Understanding the ESG landscape: Key insights from our 2023 Manager ESG Survey

Executive summary:

- Russell Investments’ 2023 Manager ESG Survey, now in its ninth year, continues to offer valuable insights into the evolving landscape of ESG practices within the investment management industry.

- Our survey covers a wide range of topics including ESG commitments, challenges, and reporting, Net Zero target setting, active ownership, and diversity.

- For active managers, key challenges include the availability of data, reporting standardisation for corporates, and meeting diverse client needs. Nevertheless, our research shows that commitments to responsible investing reporting frameworks and initiatives continue to rise.

The backdrop

Introduced in the early 2000s and initially an esoteric term, ESG—standing for environmental, social, and governance criteria—has firmly embedded itself in mainstream discourse. Even so, the investment community continues to grapple with how to integrate ESG elements into their decision-making processes. Notably, while regions like Europe, Canada, and Australia have fortified their reporting mandates, the United States remains engaged in a contentious debate.

For investment professionals, key challenges to ESG integration include the availability of data, lack of standardised reporting for corporates, and meeting diverse client needs. Nevertheless, fewer managers are reporting that ESG considerations do not affect their investment decisions, and there is an upswing in commitments to responsible investing reporting frameworks and initiatives. Our research suggests that ESG has firmly established itself as a lasting force in the investment landscape.

The survey

Russell Investments’ 2023 Manager ESG Survey, now in its ninth year, continues to offer valuable insights into the evolving landscape of ESG practices within the investment management industry. Garnering results from 169 participants globally—a mix of equity, fixed income, real assets, and private markets asset managers—the survey offers a comprehensive view of industry-wide perspectives on ESG integration, the momentum toward net-zero objectives, diversity initiatives, and more. The participant roster is broad, encompassing a range of investment approaches from sustainable investing boutiques and large traditional managers. The collective assets under management (AUM) for 2023 was nearly US$20 trillion1, with entities ranging from firms with an AUM of less than $10 billion to those with over $500 billion. Geographical diversity is also evident, with a significant majority based in the U.S., but also strong participation from Europe, the UK, Australia, and New Zealand.

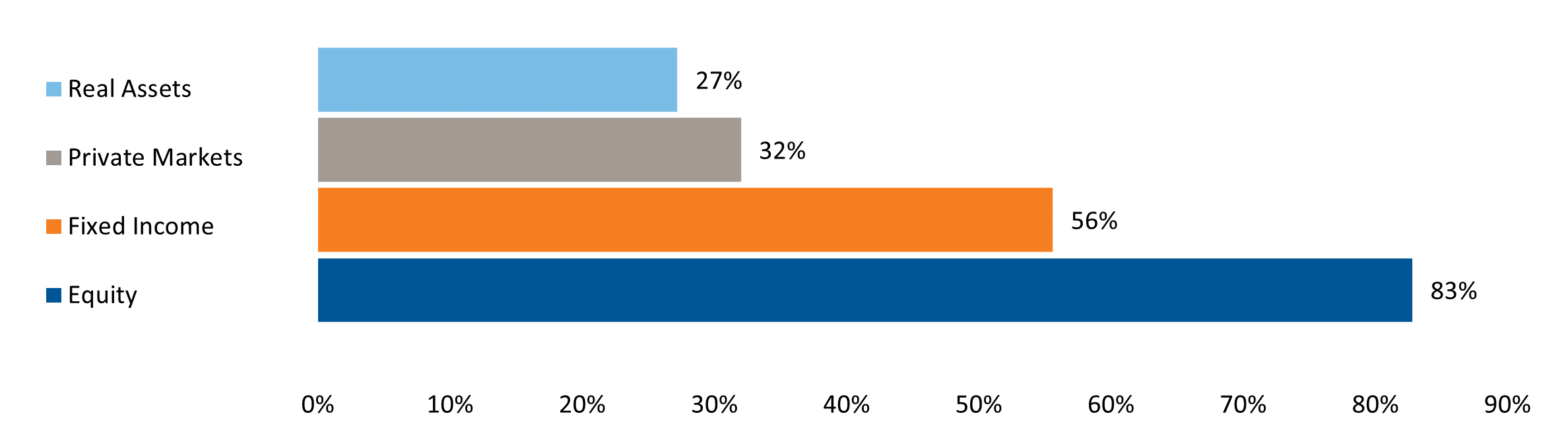

Respondents' asset class offerings

(Click image to enlarge)

While the response rate for the 2023 survey was lower year-over-year—possibly due to survey fatigue— the demographics of our respondents suggest we continue to capture a broadly representative set of industry perspectives.

Responses received for the 2023 survey were often consistent year-over-year, with results suggesting that a number of trends are continuing.

