Long-Term Portfolio Positioning Amid Tariff Turmoil

2025 STRATEGIC POSITIONING

Key takeaways

- We prefer equity to credit at a three-to-five-year time horizon

- In fixed income, we remain overweight duration

- We believe private markets present attractive opportunities for clients with long-term time horizons

How markets behave over a three-year period carries a lot of uncertainty. In 2025, we see several risks: tariffs, a renegotiation of defense alliances and stocks living up to earnings expectations. While the issues clouding visibility may change over time, the forecast is never 100% clear.

In setting a strategic allocation, we use a dual-horizon approach. First, we develop an allocation using equilibrium-like capital market assumptions tailored to a 20-year horizon. Next, using a refined description of where we see markets evolving over the next three to five years, considering the path of interest rates, spreads and the different economic scenarios, we make adjustments to our long-term positioning, incorporating this three- to -to-five-year forecast.

Let’s take a look at our capital market assumptions and discuss how we are strategically positioned for 2025 and beyond.

Capital Market Outlook

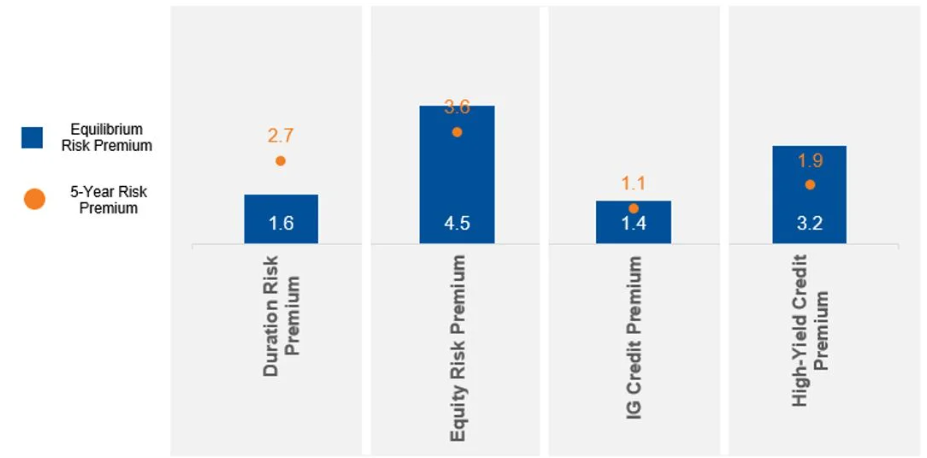

Exhibit 1 shows our capital market assumptions over the next five years relative to equilibrium.

Notes: Duration premia: 10-year treasury against cash; IG credit: ICE BofA Single-A 5-7yr US Corporate Index premia over 5-yr Single-A zero-coupon bond. HY: ICE BofA Single-B HY Index over 5-yr B zero-coupon bond. Equity premia: Excess return over 3-month T bill, equilibrium returns refer to US LC, next 5 years refers to Global Dev LC.

Equities: With high cash rates, modestly reduced earnings growth forecasts over the next several years, and high P/E (price-to-earnings) ratios in certain segments, we expect the equity risk premium to be slightly lower than normal.

Duration: We forecast decreasing cash rates, with a steepening yield curve. Our forecast is for Treasuries to produce a higher yield than cash along with capital appreciation from roll down.

Credit: With a tight starting point for credit spreads, yields are likely to be lower than normal. Moreover, we anticipate spreads eventually reverting to more normal levels, which would lead to capital depreciation. Together, these produce a lower forecast for the credit risk premium over the coming years.

Equity-Bond Correlation: The stock-bond correlation is an important consideration in balancing risk-on and risk-off exposures. To maintain similar volatility, more bonds are required in an allocation when this correlation is elevated. We show the historical rolling correlation in Exhibit 2, where we note that this correlation measure, currently at 0.2, appears to be receding since its recent peak. Inflation shocks from trade or fiscal policy missteps can cause this measure to rise again, however.

Cyclical considerations

Exhibit 2: Rolling 1-Year Correlation – Stocks & Bonds

Note: 52-weeks rolling correlation between S&P500 and 10-year US treasury

Increased unpredictability: There is heightened uncertainty coming from the current U.S. administration’s policies, such as challenging existing global trade arrangements, border policies and defense alliances.

Recession risk: Lower immigration, reduced government spending and higher tariffs are likely to temper U.S. growth. Despite these headwinds, the U.S. economy looks reasonably strong, although business and consumer confidence are deteriorating.

