2017 Value of a fiduciary adviser: more than 4%

We’d like to share an article our colleagues in the U.S. have recently published relating to the often under rated value of an adviser. We recognise that the advice that you give to your clients makes a real difference to their futures; to that end we’d like to help you shape those futures further by giving you the tools you need to succeed.

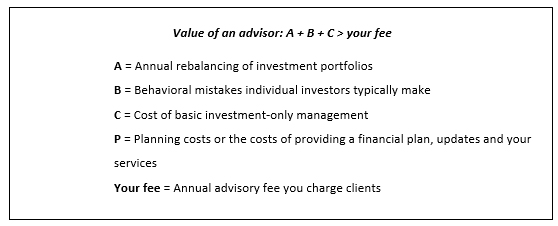

The Value of an advisor

Updating our annual “Value of an advisor” study for 2017 seems especially relevant given the spotlight that the DOL fiduciary rule has shone on all manner of fees in recent months. Regardless if the fiduciary rule is materially changed or not during the current delay, the fact remains that fees – and the value clients derive from them – are forefront in investors’ minds today. And yet, as in the past four years of this study, we have concluded that the value an advisor delivers to their clients materially exceeds the 1% fee they typically charge for their services.

Eight consecutive years of strong U.S. stock market performance (Russell 3000® Index) no doubt contribute to some of the popular skepticism about the value of advisors. When virtually all stocks are rising, it doesn’t seem hard to throw together a winning portfolio. However, that view completely overlooks the fact that the value advisors deliver rests in many places – not only investment selection. In fact, standard investment selection has arguably become one of the least valuable parts of an advisor’s value.

Instead, the technical and emotional guidance that only a trusted, human advisor (as opposed to robo-advisors, for instance) can offer to investors who are attempting to undertake the complex job of coordinating the accumulation, distribution and transfer of their wealth, is invaluable – particularly in an environment that is likely to deliver lower returns and higher volatility than investors have grown accustomed to recently.

Of course “invaluable” is a difficult sum to bill a client for, though, so at Russell Investments, we have attempted – this year again – to estimate the value of an advisor. In 2017, we assess the value of an advisor to be approximately 4.04%.

Here’s how we arrived at that conclusion.

The value of an advisor in 2017

(Note: Our estimates are based on a $500,000 advisory portfolio.)

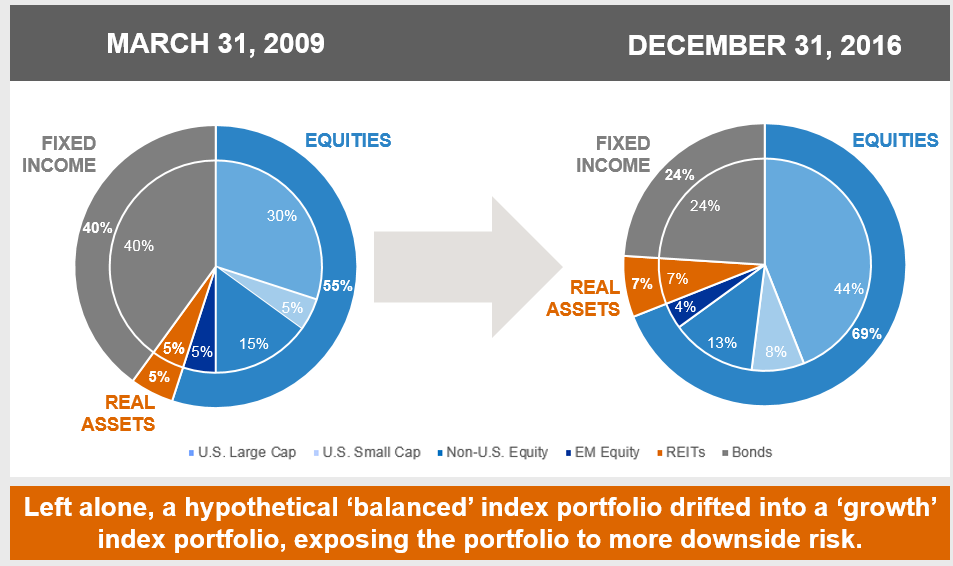

A = Annual rebalancing of investment portfolios

Particularly in periods of rising markets, it can be easy to underestimate the value of a disciplined rebalancing policy. But that’s a mistake. As the chart below shows, a hypothetical balanced index portfolio that hasn’t been rebalanced to policy weights since the bottom of the Great Financial Crisis on March 9, 2009 would look more like a growth portfolio today, exposing the investor to more risk than initially agreed upon.

