Key China watchpoints in 2022

Is the Chinese economy on track for a soft landing?

The Chinese economy has entered 2022 on a shaky footing despite hosting the Beijing Winter Olympics, with the property market still under stress and COVID-19 restrictions still in place. We had been expecting new rounds of stimulus to support the economy, given that 2022 is a very important year politically (as Xi Jinping is likely to enter an unprecedented third term), and are encouraged that those measures have started to be implemented. That said, the data is likely to get worse before it gets better, given the lag time of stimulus—and we think that, unlike in previous periods of easing, the probability of overshoot this time around is quite small.

Stringent COVID-19 policies likely to continue hovering over China

Let's start our journey with the COVID-19 situation. China has maintained its aggressive zero-tolerance approach to combating the virus, and we have seen regional lockdowns in response to outbreaks—some of which have been in important port towns such as Ningbo. These measures have been generally successful in bringing COVID-19 outbreaks under control, which likely emboldens the government to maintain this approach.

We continue to think it's likely that the government will maintain its COVID-zero approach until the November National Party Congress. That said, though, there are two developments that are encouraging. The first is that in the latest lockdowns, the approach was far more pragmatic in imposing less-harsh restrictions on economically important areas (such as Shanghai and Shenzhen). Secondly, the recent conditional approval of the Pfizer treatment pill for COVID-19 could alleviate some of the caution at the margin (although the ability to secure enough supply this year is still in question).

Not yet out of the woods on property

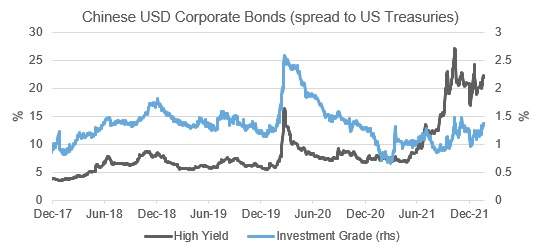

The property market has continued to show signs of stress, with property developers facing challenges with refinancing and several firms announcing an inability to make debt payments. Most recently, one of the better-placed firms, Zhenro, warned it may not be able to make a debt payment. Spreads on U.S. dollar bonds of Chinese property developers are still very elevated, and there is a substantial amount of financing that needs to be rolled over this year.

Click image to enlarge

Chinese bond spreads

It is important to remember that this process began because of government policy, driven by the desire to reduce the leverage within the property sector. We have now seen signs of concern from the government, and a number of measures have been put in place to try and stabilize the situation. Outside of general monetary easing, the most notable measure has been allowing state-owned firms to borrow money to buy the distressed assets of some of these private developers.

Fine-tuning is the name of the stimulus game this time around

We are seeing broader signs of stimulus measures coming from fiscal and monetary authorities in China. The government has emphasized the need for stability and indicated a pickup in infrastructure investment. At the same time, the People's Bank of China has reduced the amount of money that banks have to hold against deposits (therefore allowing banks to increase the amount of money in the system), and has also cut the loan prime rate (the rate on which most mortgages and business loans are built off).

We think this stimulus is more about fine-tuning, and unlike in previous stimulus periods, we see little chance of an overshoot. Our view is driven by the continued concern within the Chinese government about the level of debt in the system, and the reduced transmission of monetary policy given the softness in the property market (if property moves sideways, lower interest rates may not be enough to entice a pickup in lending).

Tech regulation an important watchpoint for emerging market equities

The big theme for emerging market (EM) equities last year was the drag from the big Chinese tech companies as they came under increasing scrutiny from the Chinese government. Emerging market equities (as measured by the MSCI Emerging Markets Index) are still experiencing high levels of consolidation, with the three big Chinese tech names (Alibaba, Tencent and Meituan) accounting for almost 10% of the index.

Despite the broader pivot to easing policy, the government has maintained pressure on these tech names. Case-in-point: In just the last fortnight, the government has ordered food delivery services (including Meituan) to reduce the fees that they charge businesses, told state-owned firms and banks to disclose relationships to Ant Group (the financial arm of Alibaba, whose IPO was cancelled last year), and there have been rumors around more regulation coming for Tencent. From a high level, it needs to be understood that Chinese authorities are keen to reallocate capital from these consumer tech names to more strategically important areas—and therefore, we believe this pressure is unlikely to alleviate.

What to expect from the National Party Congress meeting

While the focus the next couple of months will remain on the evolution of the property market and the impact of stimulus measures, it would be remiss of us not to look ahead to the 20th National Party Congress meeting that will likely be held in October. This will be the meeting where Chinese President Xi Jinping would likely take on a third term—an unprecedented move in recent history, which explains the premium being placed on economic stability this year.

One of the key watchpoints through this year and into the National Party Congress will be further clarity on how the concept of common prosperity will be implemented in China. This has become a key talking point of party rhetoric, with the overarching goal of improving income and wealth inequality. The National Development and Reform Commission has pushed back against over-promising on social welfare recently, which suggests a more pragmatic approach will be followed.¹ However, we are monitoring the situation closely, as this could pose a risk to higher-end household consumption in China (which would be a headwind to European luxury brands, which source a lot of their revenue from China).

The bottom line

After a wobbly start to 2022, Chinese authorities appear to be stepping up their efforts to stabilize the nation's economy. Recently introduced stimulus measures will likely guide China toward a soft landing, but the lag time between implementation and impact means we'll probably see weaker economic data in the months to come before improvement kicks in. Ultimately, with the National Party Congress looming later this year, we expect China's economy to be on much stronger footing by the final quarter of 2022.