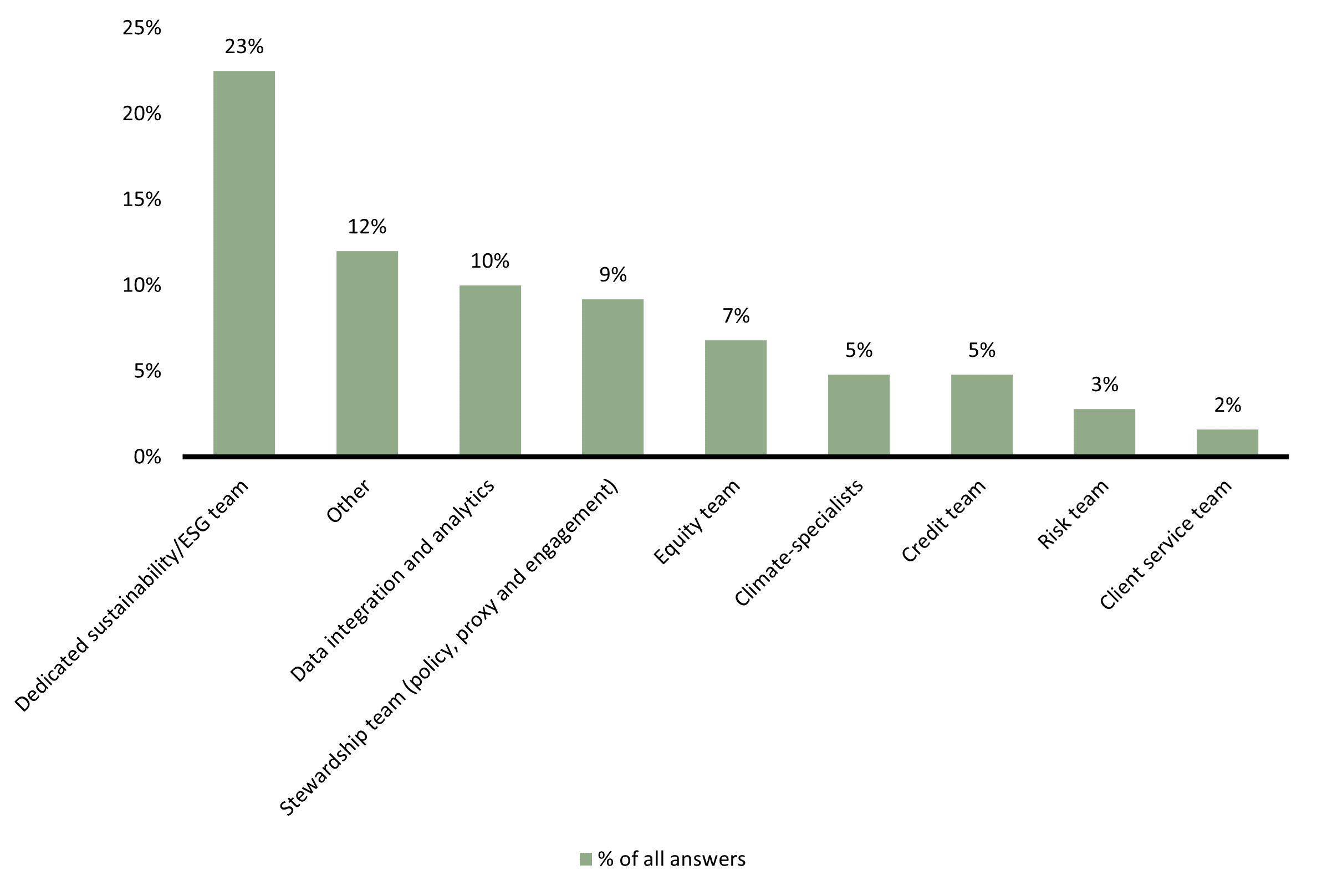

Managers continue to hire into ESG-related roles

Employment trends among respondents reflect rising attention to sustainable investing. Our survey results suggest that managers continue to hire into ESG-related roles, adding specialists across functions including data analysis and compliance. As shown below, 75% of participants reported hiring dedicated ESG personnel, primarily to ESG or sustainability teams. 10% of firms also reported adding to their data integration and analytics teams. “Compliance” was a frequent response added under “other”. Increasing regulatory requirements around the globe“but primarily in the UK and Europe“have led to an increased demand for ESG-specific compliance.

In the past year, in which areas have you hired dedicated ESG resources?

(Click image to enlarge)

ESG integration

As in the past, our survey included several questions meant to gauge the managers’ means of integrating ESG-related data and information within their investment processes. Asset managers continue to tap into a wide range of ESG information sources to bolster investment decisions. We’ve observed rising emphasis on active ownership as an investment tool; indeed, it emerged as the number one ESG information source according to participants. Most striking: this year only 7% said that ESG factors do not drive investment decisions, markedly down from the 22% recorded in 2022.

When do ESG inputs or issues most often impact your firm's investment decisions?

