France elections: Far-right rejected in second round, but so is Macronism

Executive summary:

- The second round of the French National Assembly election delivered a hung parliament, as expected, but also a huge surprise. The far-right party National Rally (RN) fell from first to third place and the left-wing alliance of the Nouveau Front Populaire (NFP) came out on top.

- President Macron’s centrist coalition outperformed the first-round result by squeezing into second place. That said, Macronism has been as decisively rejected as the far-right populism of the RN.

- The prime minister from Macron’s party, Gabriel Attal, offered his resignation. It is unclear who will succeed him, and which coalition and policies can find a majority in a split National Assembly.

- The market’s worst-case scenario of a far-right majority is averted, but uncertainty remains high and could continue to weigh on French financial assets.

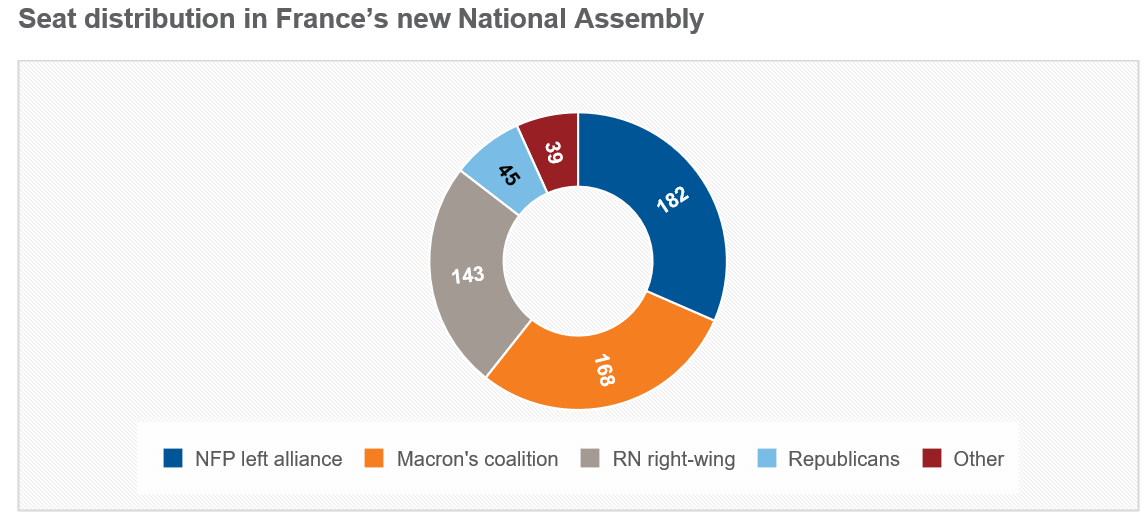

In the second round of parliamentary elections, French voters decisively rejected the far-right populism of National Rally (RN), the party of former presidential candidate Marine Le Pen. The party dropped from first place after the first round to third place, winning 143 seats in the new National Assembly (see Exhibit). The threat of an RN majority had mobilised voters; turnout was at the highest level for more than four decades.

The newly formed left-wing alliance Nouveau Front Populaire (NFP) will be the strongest bloc in the National Assembly with 182 seats. However, it is an assortment of leftist parties that was only put together for these elections three weeks ago. President Macron’s centrist coalition leapfrogged the RN to place second, winning 168 seats. No party is anywhere near the absolute majority of 289 seats. France has a hung parliament, with three major blocks but no clear path to a government. On Sunday evening, the prime minister from Macron’s party, Gabriel Attal, immediately offered his resignation.

What does the result mean…?

There are arguably no winners. It is unclear how a new government can be formed in the hung parliament that emerged from Sunday’s polls. Financial markets were worried about a far-right RN majority but also wary of a prominent role for the hard-left La France Insoumise (LFI) under the leadership of Jean-Luc Mélenchon. The RN had laid out policies for the 2022 presidential election that were estimated to have a price tag of €100bn, including reversing Macron’s controversial increase in the retirement age. That said, the President’s supply-side reforms are also opposed by the left-wing LFI and are unpopular with the electorate. Despite his party outperforming expectations and their first-round result, Macronism has taken a big blow over the last month. He may have to work with a prime minister chosen by the NFP or appoint a technocratic “government of national unity”.

…for European bonds and the euro?

