The good, the bad and the alternative

With the current late cycle market environment, investors are becoming more and more interested in seeking returns from non-traditional assets. This article discusses where to find value in unlisted assets and how to avoid the tripwires.

With the current late cycle market environment, investors are becoming more and more interested in seeking returns from non-traditional assets. Samantha Steele, Russell Investments’ heads up private market strategies for EMEA, with18 years experience working in Australia and the UK covering Asia Pacific and European markets, tells how to successfully invest in unlisted assets and shares where Russell Investments is seeing value in the sector.

Why invest in private markets?

At Russell Investments, we define private markets as real estate, infrastructure, private equity and private debt. We can blend these strategies together or alternatively we run specialist calve out strategies, for example a global real estate strategy.

We see that there are four reasons why you should consider investing in private markets:

- Potential for superior returns to traditional asset classes. We see that there is a liquidity premium of around 200-300 basis points above comparable listed assets, which is obviously a substantial opportunity. This compensates investors for the complexity, illiquidity and lack of transparency that comes with private market investing.

- Alternatives can also provide a hedge against inflation, and this is particularly true for real estate and infrastructure.

- Lower correlation with other asset classes. We have found that alternatives don’t have the volatility that occurs on listed markets. One reason is their higher illiquidity but the other is also due to the appraisal process that we have in the private markets, which means assets aren’t susceptible to the big swings that occur in the private market.

- Diversification. Private markets provide a significant amount of diversification and exposure to asset classes and strategies that you can’t get exposure to through the listed market.

From my experience investing in private markets, also referred to simply as unlisted assets, there are some key tactics that help to enhance returns and minimise risk, including:

Take an active approach

When investing in private markets, you can often get much closer to the underlying asset than when you are investing in listed markets, and this provides an opportunity to influence returns, but only if you take an active approach.

It’s like lifting up the bonnet of the car, making some adjustments to the engine, and ensuring that vehicle can go a lot faster than it would if you were just sitting in the back of the car complaining that you aren’t going fast enough.

For example, we sit on a number of investment advisory meetings for underlying funds through which we invest in private markets. This allows us to get increased transparency from the fund but also input to approving / opposing issues such as conflicts of interests.

At the asset level, there is more opportunity to drive operational returns when compared to listed assets, but again you need to be active. For example, if you are buying an office building where you’ve got 60% vacancy, you can actively enhance the returns by repositioning that asset through refurbishing and lease up that space and therefore enhance rents, income security and improve overall capital returns.

Work the informational advantage

Investing in private markets is opaque and not transparent in comparison to public markets, there is the ability to gain informational advantages. This is a particularly important for sourcing deal flow and we invest with managers that take the approach to acquire assets off-market, avoiding the auction process and therefore enhance the entry pricing, as these investments can sometimes secure deep discounts to open market value.

Manager selection is crucial

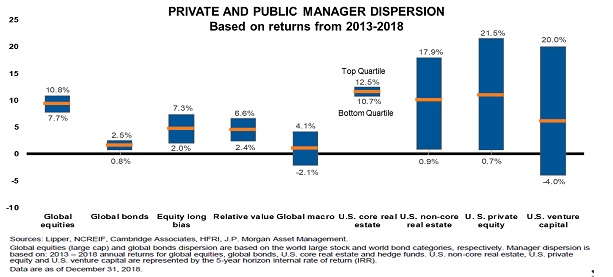

In the private markets, there is a large dispersion between top quartile and bottom quartile managers, reflected in the deviation around the median manager’s performance, so manager selection is crucial. As you can see from the chart below, the disparity is much greater for unlisted assets than listed assets, with the exception of US core real estate, which is in many ways more akin to a listed asset because of its higher level of transparency, liquidity and benchmarks.

First time investors going into this space need to understand that there is a much biggest dispersion between manager returns in private market investing versus public market investing. We would strongly suggest that you use an expert to undertake these strategies for the first time.

So, where are the best opportunities in unlisted assets at the moment?

In private equity, small is good - beware of heightened competition with buyouts near record prices

Slowing investment activity, paired with strong fundraising and exit activity has resulted in a “mountain” of capital to be deployed, causing a pickup in competition for assets.

The fund raising side of the private markets continues to be dominated by mega buyout funds. We have looked at these strategies and prefer playing below the radar, looking at smaller to mid-sized strategies. This allows us to more nimble compared to the mega funds.