(Click image to enlarge)

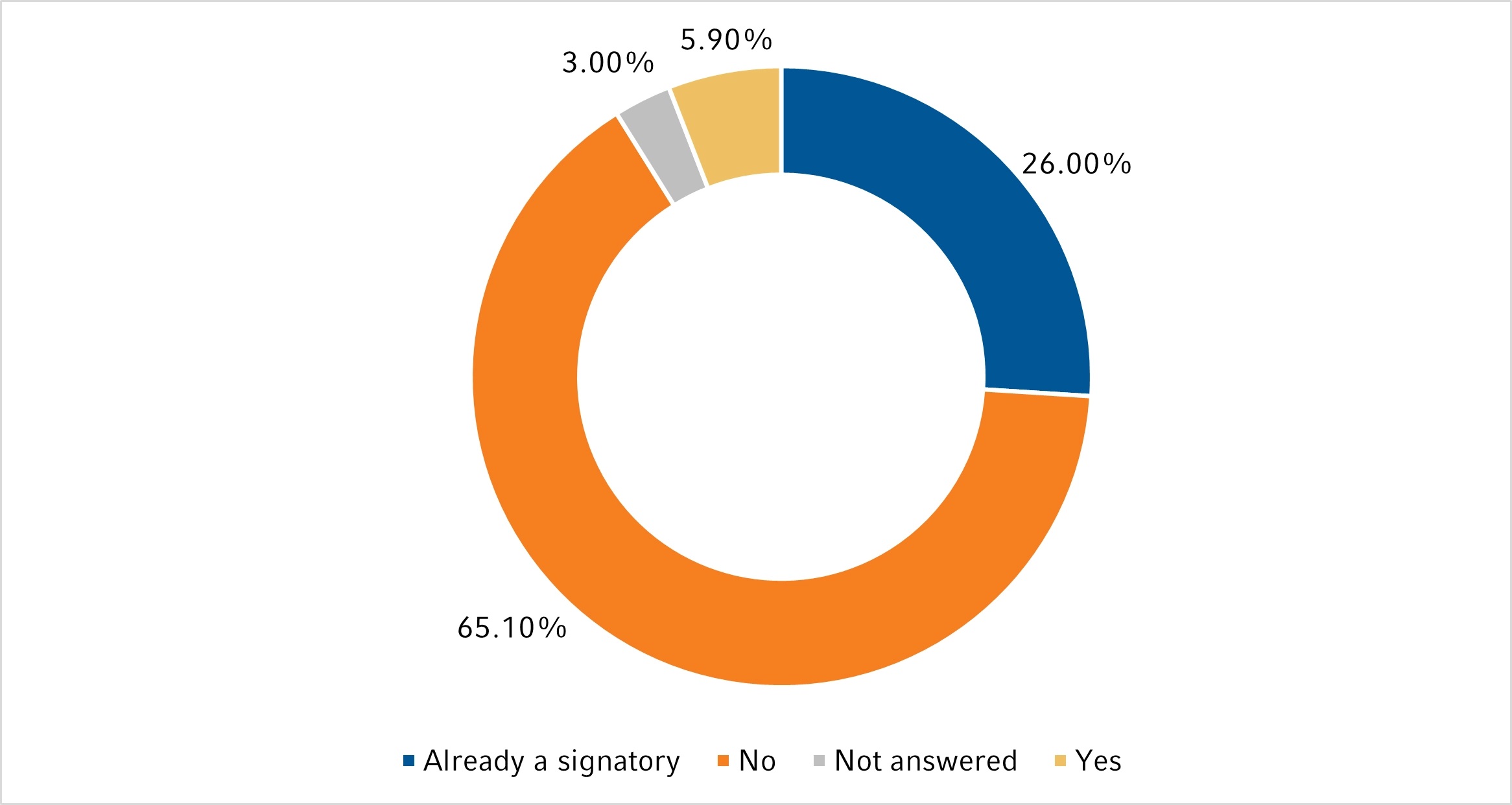

Respondents indicated consistent momentum toward Net Zero initiatives.

As the focus on sustainable investing intensifies, the commitment to the Net Zero Asset Managers initiative among firms paints a revealing picture. 27% of respondents indicated that they have already committed to the Net Zero Asset Managers initiative, while 6% of respondents indicated they plan to sign up in the next 12 months. This figure is the same as in 2022, which could suggest similar adoption momentum, despite a notable public withdrawal by a large, U.S.-based asset manager in 2022. Many also explained that while their plans are unsettled, they are currently evaluating the initiative.

Adoption varies dramatically by region. 80% of respondents domiciled in Europe are already signatories, versus 58% in the UK, 40% in Japan, and only 20% in the U.S. Managers responded that the Paris Aligned Investment Initiative’s Net Zero Investment Framework (NZIF) is widely preferred as the framework for establishing targets.

