January FOMC meeting: A pause, but (probably) not the end of the tightening cycle

The Fed announced a pause in interest-rate increases today, stressing it will wait and see how the economy fares as the year unfolds before weighing future rate adjustments.

Leading into today’s Federal Open Market Committee (FOMC) decision, Chair Jerome Powell and a host of regional Federal Reserve (the Fed) bank presidents had unanimously expressed support for a pause in the Fed’s tightening cycle. Even perma-hawk Esther George, from the Federal Reserve Bank of Kansas City, advocated for a cautious and patient approach to monetary policy in her speech a few weeks ago.1

In a press conference today following the conclusion of the FOMC meeting, Powell stuck to the script and emphasized the Fed is waiting patiently to see how the economy evolves. The January statement removed the reference to further gradual increases, scrapped the central bank’s assessment that risks to the economic outlook are roughly balanced (hinting that they are skewing slightly to the downside now), and noted that inflationary pressures are muted. Translation: the Fed is on hold until at least June. The battery of dovish tweaks to the Fed’s guidance was enough to lift U.S. equities in the minutes following the announcement.

The cause for the pause: Downside risks

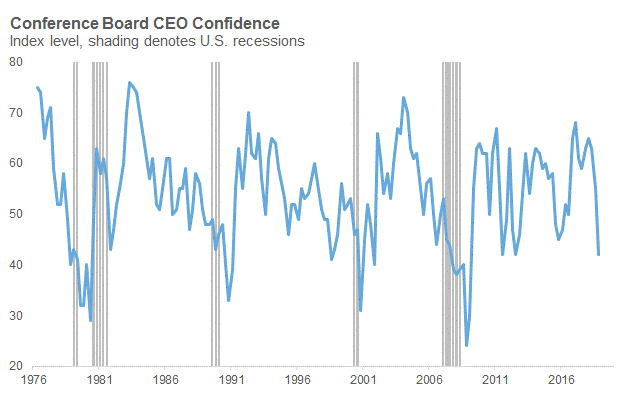

It’s important to remember that the cause for the pause is most likely about emergent downside risks to both the U.S. and global economic outlook. While the Fed still expects a strong economy in 2019, the recent volatility in financial markets, the slowing in global growth, and sharp declines in measures of U.S. consumer and business confidence have all eroded the central bank’s conviction in that baseline somewhat.

Source: The Conference Board

Source: The Conference Board

In our assessment, the catalysts for the sharp drop in business confidence and high-frequency business activity data are twofold:

- A slowdown in global economic growth rates, particularly in China, and;

- Relatedly, lingering uncertainty around the outlook for U.S.-China trade policy.

The good news? The necessary policy responses seem to be falling into place to put a floor under the global economy:

- Fed pause

As noted above, the Fed has paused its tightening cycle at a level that is arguably still slightly accommodative. - China stimulus

While China hasn’t brought out a bazooka yet, it has announced several incremental steps that collectively should help stabilize their economy at around a 6% growth pace in 2019. - U.S.-China trade policy

While the outcome of trade negotiations is still uncertain, the tone from the White House has generally grown more optimistic in recent weeks about the desire and potential for a trade deal.2 We’d stress that the speed of reaching an agreement is important when weighed against the slide in business confidence. A deal by March 1 would likely be a positive outcome for markets and the corporate sector. A kick-the-can-down-the-road solution that simply pushes the deadline beyond March would almost certainly cause business uncertainty to linger, morphing into a greater concern. A failure, coupled with a further escalation in tariffs, would likely increase the risk of a negative spiral in the global economy taking hold.

Stop talking about the balance sheet already

Markets have grown hyper-focused about the Fed’s balance sheet policy in recent months. It’s important to stress, however, that the federal funds rate is the active and primary monetary policy tool. While Powell did express some flexibility on the Fed’s balance sheet today, that flexibility is contingent on a meaningful change in economic circumstances. The way we’d translate the conditions that would warrant such a change are either:

- A recession

Historically, the Fed has cut overnight interest rates by 400-500 basis points to combat recessions. With the policy rate currently only modestly above 2%, the central bank likely will not have sufficient conventional monetary ammo to stimulate the economy in such a scenario. As such, this is one instance where we’d expect asset purchases to re-emerge and change the Fed’s course on the balance sheet. - An unwanted tightening of financial conditions

Specifically, an unexpected and unwanted spike in long-term interest rates. Since the Fed started winding down its balance sheet in October 2017, long-term interest rates have been well-behaved. That could obviously change, but thus far there is little evidence to suggest the Fed should be concerned about this channel.

The path forward

If our baseline outlook is correct—that financial markets will steady, China and the global economy will stabilize and a tight labor market, coupled with accelerating wage inflation in the U.S., will exert some further upward pressure on consumer prices—we would view today’s outcome as a pause, not the end of the Fed’s tightening cycle.

Our baseline forecast calls for one interest-rate increase later this year, likely in September. We’d stress that there’s a lot of dispersion around this projection—the Fed could cut rates if conditions continue to deteriorate, or it could raise rates up to three times this year if financial markets, the global economy and inflation all move higher in short order. Our net assessment is that the bond market has grown overly pessimistic, effectively pricing no more rate hikes during this current period of economic expansion. With that in mind, we expect the 10-year Treasury yield to gradually move up to around 3% over the next 12 months.

1 Source: Source: https://www.kansascityfed.org/~/media/files/publicat/speeches/2019/2019-george-kansascity-01-15.pdf

2 Source: Source: https://www.scmp.com/economy/china-economy/article/2184147/chinese-team-arrives-us-trade-war-talks-under-shadow-latest

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

Indexes are unmanaged and cannot be invested in directly.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2018. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.