U.S. Large Cap: Russell 1000® Index; U.S. Small Cap: Russell 2000® Index; Non-U.S. Equity: Russell Developed ex-U.S. Large Cap Index; REITs: FTSE EPRA/NAREIT Developed Index; EM Equity: Russell Emerging Markets Index; Bonds: Bloomberg U.S. Aggregate Bond Index. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

Regular rebalancing has the potential to add value – to the tune of 0.2% in additional return and 1.6% of risk reduction, as shown in the table below.

Hypothetical rebalancing comparison: Jan. 1988 – Dec. 2016

| Buy and hold | Annual | Quarterly | Monthly | |

| Annualized return | 8.6% | 8.8% | 8.6% | 8.5% |

| Annualized standard deviation | 10.4% | 8.8% | 8.9% | 8.9% |

For illustrative purposes only. Not meant to represent any actual investment. Methodology available in notes at the end of this blog post.

An additional 0.2% in return may not seem like much at face value. But, compounded over a multi-year period, it can quickly add up. Consider a hypothetical $100,000 investment. An annualized 8.6% return over 30 years would growth the initial $100,000 to $1,188,214. An additional 0.2% in return (so, an annualized 8.8% return instead of an 8.6% return) would yield an ending amount of $1,255,645. That’s a $67,431 difference. It just goes to show that small numbers, even after the decimal point, can make a big difference.

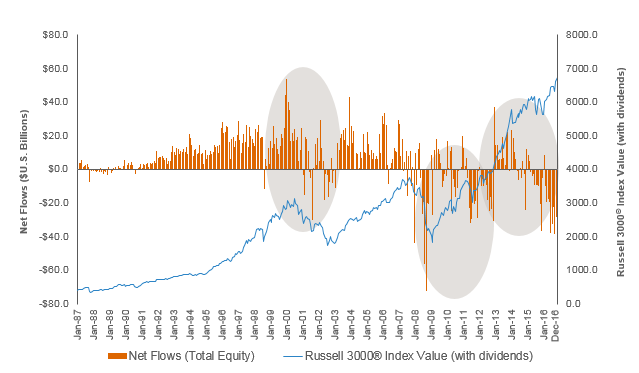

B = Behavioral mistakes individual investors typically make

Although advisors don’t typically include “behavior coach” in their job description, it’s most likely the single largest contributor to the total value they bring their clients. Left to their own devices, many investors will “buy high” and “sell low,” as the chart below illustrates.

Investors look for patterns in the stock market

Data shown is historical and not an indicator of future results.

Source: Industry flows into equities. www.ici.org/research/stats. Russell 3000® Index: www.ftserussell.com (“value with dividends”). Data as of December 31, 2016. Index performance is not indicative of the performance of any specific investment. Indexes are not managed and may not be invested in directly.

From 2009 to 2013 investors withdrew more money from U.S. stock mutual funds than they put in (see the orange bars). Unfortunately, the stock market (the blue line) steadily climbed – to the tune of 16.1%, based on the Russell 3000® Index from 12/31/2009 to 12/31/2013 – during that time. Those investors who have chosen to stay in cash since the market bottom on March 9, 2009 to the end of 2016 fared even worse: they forewent a cumulative return of 300%, based on the Russell 3000 Index.

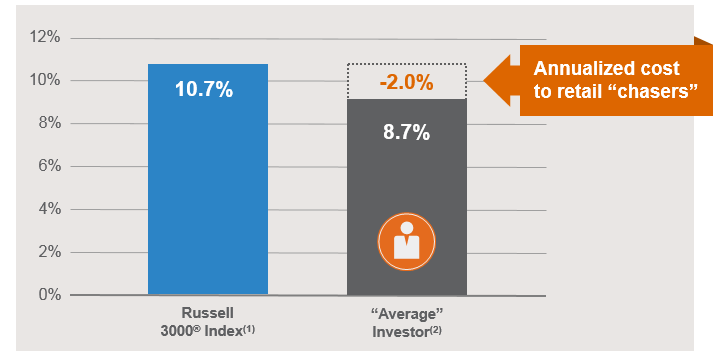

What impact might this type of behavior have on the “average” equity investor’s portfolio? The chart below tells all.

