federal Reserve, which is widely expected to follow suit at their September policy meeting.

UK services inflation impacted by one-offs

Price increases for restaurants and hotels, health, and other services were widely seen as a major stumbling block to starting the easing cycle. Elevated service inflation of 5.7% in June had been meaningfully above the projection of 5.1% from the BoE’s last Monetary Policy Report published in May, but the MPC decided to look through some of the one-off effects. Aside from Taylor Swift fans driving up hotel and concert ticket prices, there were index-linked adjustments to rents and communication services that reveal more about past inflation than current price pressures.

Importantly, the labour market cooling that has been underway for months continues apace and is expected to dampen wage growth, feeding into lower future inflation for services. The unemployment rate rose to 4.4% in the three months ending in May 2024 from a cyclical low of 3.6% in mid-2022. Job vacancies, which are a leading indicator for wage growth and unemployment, have fallen continuously for 24 months.

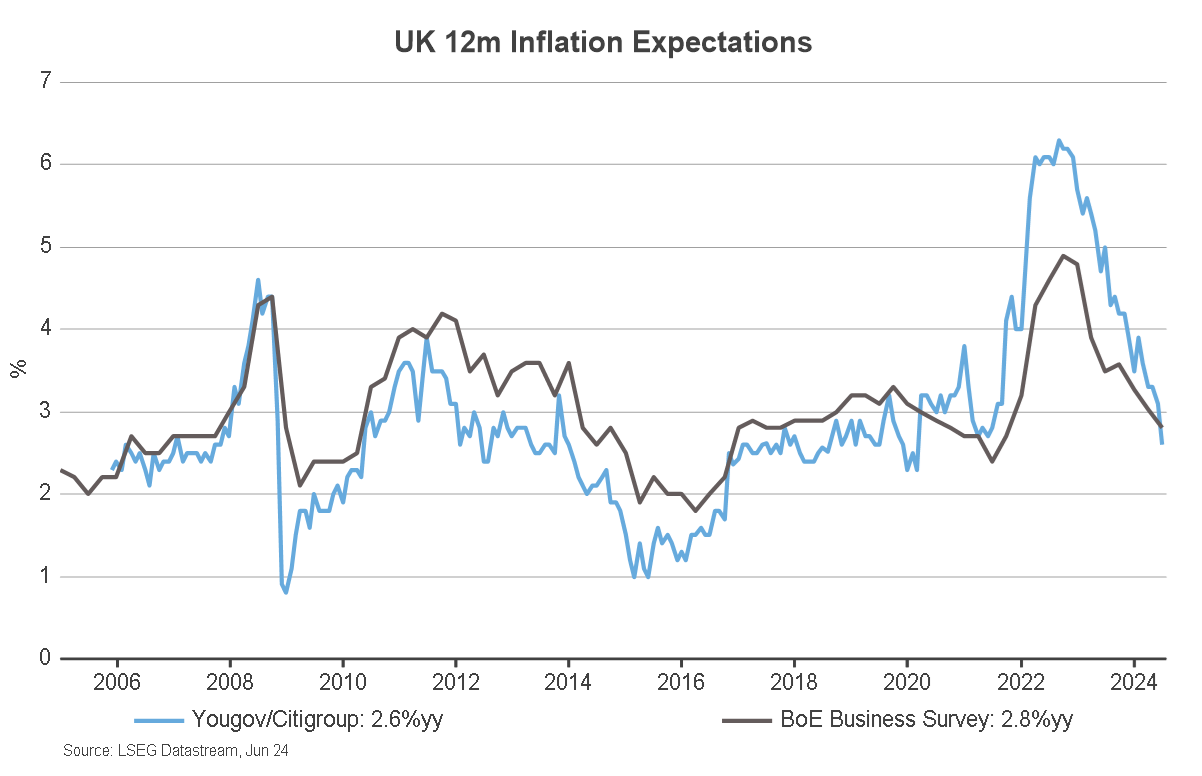

What should also be reassuring to the BoE is the return of inflation expectations to normal levels. As shown in the Chart, the Yougov/Citi survey of consumers and the BoE’s business survey for 12-month ahead inflation expectations are back to 2.6% and 2.8% respectively, in-line with pre-pandemic levels. The period of very high inflation in 2022/23 has not embedded itself in the psyche of consumers and businesses, making the central bank’s job easier.

Inflation expectations back to normal

Market reaction

Although the decision was expected by most analysts, bond markets still reacted to the announcement at noon today. The yield of 10-year UK gilts fell to a low of 3.91% after the decision. Long-term interest rates in the UK had fallen along with global bond yields in recent weeks as inflation pressures appear to ease across the world economy. We believe that central banks will validate the markets’ expectations for further rate cuts over the next 12 months in the UK and elsewhere, which would be a relief for mortgage borrowers.

In foreign exchange markets, sterling has been the strongest G10 currency2 this year, but the pound fell in anticipation of today’s rate cut decision and was down 0.6% versus the U.S. dollar. Investors have built up significant long positions in sterling, making it vulnerable to a short-term correction. The downside for the pound vs the dollar should be modest, in our view, as the U.S. Federal Reserve is also expected to cut rates at their next meeting in September.

The bottom line

The BoE reduced its key interest rate from 5.25% to 5.00% today in a tight 5-4 decision. Since the BoE’s last rate hike in August 2023, the 10-year UK gilt yield has traded in a range between 3.50% and 4.65%. After today’s decision, and in anticipation of further cuts in an easing cycle, we expect bond yields to drift towards the lower end of their range.

Changes in bond yields have a direct impact on the liability valuation and funding status of Defined Benefit pension schemes. Consequently, it is crucial to set up a robust strategy to lessen the effects of interest rate and funding level volatility. In the aftermath of the gilt crisis in 2022, it is prudent for pension fund trustees to devise and enact a clear governance and execution framework for liability hedging.

1 Andrew Bailey, Sarah Breeden, Swati Dhingra, Clare Lombardelli and Dave Ramsden voted for a cut while Megan Greene, Jonathan Haskel, Catherine L Mann and Huw Pill preferred to keep rates unchanged.

2 G10 currencies are the world’s most traded and liquid currencies. The group includes the Australian dollar, Canadian dollar, Swiss franc, euro, UK pound sterling, Japanese yen, New Zealand dollar, Norwegian krone, Swedish krona and US dollar.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.