Upcoming manager signatories in 12 months

(Click image to enlarge)

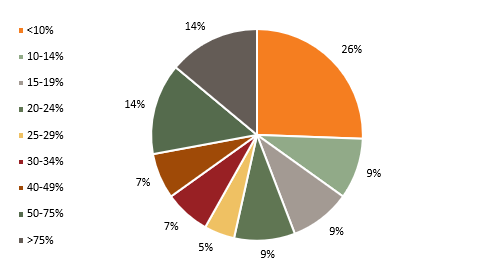

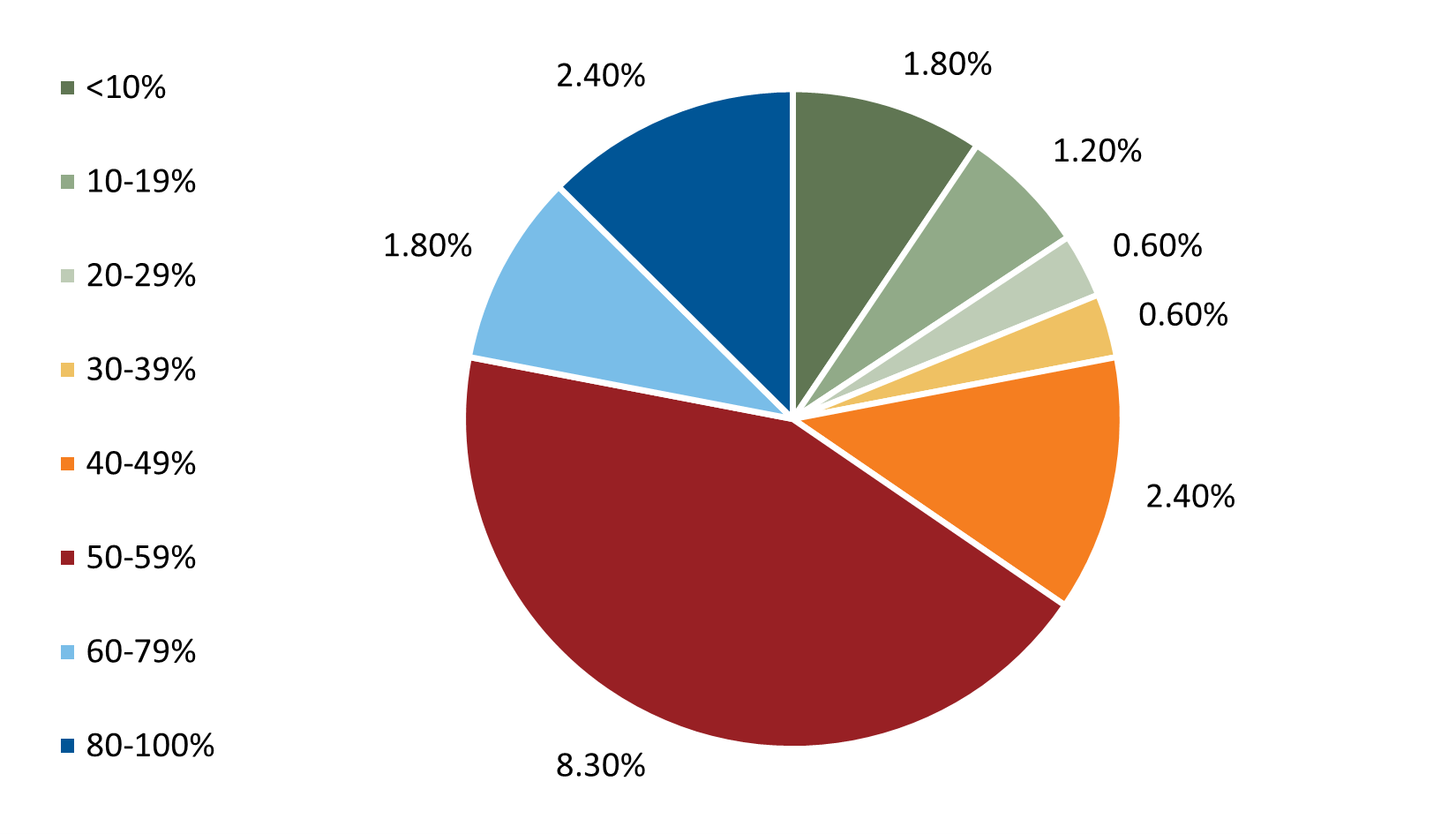

Net zero aligned assets under management are low but managers’ interim targets suggest a meaningful ramp up into 2030.

Among firms that are NZAMi signatories, the majority currently manage only a small portion of assets in alignment with net-zero objectives. However, they anticipate this number to grow, as reflected in their 2030 targets. Specifically, 35% of managers, represented in orange and blue in the pie chart below reported that current “net zero” assets are equal to or less than 14% of their total AUM.

Exhibit 4: AUM managed in line with net zero goalsRespondents' AUM currently managed in line with net zero goals

(Click image to enlarge)

Meanwhile, two-thirds have said that their 2030 interim targets are to reach 50% or more of AUM in line with net zero by 2030. 13% of managers in our survey are already managing 80-100% of assets in alignment.

