Japanese equities then and now: 25 key indicators and contributors to the current investment landscape

This year, we mark the 25th anniversary of the Russell Investments Japan Equity Fund, which launched in 1995, the same year that Amazon started to sell books online. The long-standing success of the Japan Equity Fund is testament to the team culture at Russell investments, a key contributor to the strong performance to date, helping it thrive despite turbulent times in the Japanese economy. As of June 2020, the core team of the Japan Equity Fund is made up of individuals with a combined experience of over 93 years in the industry and 63 years at Russell Investments.

In keeping with the anniversary theme, we explore 25 factors of notable events, trends and changes to the Japanese economy, as well as some of the key contributors to the success of the Russell Investments Japan Equity Fund over the past two decades.

1. A flexible approach - As shown in the below chart, Japanese equity styles have changed significantly. During these times of change, we have kept a nimble approach, ensuring that we are able to change the portfolio structure to ride with the new direction of the market.

Source: Russell Nomura. Data as at 2019.

2. The lost decade - The Japanese asset price bubble collapse in late 1991 caused a lost decade for the economy. The central bank imposed a zero-interest policy in late 1990s to get the economy out of recession after the bubble crisis. The interest rate was reduced from 2% to 0.5% in 1995 and has further reduced to -0.1% as of June 2020.

3. A maverick persona prompts reforms - Junichiro Koizumi was Prime Minister from 2001 – 2006 and was a powerful force in Japan and a huge advocate for deregulation, which Japan went through during his tenure. Furthermore, Koizumi implemented the privatisation of the post-office savings system, a radical move to clear out bad bank loans and a curb on high state indebtedness.

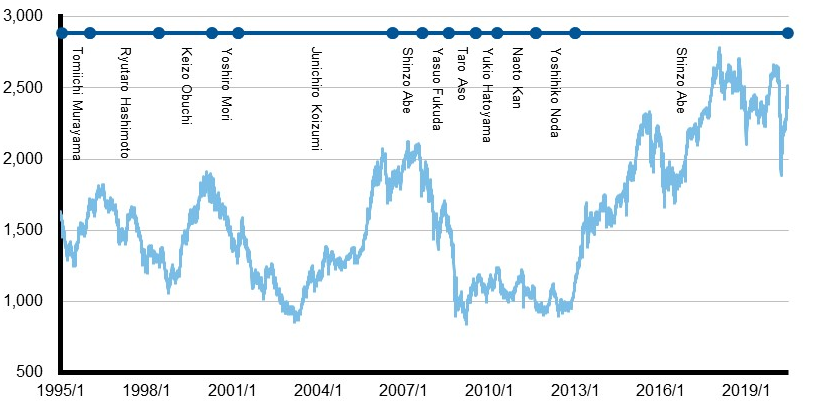

4. Political volatility - Japan experienced a rollercoaster of political leadership, with a number of leaders in just six years. This created uncertainty amongst corporate companies, with many of the larger firms moving their Asian headquarters outside of Tokyo. The below chart shows the (monthly) movements in the TOPIX throughout the political changes.

Source: Bloomberg and Russell Investments. Data as at 29 May 2020.

5. The sleeping nation awakens - Despite its preponderance of high-growth tech companies, the Japanese stock market has traditionally held a reputation for being littered with so- called ‘zombie’ companies and investors alike: those which have been barely profitable over many years and only survive thanks to support from the government or from affiliated companies in the same ‘Keiretsu’ (a set of companies with interlocking business relationships and shareholdings). However, this is now changing for the better. Japan remains a great place for active management, and particularly for those able to find the best active managers.

6. A strengthening yen - Over the past 25 years, the Japanese yen had traded at similar levels to the U.S. dollar. However, in the last quarter of a century the exchange rate has been on a rollercoaster ride, reflecting the relative fortunes of the Japanese economy. The below chart shows the movements in the yen versus the U.S. dollar.

Source: Bloomberg. Data as at 29 May 2020.

7. A catalyst for corporate Japan to look outwards - The strengthening of the yen following the global financial crisis (GFC) negatively impacting export-oriented manufacturers. This became a strong argument to make corporate Japan invest overseas and move into a more ‘open economy.’ Despite trade balance surplus previously being taken for granted, dividend income or returns from overseas subsidiaries or investments are meaningfully positive.

8. An injection of fiscal stimulus - In 2013, Prime Minister Abe announced a fiscal stimulus package of 10.3 trillion yen. The aim of the stimulus was to complement private spending in the economy in order to stimulate growth, which was partially paid for through an increase in consumption tax.

9. Shareholder activism - Japan’s Stewardship Code was issued in February 2014. The Stewardship Code has been put in place to further promote and achieve effective corporate governance. Under such circumstances, shareholder activism in Japan has grown.

10. Company governance structures begin to take shape - Significant improvement to corporate governance has been implemented, following the introduction of Japan's Corporate Governance Code, which came into force in June 2015. The Governance Code ensures that companies respond to requests from shareholders to engage in dialogue. Furthermore, the board of directors should establish, approve and disclose policies relating to measures and organisational structures that aim to promote constructive dialogue with shareholders.

