2018 ESG survey

ESG manager survey: The what and the why

In August, we gave you a preview of our results, but looked exclusively at ESG survey Spotlight on integration by fixed income managers. Today, we’ve presented our results from across the board and have put the spotlight on:

• Adoption of the Principles of Responsible Investment (UNPRI)

• Implementation of responsible investment policies

• Dedicated investment professionals

• Investment process—motivation, data and research

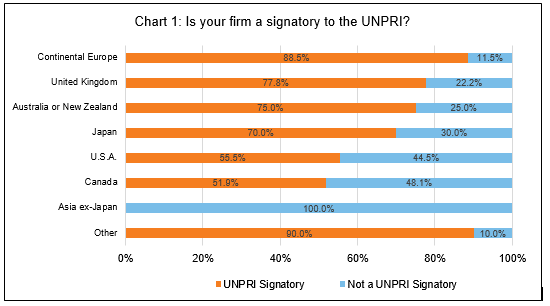

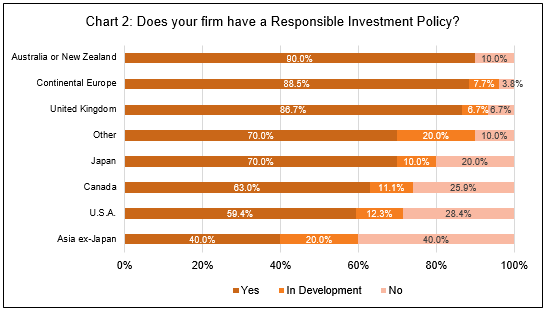

UNPRI signatories and responsible investment policies

The UNPRI (United Nations-backed Principles for Responsible Investment) are a globally recognised benchmark that actively promote the implementation of responsible investment policies. Therefore, it was important to ascertain from our survey the extent to which managers across the globe have pledged to the UNPRI and developed a responsible investment policy.

We found that the vast majority of our survey respondents are indeed UNPRI signatories and have adopted a responsible investment policy. That said, we found that this differs significantly across regions, time and assets under management (AUM).

Regional differences

As you can see in charts 1 and 2, firms based in the United States, Canada and Asia (excluding Japan) lag significantly behind peers from other regions. Even after factoring in the firms that intend to develop a responsible investment policy over the next 12 months (chart 2), firms from these countries still fall to the bottom of the pile.

Source for Charts 1 and 2: Russell Investments 2018 ESG survey

UNPRI Timeline

This trend also aligns with the timeline by which these countries signed up to the UNPRI. Over 50% of respondents in North American regions (i.e., the U.S. and Canada) only became UNPRI signatories after 2015. Meanwhile, of all respondents, the majority of firms in Japan, Australia, New Zealand, the United Kingdom and continental Europe became UNPRI signatories prior to 2015. The number of UNPRI pledges has grown rapidly since 2006 and there is a clear relationship between the date of a firm’s pledge, and the extent to which they have implemented responsible investment policies. This suggests to us that being a UNPRI signatory is now more of a hygiene factor, rather than a clear indication of actual ESG integration.

Adoption positively correlates with AUM

We also found that the prevalence of UNPRI signatories and responsible investment policies increases with the size of a firm’s AUM. Per our survey, the percentage of firms that are UNPRI signatories with responsible investment policies is twice as high in firms with an AUM greater than $500 billion USD (versus firms with an AUM less than $10 billion USD). This is likely due to larger firms having the resources—and perhaps the financial incentive—to fulfill the responsibilities required to be a UNPRI signatory and to have detailed responsible investment policies.

Investment process: Dedicated ESG professionals

AUM is the key

According to our survey, only 36% of firms have dedicated ESG professionals who spend at least 90% of their time on ESG-specific matters. On a regional scale, firms domiciled in the U.S., Canada and Asia (ex-Japan) have the lowest percentage of firms with dedicated ESG professionals versus all surveyed regions. AUM is a very strong factor in this:

• 92% of firms with AUM greater than $500 billion have dedicated ESG professionals

• Meanwhile, 91% of firms with AUM less than $10 billion do not have dedicated ESG professionals

This inverse relationship is unsurprising given the often-limited number of employees at small, boutique asset management firms compared to the largest asset managers.