Persistent moderate inflation: We expect inflation to gradually decline toward the U.S. Federal Reserve’s target, setting the stage for rate cuts. Although there will be uncertainty around the impacts of tariffs and restrictive immigration policies, we expect two rate cuts in the latter half of the year.

Unemployment and wage growth: Our expectation for job and wage growth points toward a balanced rather than an overheating economy.

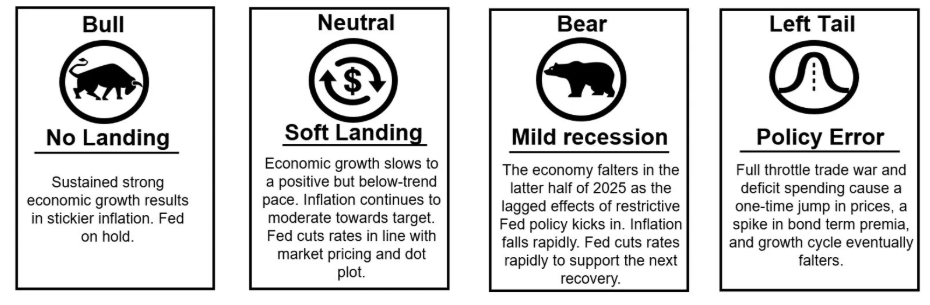

We summarize cyclical risks impacting markets over the next three to five years into the following potential scenarios.

Exhibit 3: Economic Scenario Definitions

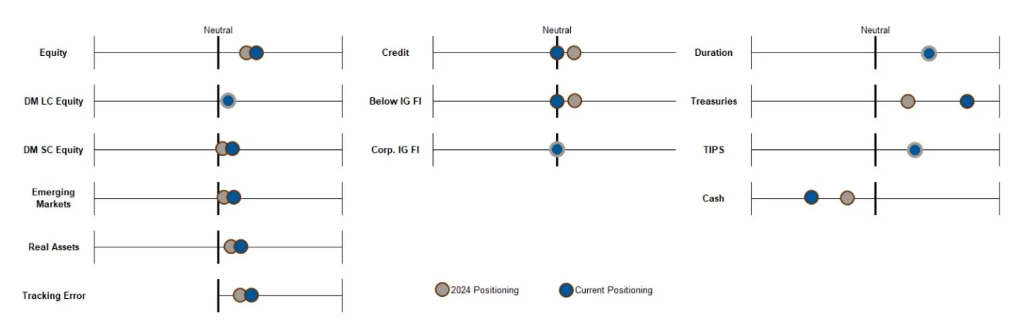

Taking account of our CMAs (Exhibit 1) and cyclical risks, we come to the following strategic positions.

Exhibit 4: Strategic Positions against Benchmark

Positioning Rationale

With a relatively low credit premium forecast—a result of compressed spreads—we see limited upside for credit exposure. At the same time, there are large segments of the global equity market that are reasonably priced given the cyclical backdrop. As a result, we see more risk-adjusted upside in equity than in credit.

Nominal Treasury Bonds and Duration

We remain overweight duration. Over the next five years, we project 10-year U.S. government bonds to outperform cash by 2.7%, compared to 1.6% over an equilibrium-like horizon. We think the duration overweight should be taken in the belly of the curve (intermediate bonds).

Treasury Inflation-Protected Securities (TIPS)

We use inflation-linked bonds and intermediate nominal bonds to achieve our duration positioning. The real yield on TIPS is in the 1.5%-2% range, which is reasonably attractive against history. Moreover, policy errors coming from trade wars and other actions have the potential to trigger an inflation episode. With high real yields and inflation protection, we see TIPS as a safe way to obtain duration exposure.

Alternative Diversifiers

Alternative diversifiers, such as cross-asset trend and actively managed long volatility strategies, can complement duration in protecting portfolios from drawdowns. We view these positions as stable diversifiers in a portfolio. Long volatility mitigates sharp drawdowns, while cross-asset trend provides resilience during prolonged declines. Unlike bonds, these strategies are not structurally exposed to inflation shock risk, enhancing diversification.

Private Markets

We believe private markets present attractive opportunities for clients with long-term time horizons. Trade wars can cause considerable shifts in supply chains that long-term private asset investors can capitalize on—with the right insight. Of course, investing in private assets comes with liquidity constraints, locking up capital for longer periods. Like alternative diversifiers, private equity is a stable recommendation in portfolios that can take on illiquidity.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.