The high cost of investor behavior

(1984-2016)

(1) BNY Mellon Analytical Services, Russell 3000® Index annualized return from January 1, 1984 to December 31, 2016.

(2) Russell Investment Group & Investment Company Institute (ICI). Return was calculated by deriving the internal rate of return (IRR) based on ICI monthly fund flow data which was compared to the rate of return if invested in the securities of the Russell 3000® Index and held without alteration from January 1, 1984 to December 31, 2016. This seeks to illustrate how regularly increasing or decreasing equity exposure based on the current market trends can sacrifice even market like returns.

Indexes and/or benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

Left to their own devices, the average stock fund investor’s inclination to chase past performance cost them 2% annually in the 32-year period from 1984-2016. In that sense, an advisor’s ability to keep their client stick to their long-term financial plan, and thereby skirt irrational, emotional decisions, is worth 2.0%.

C = Cost of basic investment-only management (aka, robo-advisors)

What should an advisor who delivers investment-only management and no financial plan, no ongoing service, no guidance, nothing except for an annual statement, online access and a phone number to call in case of questions charge their clients?

Robo-advisors have set that price at approximately 0.33%.1

P = Planning costs and ancillary services

As part of a fee-based relationship, advisors add value by building and regularly updating a custom financial plan for each client and conducting regular portfolio reviews. Many also offer ancillary services, such as investment education, assistance with annual tax return preparation, Social Security and retirement income planning, as well as one-off custom requests from clients—all of which could cost thousands of dollars if purchased à la carte.

How much does the financial planning component cost nowadays? Per a recent Financial Planning Association’s (FPA) study2, the cost of developing and building an initial financial plan is coming in at around $2,600 on average (which includes the cost of the advisor spending up to 13 hours interviewing the investor as a basis for the plan). Planners now typically charge an hourly rate of approximately $200 per hour for ongoing monitoring and updating of the plan.3

By providing a financial plan with ongoing goal and risk tolerance monitoring, the value of both the initial plan and ongoing adjustment are worth approximately of 0.50% on a $500,000 account. (In our example here, we assume that creating and maintaining the financial plan are part of the annual advisory fee.)

What is the value of typical ancillary services an advisor and their staff offer? Advisors and their staff consistently underestimate the value of the ancillary services – time saving and peace of mind during tax season, in preparation for retirement, custom requests and questions – they may provide their clients. These additional services can quickly consume 20, 50, or 100 hours each year. I estimate that value at 0.25% (assuming these are part of the annual advisory fee).

The bottom line

What is your true value as an advisor in 2017? If you are delivering all the services and value beyond the cost of investment-only advice, then the value of your services individually may be:

| (A) Annual rebalancing | 0.20% |

| (B) Investor behavior | 2.00% |

| (C) Cost of basic investment-only management | 0.33% |

| (P) Planning costs & ancillary services | 0.75% |

| Total 2017 value of an advisor | 3.24% |

For illustrative purposes only.

For many advisors this means that the value they deliver is worth more than the fee they charge their clients. Clearly, investors stand to benefit from such a trusted relationship with an advisor – particularly at a time of record high U.S. equity markets and likely rising interest rates. At the same time, advisors also stand to gain from relationships with satisfied clients in today’s competitive landscape of margin compression, regulatory scrutiny and demographic change. After all, satisfied clients are likely to be persuasive advocates for the advisor, repaying the advisor with worthy referrals that can potentially help enhance the value of the advisory firm.

Please be advised that all links within this article take you to our US site where regulation may differ.

MCR-2017-06-22-0277

1 Based on the average fee charged for investment-only management by 10 robo advice offerings for a client portfolio of $500,000 as accessed on the companies’ websites on 3/7/2017.

2 FPA Research & Practice Institute, “Financial Planning in 2015: Today’s Demands, Tomorrow’s Challenges.”

3 FPA Research & Practice Institute, “Financial Planning in 2015: Today’s Demands, Tomorrow’s Challenges.”