Exhibit 5: Interim net zero targetsRespondents' 2030 interim net zero targets

(Click image to enlarge)

Data is still one of the biggest challenges to integrating ESG information

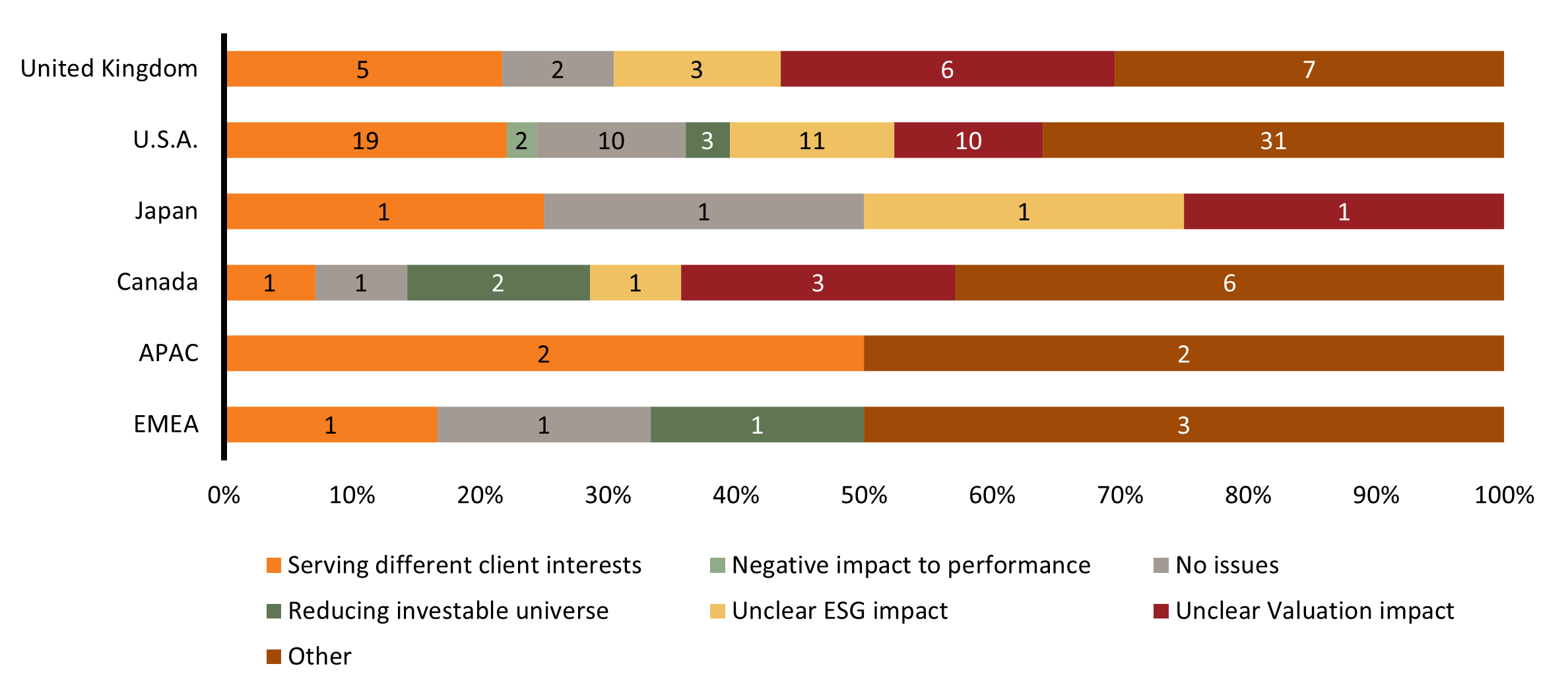

Over the years, our survey results have consistently revealed differences among regional perspectives, and 2023 was no different. We presented managers with seven options (detailed below) and asked them to pinpoint the most significant obstacle to incorporating ESG information.

A notable segment selected “other”, while articulating concerns specifically related to data. They emphasised the hurdles posed by inadequate disclosures and insufficient standardisation of disclosure frameworks for companies, data providers, and rating agencies.

Many managers also flagged the difficulty of serving diverse client interests when assimilating ESG-related information into investment decision making—an answer reflected by respondents from all regions. Interestingly, only managers in the United States cited negative performance repercussions as a challenge, possibly mirroring the country’s ongoing political debates around financial materiality.Exhibit 14: Challenges to ESG integration by region

What is the biggest challenge to integrating ESG information?

(Click image to enlarge)

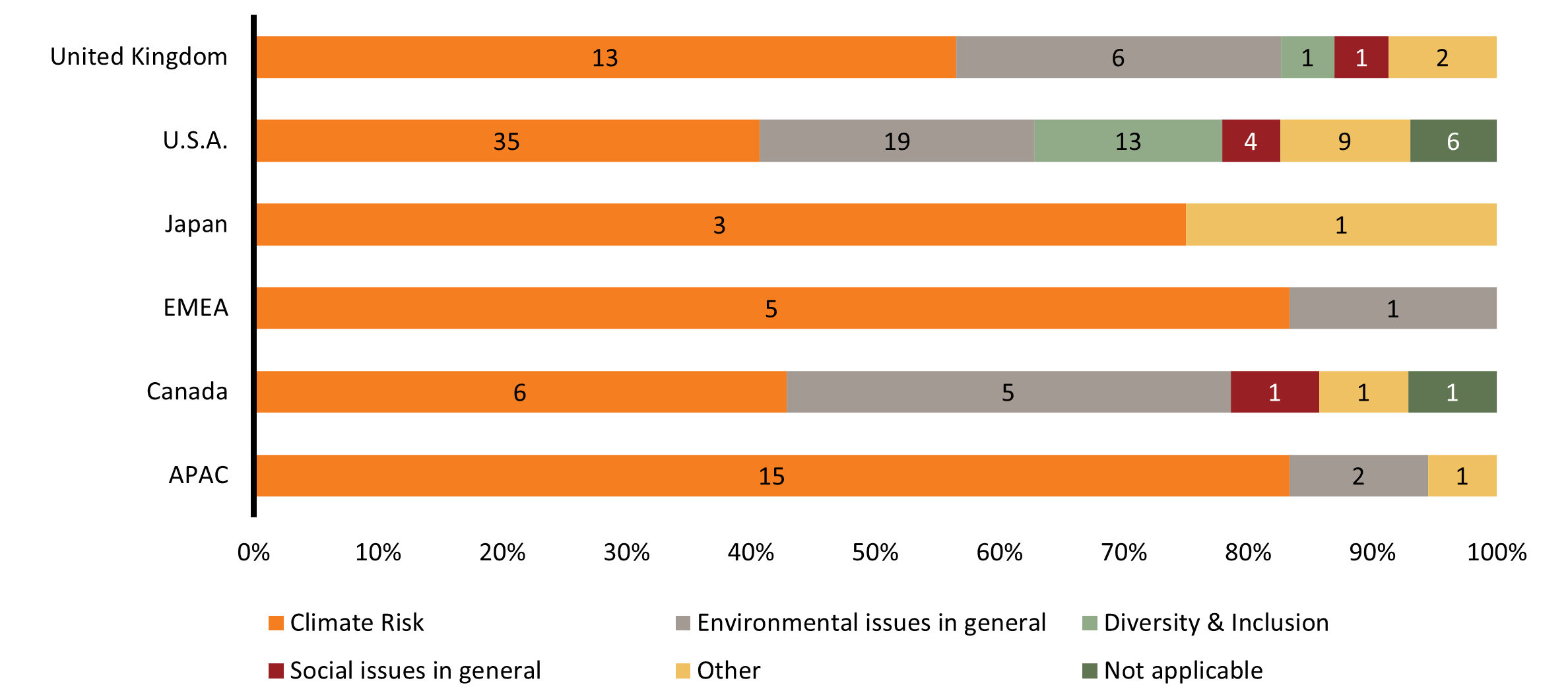

Climate remains the greatest ESG-related concern among managers’ clients.

We also invited respondents to share their views on their clients’ top ESG-related concerns. While responses varied by region and asset class, apprehensions surrounding climate risks and environmental issues dominated across the board. Notably, in the United States—where such topics can spark more debate—climate risks and environmental issues captured 54% of the responses. These findings were aligned with our 2022 survey results.

Social issues once again received lower emphasis from respondents, with diversity noted as the key issue by 13% in the U.S. and by a few managers in the United Kingdom. Some respondents did not provide answers or indicated “not applicable” status across various asset classes, underscoring the complexity of addressing these ESG factors uniformly across different investment types.

Exhibit 15: Top ESG concerns by regionClients' top ESG concerns - as reported by managers

(Click image to enlarge)

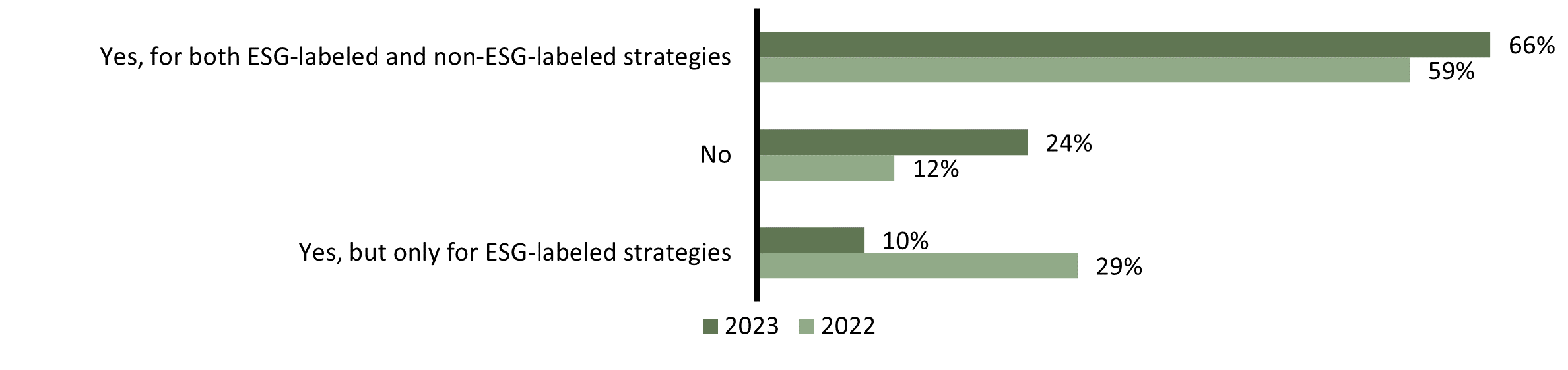

Managers continue to increase reporting of ESG metrics.