With buyouts at record pricing, you need to be selective. While we have seen strong multiples, we expect multiple expansion will be less from current levels, and therefore we prefer smaller companies own by niche managers who can apply their industry and subject matter expertise to drive value through operational improvements rather than financial engineering.

One thing to be aware of in this market, particularly when there is a lot of competition and a focus on acquiring assets quickly, is that investors can lose focus on the details. It’s important that deals aren’t pushed through on loser terms. This is where a lot of trip ups can happen. You still need to have the proper covenants, due diligence and detailed documents in place, so don’t compromise on any of those.

Private debt – plenty of opportunities but be selective

Private equity is a long-established asset class and now we are seeing private debt moving in the footsteps of private equity. The macro trend that we’ve seen over the last 20 years has been that banks are providing a smaller proportion of loans, largely due to regulatory changes.

Private lenders have been filling the gap. Why? Firstly, private debt is seen as an alternative to investing in banks and financials. Secondly, investors see private debt as a similar risk profile to fixed income but also with a higher yield potential.

So, what are the tripwires in this relatively new sector? While senior loans rank above mezzanine debt and then above equity when a company is wound up, it is important to be aware that not all senior loans are equal, and the level of security makes a real difference with risk and return. Private debt is very specialist and the ability of the manager to evaluate the credit risk of the borrower is critical.

What do we like at the moment in private lending? We are focused on asset backed strategies over pure cash flow based lending, and senior secured finance versus junior credit.

Despite the headlines about high real estate prices, we are still finding significant value in the sector. Yield compression has been fuelled by central bank liquidity and low interest rates, and this compression is now slowing. However, we are still achieving premiums over bond rates and in most markets, we are still above the 10-year average, particularly in Asia and Europe.

The occupier market is still fairly healthy, and we are seeing this further backed by capacity constraints in the market. The rising cost of construction is impacting the supply pipeline and helping reduce vacancy but it is also helping increase rental growth.

We are placing more of a preference on debt strategies than we are on equity. We think there is an attractive premium available from debt and from a cycle context it makes more sense.

On the core real estate side, you do have to be very cautious. We are finding that core real estate is very expensive at the moment. With real estate equity investments, we continue to value-add / develop-to-core strategies due to the option to enhance income and improve capital growth potential. Our approach across all of our private market strategies is to target small, niche managers, accessing small to mid-sized deal flow in these markets - deals that are just off the radar for the big investors.

This is an approach that needs some work that not all investors can do themselves. That’s where you need to partner with a specialist. We’ve partnered with managers that have an expertise in taking an unloved asset, improving it and selling it on to the core market where there is wealth of buyers.

Infrastructure: Global energy transition a great opportunity

In infrastructure, we are finding the core market quite expensive. Where we do see a great opportunity is in the global energy transition sector. This is an emerging new class of infrastructure that we need to be more aware of.

What is creating this new asset class? Firstly, there is increasing awareness of environmental issues and global warming, which have changed consumer preferences.

Secondly, there is improved cost competitiveness of renewable infrastructure – for example solar energy has come down 70% in the past decade. The National Renewable Energy Laboratory estimates that wind and solar costs could fall another 20-40% between now and 2030.

Another factor is the rising popularity of electric vehicles and falling battery costs, which has really opened up the potential for energy storage. The International Energy Association expects the global electrical vehicle fleet to grow to about 30% between 2030 to around 125 million.

From an access point, we wouldn’t suggest buying existing renewable assets as we seem limited upside and pricing concerns. We think the way to create value is by partnering with a manager that is creating these investments, so you are going in from a position of building out this product for the market.

The bottom line

Private market investments can diversify risk, generate alpha and provide cash flow. There are plenty of opportunities as the moment but it’s important to watch for the tripwires such as covenant light private equity deals. Manager selection is critical and there is a large dispersion between top quartile and bottom quartile managers. There are a lot of complexities associated with investing in private markets – regional differences, illiquidity, lack of transparency – therefore we suggest using an expert to build up these portfolios to get better outcomes.

Important information

Issued by Russell Investment Management Ltd ABN 53 068 338 974, AFS Licence 247185 (RIM). This document provides general information only and has not been prepared having regard to your objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation or needs. This information has been compiled from sources considered to be reliable, but is not guaranteed. This document is not intended to be a complete statement or summary. Copyright © 2019 Russell Investments. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments.