Bank of England: A surprise end to UK rate hikes?

Executive summary:

- BoE shocks markets by holding off on a rate increase

- We believe it is likely we have seen the last rate hike of the cycle

- It is now even more important for Defined Benefit pension schemes to have a clear liability hedging policy in place

Today, in a shock decision, the Bank of England (BoE) left its policy rate at 5.25% by the tightest possible majority vote of 5-4. All but one of 65 economists polled by Reuters had predicted that the BoE would raise the rate to 5.5%.

The likely reason for this unexpected decision was the downward surprise on inflation. Yesterday, good news emerged in the latest inflation report, showing that the UK’s inflation rate eased in August, defying expectations of a further rise.

The consumer prices index (CPI) measure of inflation fell to 6.7% year-on-year, down from 6.8% in July and lower than the consensus forecast of 7.0%. The core CPI, which strips out volatile items such as food and energy, dropped to 6.2% from 6.9%, significantly below the 6.8% predicted by economists.

We believe this will be met by relief in the halls of the Old Lady. Despite the risk of a sharper economic slowdown, the Monetary Policy Committee (MPC) members are very mindful of their own credibility, which has suffered from the surge in inflation starting in mid-2021 to a peak of 11.1%.

What do we think this means for markets?

Money market traders now price a 50-50 chance of one more 25 basis point rate hike over the next six months. However, we believe it is more likely that we have seen the last rate hike of the cycle.

If the zenith is indeed at the current level of 5.25%, having embarked on its journey from a mere 0.1%, the BoE’s current cycle would secure its place as the fourth most substantial tightening cycle in Britain's annals over the past century. The potential end of a central bank tightening is often a good time to think about investing into longer-term bonds.

Each prior instance of rapid rate hikes has been followed by recession, casting an ominous shadow over households and financial markets. Presently, the prospect of a downturn looms large in the collective consciousness of the MPC. Even as the MPC has undertaken 14 rate hikes, the full ramifications of these measures have yet to permeate the real economy.

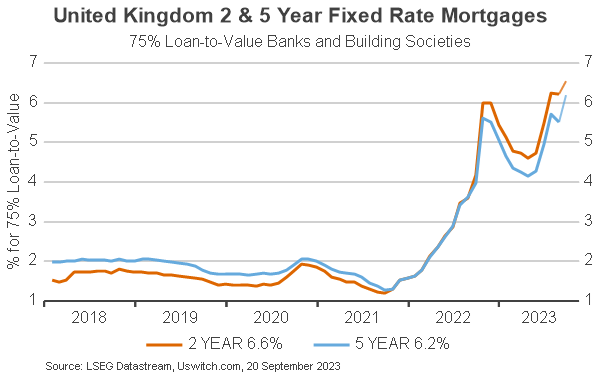

One obvious channel whereby the rate hikes will further dampen growth is the housing market. After reaching a trough of 1.2% in September 2021, the average 2-year fixed rate for a 75% loan-to-value mortgage has risen more than five-fold to 6.6% on 20 September (see chart). Due to rising global interest rates, UK mortgage rates are now higher than during the UK gilts crisis in September 2022.

The UK gilt curve steepened immediately after today’s surprise but is still heavily inverted, i.e. shorter-term yields are higher than their long-term counterparts. Two-year bond yields fell by 2 bps to 4.88% while 10-year rates held steady around 4.29% in response to the policy announcement.

The pound has struggled since the end of the tightening cycle that is now coming into view. Against the US dollar, it has fallen significantly from its 2023 high of 1.31. After dropping below 1.23 after today's BoE decision, sterling is now quite undervalued1 against the greenback, which could limit further depreciation pressures.

The bottom line

We have thought for some time that the BoE is already overtightening. It is trying to regain lost credibility in controlling inflation at the cost of a likely sharp slowdown in the UK economy.

As the Bank of England has reached a likely peak in its rate hiking cycle, the rise in longer-term bond yields could also come to an end. It is therefore important for Defined Benefit pension schemes to have a clear liability hedging policy if they are seeking to control funding level variability.

In the wake of the tumultuous events that unfolded during the LDI crisis of 2022, establishing and upholding an effective governance and implementation framework is an imperative.

1 The purchasing power parity exchange rate for GBP/USD is around 1.48. Source: Organisation for Economic Cooperation and Development.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.