11. Kuroda Bazooka - The current Governor of the Bank of Japan, Haruhiko Kuroda, shocked the economy in 2016 as it led Japan’s move into negative interest rates, after a stretch of economic weakness.

12. Female empowerment in the workforce - Abe has encouraged more women to enter the workforce and relaxed immigration laws to allow a modest number of blue-collar workers to fill gaps in pressurised sectors of the economy.

13. A fight for better working conditions - The government amended labour laws (which came into effect in April 2019) to improve working conditions by reducing hours, revising wage laws and annual leave rules. The hope is that employees less able to work long hours or more labour-intensive jobs (such as the elderly, parents/carers or disabled) will remain, enter or return to the workplace.

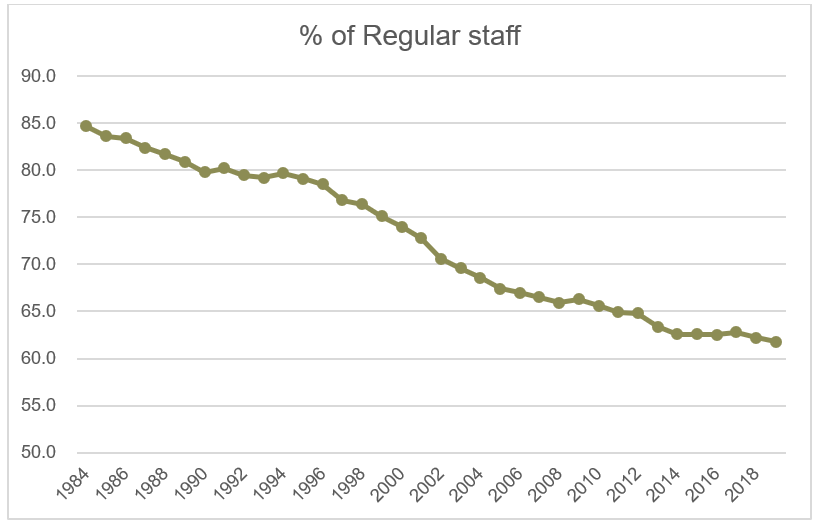

14. Lifetime employment - If you are classed as a permanent employee in Japan, you are entitled to stay at that company during your lifetime. The below chart demonstrates the effect of the ‘lost decade’ on companies in Japan, with the significant decline in lifetime contracts and an increase in contracting / temporary employees.

Source: The Japan Institute for Labour Policy and Training.

15. Networking across the globe - Japanese companies are entering a new phase of globalisation, with an increased number opening headquarters overseas and providing a full localised service to international customers.

16. A tech boom - The modern industrial history of Japan is a story of technology adoption, advancement and in some cases domination. While other Asian countries have taken the lead in certain areas of technology, Japan remains at the cutting edge in some of the highest tech components. So, while your iPhone may be designed in California and assembled in China, some of the most critical components will have been manufactured in Japan. One example is Murata, a leading company in the manufacturing of electronic components, ranging from communication and wireless modules to power supplies.

17. Dividends are on the rise, but wages are not - The net profits of Japanese companies grew by 630% from fiscal 2000 to 2018, according to corporate earnings data provided by the Finance Ministry. During that period, labour costs rose only 3%, but dividends jumped 440%.1 In other words, much of the wealth created by companies has gone to shareholders, not their employees.

18. The Abenomics rally - Retail investors sold almost a net nine trillion yen ($82 billion) of stocks in 2013, when Prime Minister Shinzo Abe ushered in his reflationary policies. In contrast, foreign investors made net purchases worth 15 trillion yen, positioning themselves to benefit from the subsequent Abenomics rally.2 Furthermore, share ownership ratio of foreign investors has increased from 10.5% to 29.1% (from 1995 to 2018). The daily volume of Japanese equities executed on behalf of foreign investors has increased dramatically.

19. ROE to grow - Despite being lower than levels in Europe and the U.S., the gap in return on equity (ROE) between Japan and other countries has shrunk in recent years. There are ample reasons to believe that Japanese companies will look to continue improving their ROE, especially with corporate profit margins at historical highs. Furthermore, there is significant pressure on companies to increase returns to shareholders based on improved corporate governance standards.

20. To merge or not to merge - A structural change is taking place amongst Japanese companies, with an increase in mergers and acquisitions, as more large corporate companies are buying smaller competitors and consolidating their industries. This is likely to further increase over the coming years.