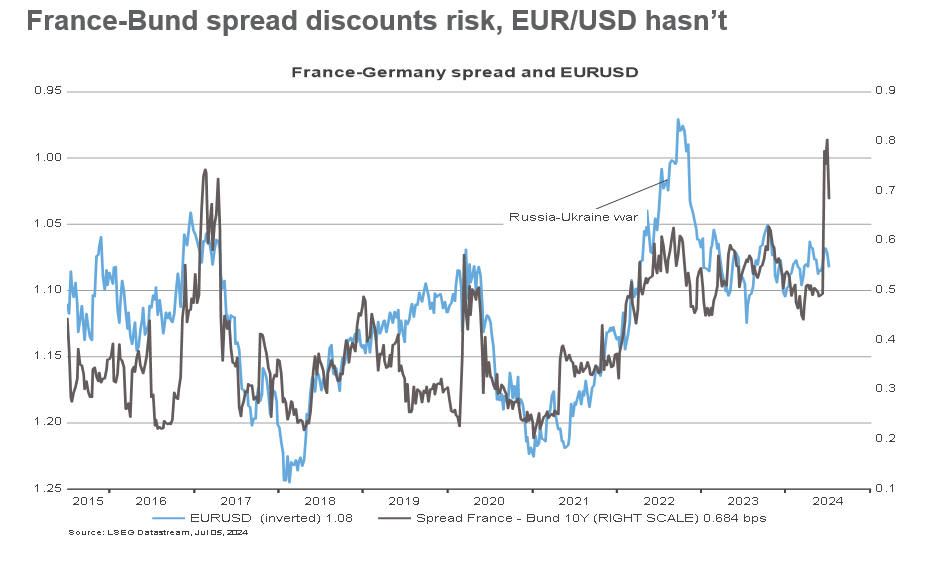

Political uncertainty has been a heavy weight around the neck of European markets, especially French assets. A good barometer of political risk emanating from the election is the spread of French over German government bonds (Bunds) with 10 years’ maturity. This spread had risen from around 0.5% before the election was called to more than 0.8% before the first round of the election (see chart below). It dropped back to around 0.7% when left and centrist parties resolved to tactically block the RN from winning a majority.

The EUR/USD exchange rate is a similar indicator of perceived political risk and usually correlates inversely with the spread. Unlike the latter, EUR/USD has barely budged from its 1.08 level during the recent period of electoral uncertainty.

When foreign exchange markets (FX) re-opened in Asia today, the euro initially dropped by a modest 0.4%, reflecting relief mixed with disappointment at the strong showing of the far-left. Although EUR/USD recovered to trade flat, higher implied FX volatility shows that traders are still nervous. That is the case in bond markets too, where the 10Y France-Bund spread hovered around an elevated 0.7% level.

…for French and European equities?

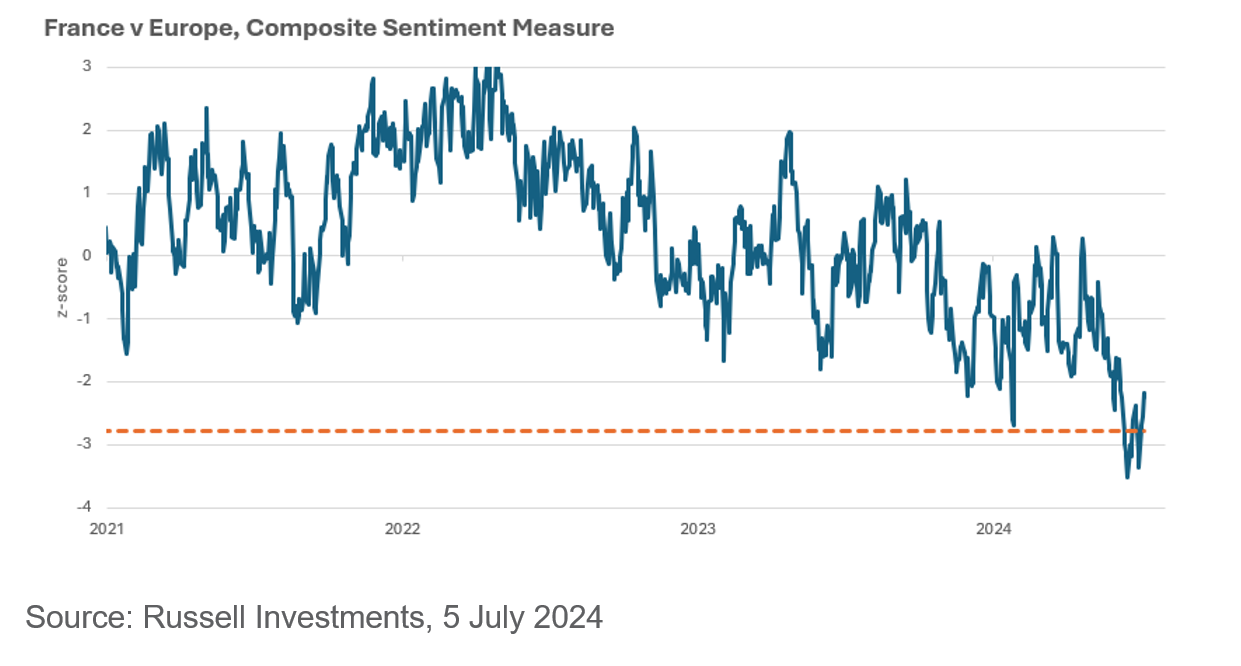

French stocks had sold off strongly in recent weeks on the risk of a right-wing euro-sceptic government, continuing their underperformance against other euro area equities since mid-2023. On our composite contrarian sentiment indicator for French vs. European equities, an oversold signal was triggered at the end of June (see chart), suggesting that a countermove was becoming more likely. While relief at last week’s first-round result had halted the sell-off, today’s outcome does not look like the catalyst that markets need for a strong rebound. Thus, the CAC40 benchmark index of French stocks dropped by 0.5% at the open this morning, but had risen by nearly 1% vs. Friday’s close by mid-morning.

French equities oversold

1. Source: Institute Montaigne.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.