Time to focus on China

From trade wars with the U.S., to the widely publicised slowdown in gross domestic product (GDP) growth, China has rarely been out of the news in the past 18 months. Unfortunately, those taking the headlines at face value may be missing out on long-term opportunities available within this economic powerhouse.

Increased inclusion of China A shares in global indices

Broad domestic opportunities now available

For investors, the importance of Chinese equities continues to grow, with the recent announcement that index provider MSCI will increase the number of domestic shares included in its flagship Emerging Markets (EM) Index.1 The move will gradually increase the inclusion factor of MSCI China A large cap securities (companies listed on the domestic Shanghai and Shenzhen exchanges) from the current 5% inclusion to 20% of their respective free-float adjusted market capitalisations.2

Upon completion, 253 large- and 168 mid-cap China A shares will be included within the MSCI EM Index, at an anticipated weighting of 3.3% in the index by November, a significant move from the current 0.71%.3 However, after the initial inclusion in June 2017, this barely scratches the surface of the broad domestic opportunities available in the world’s second-largest economy.

Recent market performance driven by trade

2019 has seen a rebound in investor sentiment

Chinese equities endured a tough 2018, ending the year as the worst performing equity market on a global basis. A risk-off environment was driven by inflammatory trade negotiations with the U.S. and fears of a growth slowdown. At the end of the year, sentiment indicators on domestic Chinese equities markets in particular were pointing to oversold territory.

However, 2019 has seen a rebound in investor sentiment. As of mid-March 2019, the MSCI All China Net Index is one of the world’s best-performing equity markets with the domestic market, as measured by the CSI 300, up +27.4%.4 Positive trade news drove expectations of a trade agreement while foreign investors have been drawn to the relative attractiveness of the market in terms of valuations relative to history.

Attractive opportunities for active stock pickers

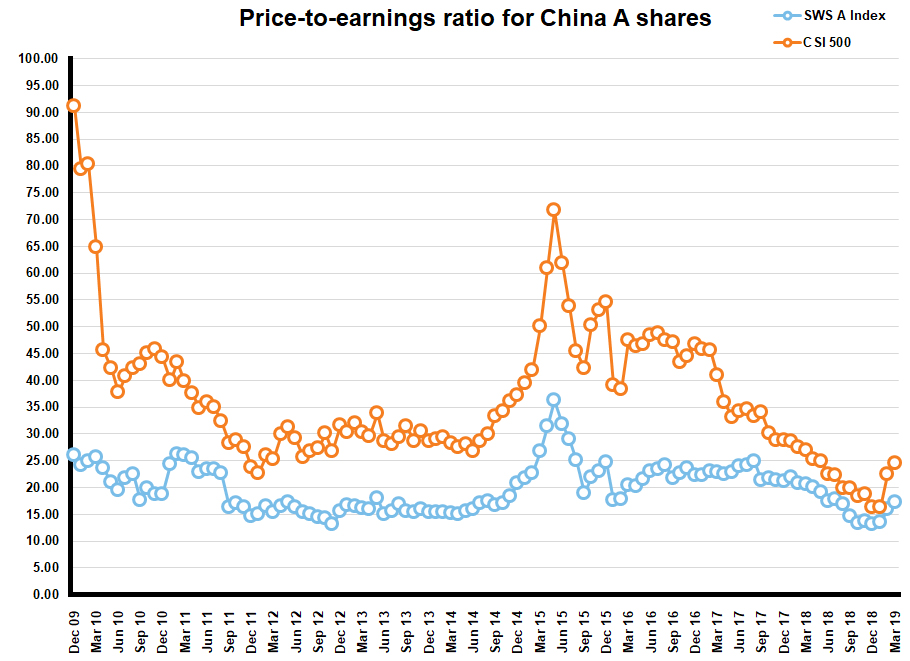

Despite the recent market rebound, the built-in panic of late 2018 created mispricing opportunities that are still present in the market for skilled investors to unveil. The A share market currently has a low price-to-earnings ratio compared to its recent history, as shown in figure 1. The broad-based SWS A Index (which combines both Shanghai and Shenzhen domestic exchanges) is trading at 17.1 times earnings, while the CSI 500 index trades at 24.5 times, as evident in figure 1.

Figure 1:

Source: Wind. Data as at 21st of March 2019.