A higher proportion of managers this year indicated they are reporting ESG metrics for all funds. At the same time, we saw an increase in the percentage of participants saying that they do not provide any ESG-related reporting. Given our understanding of the broader trends in manager solutions, we’re inclined to believe this reflects a shift in the collection of participants rather than a reversal in reporting trends. When segmenting results by asset class, private markets managers indicated “No” reporting at the highest rate. In 2023, 66% of managers reported providing ESG reporting for all strategies while 10% provide it for ESG-labelled strategies only.

Managers providing ESG reporting

(Click image to enlarge)

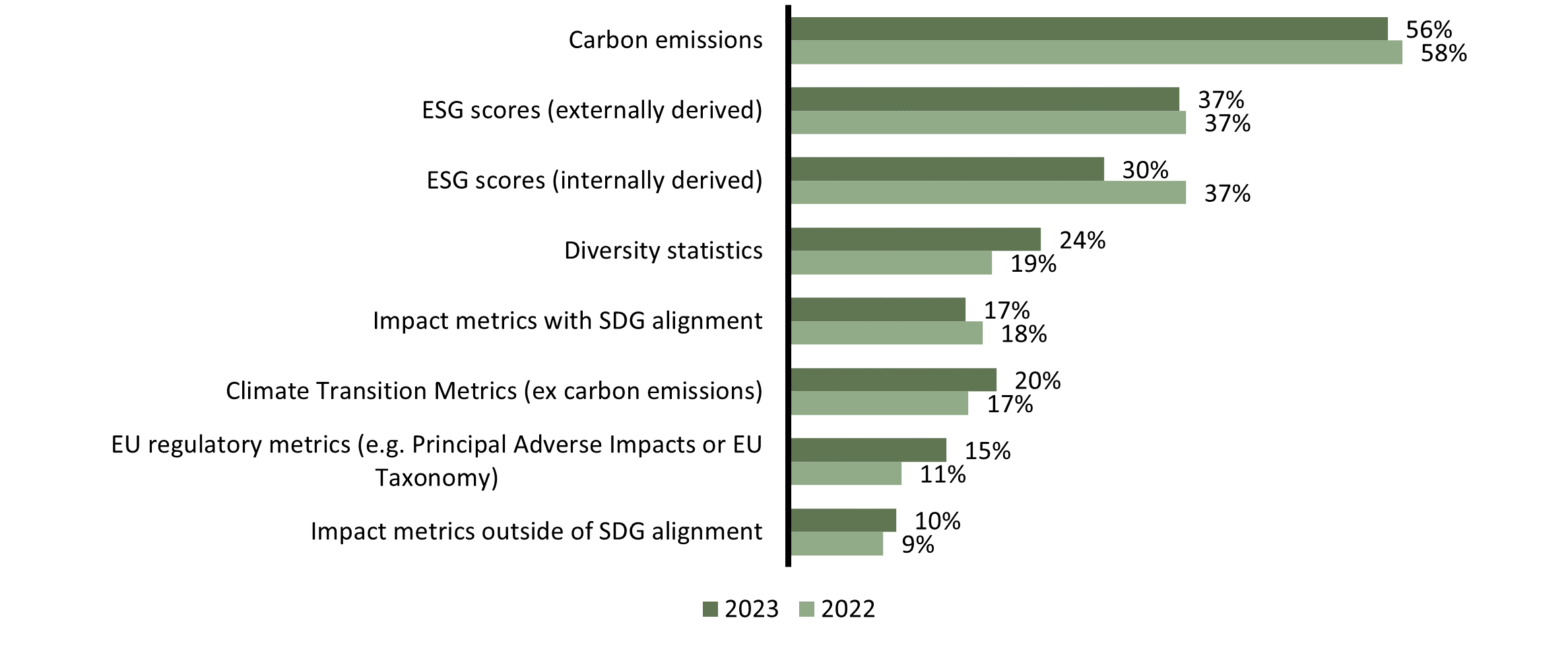

In a separate question, managers responded that carbon emissions remained the most popular reporting metric in both 2022 and 2023. It was chosen by over 50% of respondents, while an increasing proportion reported disclosing diversity statistics and other impact metrics.

In a separate question, managers responded that carbon emissions remained the most popular reporting metric in both 2022 and 2023. It was chosen by over 50% of respondents, while an increasing proportion reported disclosing diversity statistics and other impact metrics.

Commonly reported ESG metrics

(Click image to enlarge)

More managers are choosing to disclose diversity metrics.