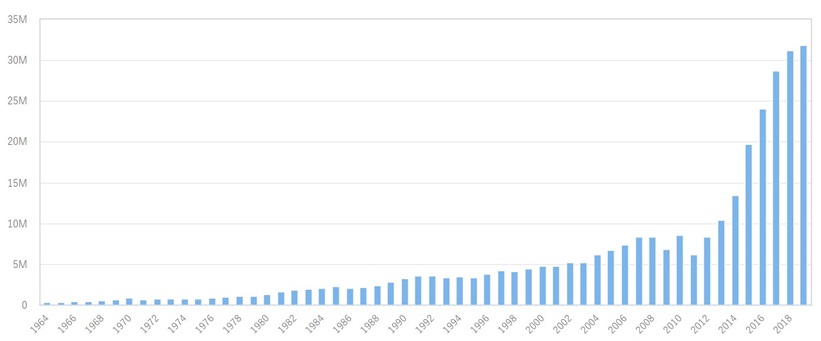

21. Japan jumps up the tourism leaderboard - The boom in Japan’s inbound tourism is arguably the most tangible success story of Abenomics. The following chart shows the dramatic increase in Japan’s tourism and the United Nations World Tourism Organisation estimates that 31.2 million overseas travelers stayed in Japan in 2018, a rise of 263 per cent since 2010. In September 2019, it was the 11th most visited country in the world.3 Abe’s expanded consumption tax exemptions for tourists, as well as a relaxation of visa requirements on Chinese tourists, could lead to further growth in the country’s tourism industry.

Source: United Nations World Tourism Organisation.

22. Diversifying for success - One of the key contributors to the success of the Russell Investments Japan Equity Fund over the past two decades is the multi-manager approach. This approach enabled diversity across a number of factors; including the team (located in both Tokyo and Sydney) and the vast amount of research carried out to find the best-in-class managers.

23. Under researched yet not underestimated - Small and mid-cap Japanese stocks are under researched relative to large and mega-cap stocks, providing better alpha opportunities for investors.

24. Japan’s response to the global pandemic - Japan’s death rate per capita from coronavirus is one of the lowest in the developed world, more than 70 times lower than the UK and 40 times lower than the U.S. Despite having a lower death rate from the coronavirus, Japan’s economy has suffered with the rest of the globe. On Tuesday 16 June, The Bank of Japan increased its COVID-19 stimulus from 75 trillion yen ($700 billion) to 110 trillion yen ($1.02 trillion).

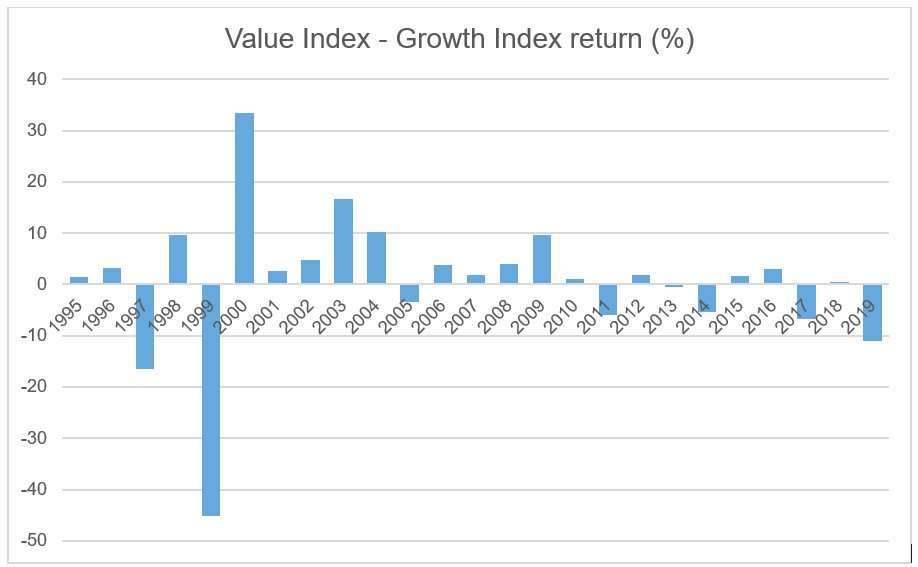

25. Mysterious Japan - There remains a mystery of Japan-specific factor pay-offs. The value factor has outperformed the growth factor in the past 18 out of 25 years. This is in contrast with the rest of the world, where the patience of value investors has been tested to the limit. Conversely, the momentum factor has not worked as well in Japan as it has in the rest of the world. The reasons are widely debated. Part of the reason lies with Japan’s highly cyclical corporate profits, which favour value stocks in the rebounds, and with Japan’s more stable institutional and retail share ownership, which pays less attention to tracking-price momentum trends.

The bottom line

The past two and a half decades have been both turbulent and triumphant for the Japan economy, as the country begins to recoup confidence from international investors. Japanese companies have been challenged by corporate governance to streamline, shareholders are becoming more active and dividends are growing.

During this 25-year period, the management style of the Russell Investments Japan equity portfolio has been materially influenced by the perspective of the managers hired within the fund. While domestic managers have advantages with regards to grassroots information and native language, managers located elsewhere can often benefit from being located away from the local hype. Comparing and contrasting how Japanese companies are performing relative to offshore players can add significant value.

At Russell Investments, we believe that the positive shift in corporate culture and reforms over the past two decades have created opportunities for outperformance by skilled managers with strong research capabilities. We also believe that the opportunity set and outlook for Japan is currently very attractive.

Discover more in our Q&A with Makiko Hakozaki, Director, Senior Portfolio Manager, Japanese equities.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

The value of investments and the income from them can fall as well as rise and is not guaranteed. You may not get back the amount originally invested.