Investment process: The journey to integration

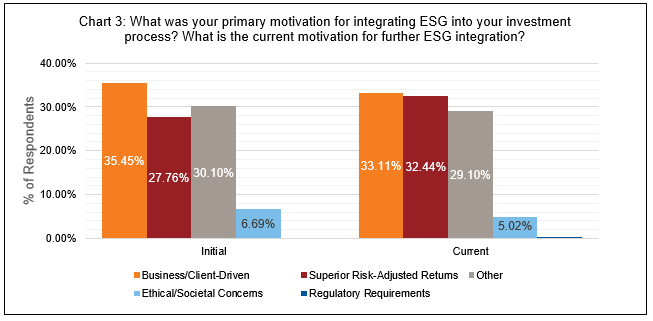

Motivation? Client demand and superior risk-adjusted returns

For 35% of firms, the primary motivation to initially integrate ESG into their investment process was business-related and in response to client demand. Meanwhile, 28% of firms were motivated by a belief in superior risk-adjusted returns.

When asked about their current primary motivation for maintaining ESG integration, the number of firms motivated by superior risk-adjusted returns increased by 4% to 32%. Business related reasons and client demand slightly decreased from 35% down to 33%. Although these shifts are small, they suggest that ESG integration is becoming slightly less business-driven and more investment-driven.

Individual ESG factors and investment decisions – Governance trumps all

When asked which individual ESG factor has the greatest impact on investment decisions, 91% of firms cited governance. However, 35% of firms claim ESG considerations dominate investment decisions only when they increase security-specific risk. Meanwhile, only 16% claim they are dominant only when they drive positive security returns. Interestingly, 49% of firms do not allow ESG considerations to dominate investment decisions regardless of their potential to increase security-specific risk or generate positive security returns.

Investment process: Data and research

Sources

Per our survey, the most common sources for ESG data and insights are ESG research vendors, direct company engagement, and company regulatory filings. The most popular ESG research vendors used by firms include, but are not limited to:

• MSCI

• Bloomberg

• ISS

• Sustainalytics.

Additional ESG research vendors cited by respondents include Trucost, Ethix, CDP, Glass Lewis, RepRisk, and Vigeo.

Use of quantitative ESG data

Progress in terms of the use of quantitative ESG data and scores in firmwide investment processes is gradual on a global scale (excluding continental Europe). In our survey, a total of 56% of firms incorporate quantitative ESG data into their investment process. Of the firms that do rely on quantitative ESG data in their investment process, 80% use a combination of both internally-produced data and externally-produced data, while 12% rely exclusively on externally-produced data.

Capital market research

When it comes to broader market insights, 31% of firms have conducted proprietary ESG capital market research to support their ESG integration efforts. Capital market research efforts decrease as firmwide levels of AUM decrease. Further to this, we found that firms domiciled in the U.S., Canada and Asia (ex-Japan) do not prioritise internal ESG capital market research (versus their more developed peers who do). These results are consistent with charts 1 and 2 above, which depict similar trends relating to geography and AUM size.

ESG integration: Geography, AUM and risk management

Geography

When looking at ESG integration by region, we found that there is a clear distinction between the extent of ESG integration across multiple geographies. Continental Europe, the United Kingdom, Japan, and Australia and New Zealand consistently compare favourably to peers in the U.S., Canada and Asia (ex-Japan), across multiple ESG resourcing and integration metrics. That said, there were indications that firms based in the U.S. and Canada are progressing towards those levels of adoption and integration. It will be important to measure the year-on-year changes in ESG integration to gain better clarity into the rate of progress for the U.S., Canada and Asia ex-Japan as they catch up to regional peers.

AUM

When considering AUM levels, firms with lower levels of AUM tend to have fewer ESG resources and less ESG integration than firms with high levels of AUM do. This is intuitive, in that investment professionals at smaller firms often wear multiple hats and have fewer employees, while larger firms have centralised resource teams that can service all products more attentively.

Risk management

When one considers the situations in which ESG factors would dominate investment decisions, it appears that firms were more concerned with ESG considerations driving security-specific risk rather than positive security returns. This suggests ESG integration is broadly viewed as a risk management exercise rather than a channel through which to generate potentially higher returns.