Our survey asks a series of questions about the representation of women and minorities across participating asset management firms. Russell Investments uses this diversity data to gain insights into our pipeline of products and associated managers. While recognising the complexities of reporting this data, we nonetheless advocate for enhanced transparency in this area. We encourage managers to disclose the presence of women and minorities within their ownership structures, boards, senior leadership teams, and among their investment professionals. For the purposes of our survey, “diversity” is described simply as women or minorities, without imposing a specific interpretation of these terms.

This year’s survey results suggest a modest improvement in disclosure rates. For example, the percentage of managers who chose not to disclose metrics on board diversity fell from 37% in 2022 to 17% in 2023, while the proportion declining to provide data on senior investment professionals fell from 26% to 16%.

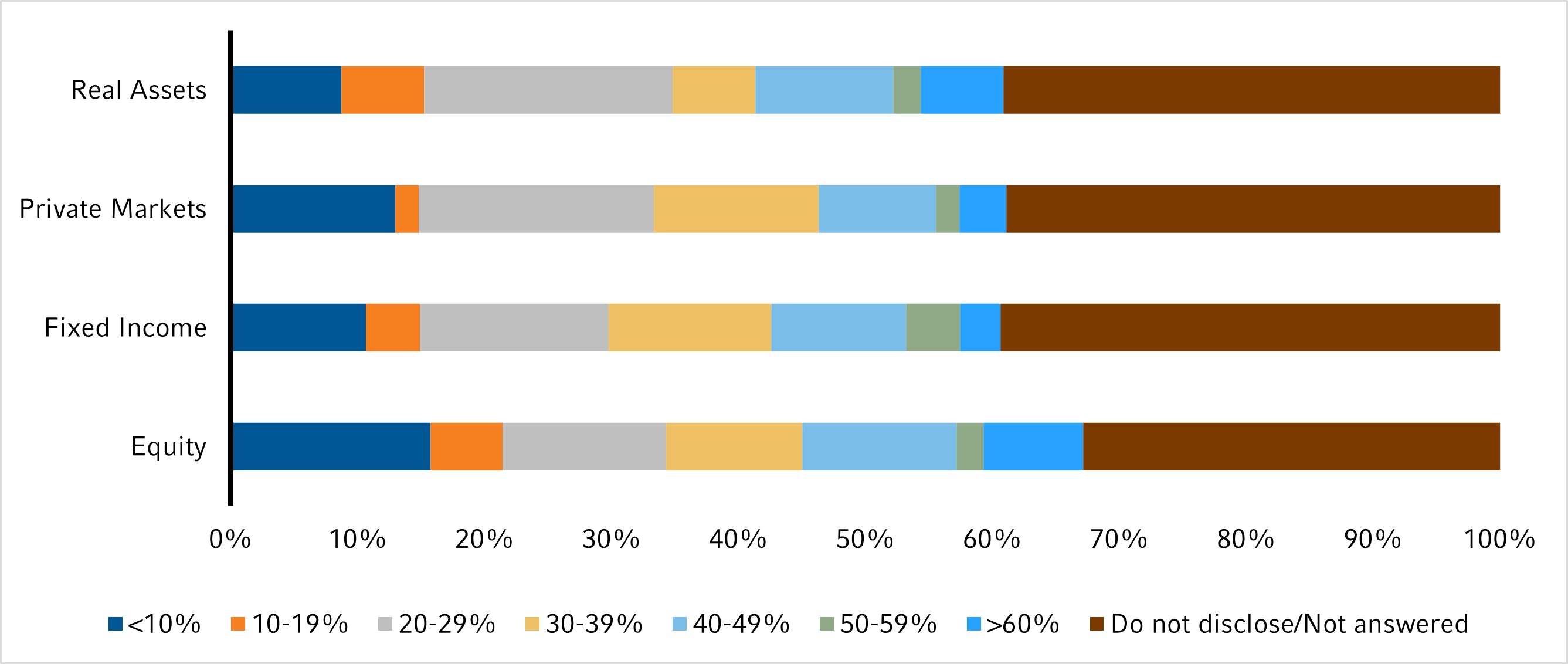

Firms offering equity strategies were the most transparent with diversity data, providing a response two-thirds of the time. In the chart below, firms that chose not to respond are represented by the brown segment of the bar chart. This answer set corresponds to a question on the level of diversity among senior investment professionals. When broken down by each asset class, we observed that firms which manage equities tended to indicate higher levels diversity (33%) than the other asset classes. However, fixed income firms were close, indicating they have 30% or greater women or minorities in their senior investor roles. Firms which indicated they offer private markets and real assets strategies trailed at 28% and 26% respectively. Firms that offer more than one asset class were counted in all relevant categories.

Ratio of women and minorities among senior investment professionals

(Click image to enlarge)

The bottom line

The results of this year’s survey indicate that despite its share of challenges, ESG investing is here to stay for the long haul. Active managers from all major asset classes continue to incorporate ESG considerations in their investment processes and hire for ESG-related roles. As climate concerns surge to the forefront, we expect ESG to only become further rooted in the investment landscape.

Up next: A blog detailing our survey results that relate to trends in active ownership.