2021 Annual ESG Manager Survey: The red flag is raised on climate risk

Our annual ESG manager survey of active managers assesses the integration of ESG considerations in investment processes among equity, fixed income and private market managers and spotlights firmwide policies, use of data, engagement and integration.

Climate risk takes front and centre stage

This year marks our seventh annual ESG Manager survey. The annual survey has evolved over the years, enabling deeper insights into trends and into how attitudes toward responsible investing have changed since it launched in 2015. A total of 369 asset managers from around the world participated in our 2021 ESG Manager Survey, representing $79.6 trillion assets under management. Our dedicated research shows that asset managers are increasing efforts to improve the overall quality of inputs when integrating ESG considerations. 55% of the respondents now have dedicated ESG professionals, compared to 43% in the previous year.

The survey participants have a broad representation by asset size, region and investment strategy offerings. Of the 369 participants, 293 offer equity strategies, 208 offer fixed income strategies, 113 offer private markets strategies and 94 offer real assets strategies. 56% of the respondents are headquartered in the U.S., 15% are based in the United Kingdom, 9% are based in Continental Europe, with the remainder located in other regions. 34% of the respondents have assets under management less than US$10 billion while 30% of the participants have over US$100 billion in assets.

In this short summary of the 2021 survey findings, we take a look at the following key findings:

- How managers are integrating ESG

- ESG-specific consideration by asset managers: UK managers lead the way

- Which ESG considerations drive decision-making

- Spotlight on active ownership

- A growth in ESG product offerings

- Screening rises in prominence

- Climate risk: The greatest issue flagged by asset managers’ clients

- Will COP26 further drive the focus on climate risk

How managers are integrating ESG

We continue to observe commitments to sustainability-related initiatives across the asset management industry. This is driven by an increase in regulatory standards, an accelerated focus on climate change and a shift in perspective, particularly in social considerations in light of COVID-19. In order to provide deeper analysis into this trend, we asked survey participants to identity sustainability-related organisations and initiatives that they are engaged with.

The results reveal that of the 369 survey participants, 80% are signatories to the United Nations-supported Principles of Responsible Investment (PRI), compared to 75% from the 2020 survey, 72% from the 2019 survey and 64% from the 2018 results. We launched our ESG Manager Survey in 2015 with fixed income managers. Our analysis shows a notable increase in PRI signatory status amongst those managers, from 52% in 2015 to 89% in 2021.

Other prevalent initiatives include supporting the Task Force on Climate-related Financial Disclosures (TCFD), collaborating with the CDP (formerly the Carbon Disclosure Project) and Climate Action 100+ signatories. Additionally, the Net Zero Asset Managers Initiative is rapidly gaining momentum. A number of firms have an extensive list of involvements and advisory roles with initiatives, such as climate change-related, regional-based organisations and stewardship codes.

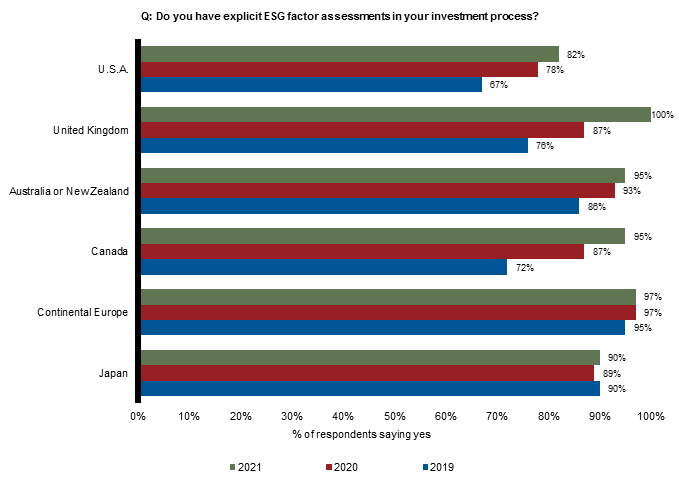

ESG-specific consideration by asset managers: UK managers lead the way

In order to incorporate ESG considerations, we believe that it is critical to conduct explicit ESG assessments in the investment process on a regular basis. We observe whether asset managers have additional inputs specific to ESG-related topics, which are often non-traditional or non-financial-metric-driven considerations. 82% of the respondents said they incorporate explicit qualitative or quantitative ESG consideration assessments at the corporate or sovereign level systematically in their investment process, compared to 78% in 2020. The below exhibit illustrates the year-over-year changes by region, highlighting that the highest percentage increase came from firms based in the U.K, with the most improvements seen among smaller firms, likely due to the local pressure from the client base and regulation.

Click image to enlarge

Which ESG considerations drive decision-making?