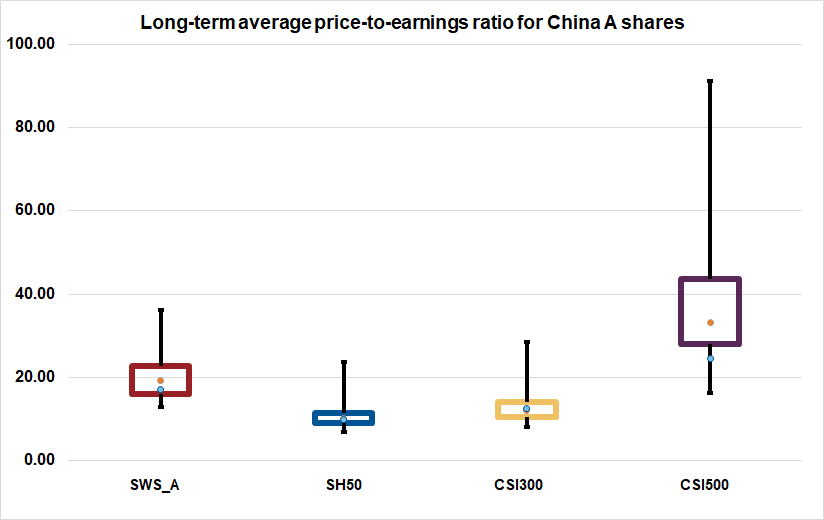

Figure 2:

Source: Wind. As at 21st March 2019.

As we can see in figure 2, the market’s long-term average valuation (orange dot) remains above current market valuations (blue dot) in the SWS A and the CSI 500 index. On a sector basis, active stock pickers focusing on domestic consumption themes are benefiting from attractive valuations, particularly among under researched small and medium-sized companies.

Structural domestic growth: A long-term opportunity

Investors looking for long-term growth should be attracted by including China A shares in their portfolios as a way to broaden the investment opportunity set with a market still exhibiting strong potential for economic growth.

Diversification and low correlation with other equity markets

The main source of China exposure for investors today will be through EM portfolios, which is gained predominantly from investing in companies listed in Hong Kong and the U.S. These are heavily dominated by financials and technology related stocks. In contrast, the composition of the onshore market is much more diversified and offers a direct route to tap into the domestic structural growth story through the greater depth and breadth of the consumer staples, consumer discretionary and health care sectors. The sheer size of the onshore market – larger than the UK and Japanese markets combined, with a $7.7 trillion market capitalisation5 – provides diversification benefits for global investors with its relatively historic low correlation to other equity markets.

Expected growth rate remains superior

We acknowledge China’s economic growth is slowing as it continues on the path from a manufacturing-based economy to a consumer, services and technology-led economy. Nevertheless, its expected growth rate remains far superior to developed and total EM expectations. While its population demographic may not be as favourable as other Emerging Markets such as India, China has over 400 million millennials. This is five times the number within the U.S.6

The central government responded to last year’s slowing domestic consumption through supportive policy measures such as VAT and personal income tax reform. This notably included the largest tax cut package in the country’s history announced in October 2018. Such fiscal stimulus is anticipated to have a significant impact on middle class consumption in particular, contributing to the government’s likelihood of reaching its 6.0%-6.5% growth target for 2019.

Increased Environmental, Social and Governance (ESG) awareness in China

Early investors in China have always paid close attention to the governance of the companies they invest in and continue to do so.

Corporate governance improvements

More broadly, we are beginning to see corporate governance improvements across the market. For example, 763 A share listed companies voluntarily provided a corporate social responsibility report in 2016.7 The emphasis on ESG issues is also on of the agenda of the central government and the regulator. In June 2017, the domestic Securities Regulatory Commission introduced requirements for all listed companies (and bond issuers) to disclose the ESG risks associated with their operations in their annual or semi-annual reports from 2020.8 Meanwhile, a newly revised “Code of Corporate Governance for Listed Companies” was issued in September 2018 which clearly requests companies to establish ESG requirements including areas such as green development, targeted poverty alleviation and strengthening of audit committee functions.9

While this remains at a very early stage, it is positive to see an emerging market take a proactive approach to these issues.

Do you have a sufficient allocation to China A shares?

There are always risks to investing in emerging markets equities and, like any market, the Chinese economy does face internal and external headwinds. However, there is the safety of margin in current valuation levels and investors should take a long-term view when evaluating investment opportunities. The key question asset owners should ask themselves is: do you have a sufficient allocation to China A shares?

1 https://www.msci.com/index-announcements, 28th February 2019.

2 As above

3 As above

4 Source: Bloomberg. As at 21st of March, 2019. CNY terms.

5 Shenzhen and Shanghai Stock Exchanges. As at February 28th, 2019.

6 https://daxueconsulting.com/infographic-millennials-spending-habits-chinese-vs-american/

7 http://www.fundsglobalasia.com/june-2018/esg-china-gets-serious-about-esg

8 http://www.cciced.net/xwzx/hfyw/201706/t20170614_93987.html

9 http://www.glasslewis.com/regime-change-begins-at-home-chinas-new-governance-code/

or http://www.csrc.gov.cn/pub/zjhpublic/zjh/201712/t20171229_329873.htm