Survey: Managers increasingly bullish on China, despite headlines

Amid nearly a year of regulatory upheaval in China across various industries, Russell Investments’ manager research team recently conducted a survey of 102 high-conviction equity managers in the emerging markets (EM), global/international, Asia and China equities space. Our survey sought to obtain manager viewpoints on the market uncertainty that has resulted - and to better understand how they are factoring in potential risks and opportunities.

The survey focused on the following key areas:

- The regulatory environment

- Earnings outlook and valuations

- Portfolio activity

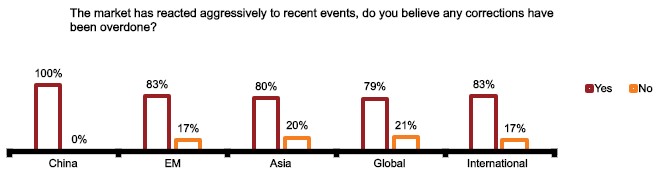

Managers largely see market reaction as overdone

While many of the managers’ responses were unsurprising, their overarching beliefs and the way they have behaved in their portfolios stand in stark contrast to the numerous media articles that have focused on negative sentiment.

The vast majority of managers surveyed indicated that the market’s reaction to China’s policy initiatives has been overdone - and that the market is over-extrapolating negative sentiment. These beliefs are backed up by more than just words, with over 50% of respondents across most regions noting that they’ve been adding selectively to their China exposure.

Click images to enlarge

Source: Russell Investments manager research team

This is no policy paradigm for experienced investors. China has often regulated its industries based on common interests of the country and long-term objectives. Contemporary examples include its anti-corruption policy initiative, reforms to its shadow banking system, curtailing online gaming for children, affordable drug pricing and greater financial market access to foreign investors. All of this aligns with the Chinese government’s vision for a less explosive but more sustainable and healthier economic growth trajectory.

While the government’s policy considerations are broad, the key focus during this period has centred around data privacy, socioeconomic considerations and national security. So far, these policy initiatives have targeted the education, internet, real estate, casino and healthcare industries (to name a few) - and have been well-documented. It’s important to note that some of the issues that Chinese authorities are addressing are not China-specific, with many other countries currently grappling with similar themes, such as anti-monopoly rules, curbing negative social practices and under-regulation of internet giants.

In addition, the National Party Congress elections taking place in 2022 are also a catalyst for a push from rhetoric to focus on social stability and balancing the interests of a more inclusive society.

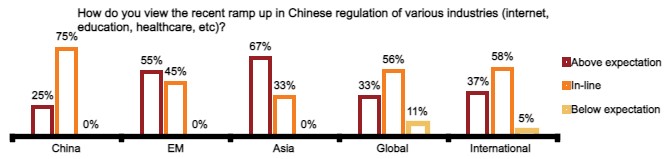

Regulatory ramp-up in-line with most manager expectations

Most China and global equity managers surveyed believe the recent changes have been in-line with their expectations, while EM managers believe they’ve surpassed what was anticipated. The key takeaway here is that most managers were surprised by the abruptness with which some of these changes were implemented, particularly in the education sector.

Click images to enlarge

Source: Russell Investments manager research team

Amid this backdrop, investors have been reassessing the ongoing regulatory risks to their investments over both the short- and longer-term, leading to their current exposure.

Importantly, while new regulations may impact the competitive landscape and, subsequently, the profitability of certain industries in the shorter term, most managers do not believe these regulations will impact the long-term attractiveness of investment opportunities in China.

Furthermore, while certain industries currently face near-term headwinds, our survey shows that many managers are looking toward long-term beneficiaries with regulatory support, i.e., electric vehicles, clean energy and high-end manufacturing. This is particularly the case for the China managers we surveyed, who are well aware of policy tailwinds and the government’s unwavering commitment to socio-economic goals, such as its five-year plans.

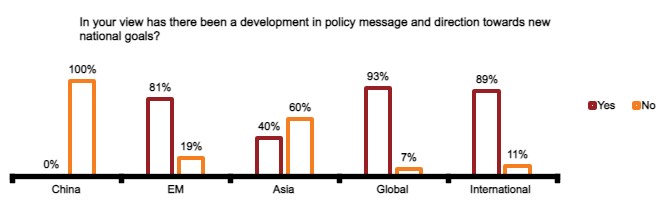

Views on China earnings and growth expectations

Responses from surveyed managers on earnings and growth expectations were mixed and largely dependent on the specific industries in question.

Click image to enlarge

Source: Russell Investments manager research team

This is consistent with managers’ expectations on how the current regulatory environment will drive changes in capital expenditures (capex) - both foreign and local. It’s also worth noting that many industries impacted by regulation so far have not been associated with more capital-intensive sectors, and therefore don’t expect significant drops in capex levels.

Click image to enlarge

Source: Russell Investments manager research team

Importantly, China has been working toward opening its capital markets to foreign investors. Because of this, government leaders are mindful of not undoing what they have set in motion over the last few years, as they understand the importance of credibility and would unlikely want to spook and derail investor expectations much further.

China manager insights

By and large, local China equity managers are repositioning their portfolios toward industries with policy support, such as hard-technology-related sectors, including electric vehicles, clean energy and high-end manufacturing.

- There is an expectation that capex in these sectors, as well as in semi-conductors, will continue to increase - and that there will be further consolidation.

- Managers also anticipate that spending will continue to increase as China enters a new industrial- and technology-upgrade cycle.

China’s transition from planned economy to market economy has been happening for some time, and while the direction is irreversible, a pause or pull-back under certain market conditions can be expected from time to time. Managers see long-term opportunities, however, as remaining intact.

Meanwhile, the country’s long-term consumption upgrade trend remains unchanged. If anything, addressing the imbalance in wealth and opportunity should increase broader and healthier overall consumption levels rather than reduce them. Amid this backdrop, some managers have increased earnings and growth assumptions, with the expectation that the cost of living will come down. In the short-term, however, they expect consumption and healthcare to continue to be under pressure.

The China managers we surveyed were also largely of the belief that the Chinese market is oversold on internet giants, and that multiple compression will remain intact with high earnings growth. They also agreed that onshore consumer staples remain expensive, that the bulk of policy risks are concentrated around the internet, education and healthcare sectors, and that education companies with no exposure to K-12 are oversold. They also feel likewise for certain gaming stocks where the targeted under-18 age group is a marginal contribution to earnings. Our survey also showed that equity managers continue to increase exposures to China A-shares.

The bottom line

The results of our survey suggest that a notable disconnect exists between the sentiment conveyed in recent articles on China and the sentiment expressed by equity managers. Ultimately, while managers see both opportunity and risk amid the country’s ongoing policy initiatives, they remain largely bullish over the long-term.