The broadening of ESG-related information available in the marketplace is highlighting the materiality risks associated with ESG, enabling further adoption of the integration of ESG. However, despite the increase, the extent of the role that ESG assessments play in actual investment decisions remains unclear - especially around environmental and social considerations. To gain further clarity, we first asked which ESG considerations impact the investment decisions the most. Each year, governance remains the dominant factor. This is no surprise, given that company management is a critical component in generating long-term enterprise value. When asset managers are considering each of the ESG elements, they need to consider the materiality of each consideration, and materiality differs by industry. For example, environmental aspects might be important for the energy or utility sectors but less important for the banking sector. However, overall corporate governance – how companies are managed – applies to all companies, regardless of industry. That being said, we have noticed a reasonable increase in environmental considerations, when compared to previous years’ responses. This is likely due to the increased awareness and desire among market participants to tackle climate risk, which could impact asset prices over time.

For those who selected environmental as the most important consideration in their investment decisions by region, we see a sizeable increase among managers who are based in Continental Europe. This steep rise in environmental considerations is in line with the recent introduction of the EU’s sustainability regulations and provides further proof that regulations can drive significant industry practices.

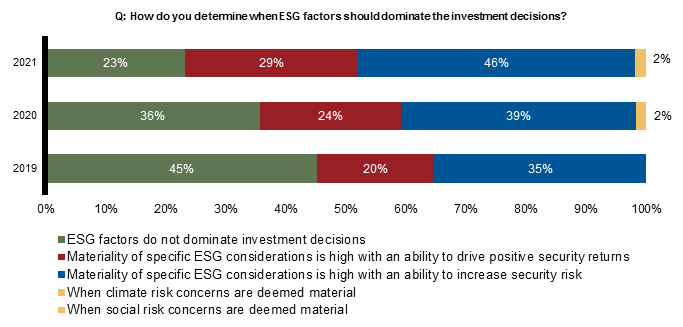

We asked managers when ESG considerations should dominate investment decisions (outside of investment guideline considerations). The results show that financial materiality is a focal point for the decision-making process. 75% of the respondents claim to incorporate specific ESG considerations when the materiality is high, versus 63% from the previous year. An increased number of respondents incorporate ESG considerations into investment decisions when there is a potential impact to security risk generated from higher material considerations. This response suggests that more asset managers treat the evaluation of the impact of ESG considerations as a risk-management exercise. Interestingly, climate risk concerns in isolation have little influence on the majority of managers’ overall investment decisions. We believe that this is because asset managers are mostly evaluating the materiality of ESG considerations - climate risk is a part of that - instead of climate risk being the sole driving factor.

Click image to enlarge

Spotlight on active ownership

Asset managers continue to increase their engagement activities. This includes engagement with underlying companies and governments, in order to influence entities’ potential outcomes, such as greater transparency, improved behaviours and reduced uncertainty and risk. 90% of the respondents include ESG discussions in meetings with senior management of the companies they invest in. 35% of the respondents claimed they always include ESG discussions, compared to just 21% in the 2018 survey response. Conversely, the respondents who rarely or never include ESG discussions declined to 9%, compared to 20% in 2018. The survey results suggest an increasing trend of engagement activities becoming a prominent component in investment activities.

The survey also indicates that engagement activities increased, even among fixed income managers, where 92% of fixed income managers regularly engage with underlying holdings they invest in. When comparing the responses over the past three years, fixed income managers show the largest year-over-year changes as more bond managers are incorporating engagement activities. Bondholder engagement has become a crucial part of the responsible investment approach and process. A growing number of bond investors hold the view that engagement activities can provide greater insights into the underlying companies or entities, improve transparency and influence business practices. As the importance of active ownership continues to increase, so will the consensus among investors to incorporate active management across all asset classes.

A growth in ESG product offerings

We have observed ESG-related product expansion across asset classes, with an increased number of assets going into ESG and responsible investing strategy offerings over the recent years. We asked asset managers to share the firmwide assets under management with strategies that are clearly defined as responsible investing or that incorporate ESG considerations, as of 31 March 2021. 57% of the respondents offer some form of ESG-related and/or responsible investing strategy. 36% of the overall ESG strategy asset base is less than US$1 billion total, compared to 43% in 2020 and 48% in 2019, indicating that ESG strategies have grown to over $1 billion for most respondents.

In order to gain a deeper understanding of ESG-related strategy offerings, we asked firms to classify the types of offerings they currently offer, including exclusionary screen-based, ESG integration, best-in-class/positive tilt-based and impact/thematic strategies. Across the asset classes, the strategies which provide ESG integration are the largest proportion of strategies offered to date. Additionally, we asked which type of strategies asset managers are seeing the most interest and asset growth in over the past 12 months. The results show proportionally more demand in ESG integrated strategies, which are often mainstream strategies that are benchmarked against traditional public indices, such as the MSCI EAFE Index and Bloomberg Barclays Global Aggregate Index. These findings suggest that investors may be looking to substitute existing core allocations for sustainable strategies with ESG outcomes.

Screening rises in prominence

Our 2021 survey results identify that screening is one of the most widely used tools utilised to implement a responsible investment policy in the asset management community. Screening uses a set of criteria to determine which sectors, companies or countries are eligible or ineligible to be included in a specific portfolio as a baseline investment decision. Negative screening with values or ethical-based criteria focuses on product-based considerations and tends to centre on certain sectors, such as tobacco, controversial weapons and thermal coal. Norm-based screening focuses on business conduct or operation irrespective of sectors, such as United Nations Global Compact violators. Positive screening focuses on business activities that may identify firms as leaders among peers. In order to gauge the level of screening practices, we asked which screening criteria the asset managers utilise for both labelled and non-labelled sustainable strategy offerings.

The most popular screening criteria is value-based negative screening for both labelled and non-labelled sustainable strategies. Specifically, 47% of the respondents who use some form of screening criteria apply the value-based negative screening for the labelled sustainable strategies. For non-labelled strategies, the use of the negative screening practices was the highest among European-based asset managers, where the majority of them utilise negative screening criteria (even in non-labelled strategy offerings).

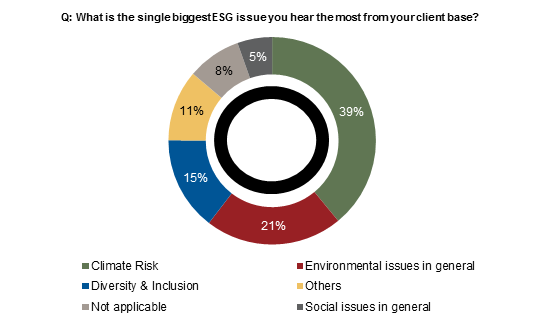

Climate risk: The greatest issue flagged by asset managers’ clientsAs ESG considerations cover a wide range of topics, we asked the survey participants to select the single largest ESG issue they tend to hear from their client base. With financial regulators making it a priority and asset owners continuing to highlight the growing urgency around climate change, it was no surprise that climate risk was flagged as the greatest issue relating to ESG that the respondents hear from their client base. Specifically, 39% of the respondents selected climate risk, followed by 21% for environmental issues in general. 15% of the respondents selected Diversity, Equity and Inclusion (DEI) as being the top ESG issue. Among the respondents who selected “Others” in this section, many cited that both climate risk and DEI are equally seen as a consistent issue.

Click image to enlarge

Will COP26 further drive the focus on climate risk

In April this year, Russell Investments joined the Net Zero Asset Managers Initiative, a group of international asset managers committed to supporting the goal of net zero greenhouse gas emissions by 2050. Launched in late 2020, this initiative is endorsed by the Investor Agenda with founding partners including the Institutional Investors Group on Climate Change (IIGCC), Ceres, a sustainability advocacy organisation, and the Principles for Responsible Investment (PRI).

As climate change plays an integral role across the globe, with financial institutions needing to take action, we asked managers if they have signed up to the Net Zero Initiative – and if not, whether they plan on joining. As a participant in this initiative, the firm must be committed to working in partnership with its clients on goals consistent with an ambition to reach net-zero emissions by 2050 across all its assets under management.

The survey results show that asset managers based in the U.S. include the highest number of signatories, with a large proportion of those not already signed up stating that they are seriously considering. The UK and Europe are not far behind - which is likely due to regulatory pressures and increased demand from clients seeking to align with net zero emissions by 2050.

In November, the UK hosted the United Nations Climate Change Conference (COP26). The COP26 summit brings almost every country together to accelerate action towards the goals of the Paris Agreement and the UN Framework Convention on Climate Change.

The bottom line

The 2021 Russell Investments ESG Manager Survey revealed a continuously high level of ESG awareness and increasing integration of ESG data and analysis into investment processes within asset management. The survey results conclude that while the starting point varies, many asset managers are evolving their ESG integration practices to capture material ESG-related information in their investment processes. Many firms have moved their ESG integration practices from making a gesture to meaningful compliance. Others have shown greater commitment, such as identifying material ESG-related information and incorporating such inputs into key investment decisions. Ever-growing regulatory pressure and client demand are further pushing ESG integration practices, with no end in sight. The speed of adoption creates its own issues, and many asset managers are trying to navigate through rapid adaptation and expansion of ESG integration.

At Russell Investments, we take a holistic approach to portfolio construction and management. Our goal is to achieve best-practice ESG integration to effectively capture ESG materiality. We believe that ESG topics, including DEI and climate change, can have material impacts on capital flows, which can influence asset prices. An integrated ESG process allows ESG issues to be understood and managed holistically. We believe that this approach not only allows for the best outcomes for our clients, but for our society and planet as well.

The question remains, will the focus on climate risk and commitment to reaching net zero greenhouse gas emissions by 2050 be further accelerated following the 2021 United Nations Climate Change Conference? We believe the answer is yes.

The survey was carried out between 24 May 2021 and 17 July 2021, with the results published 10 November 2021.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.