Bank of England: Rate cuts coming into sight

Executive summary:

- The Monetary Policy Committee (MPC) vote in favour of keeping the Bank of England (BoE) policy rate at 5.25%.

- Money market prices now imply the BoE will start cutting interest rates in June.

- Markets are predicting that economic weakness will force the BoE’s hand into eventually slashing interest rates.

Today, the MPC voted in favour of keeping the BoE policy rate at 5.25% with a 6-3 majority.

Jonathan Haskel and Catherine Mann preferred a hike while Swati Dhingra argued for a cut. The two hawks fear that underlying wage pressure could re-ignite inflation while Ms Dinghra pointed to sluggish demand growth. At the meeting prior, three members voted for a rate increase and no-one voted for a decrease.

All 70 economists polled by Reuters predicted that the BoE would stay on hold. Money market prices now imply the Bank of England will start cutting interest rates in June and are discounting more than 100 basis points on reductions by the end of 2024.

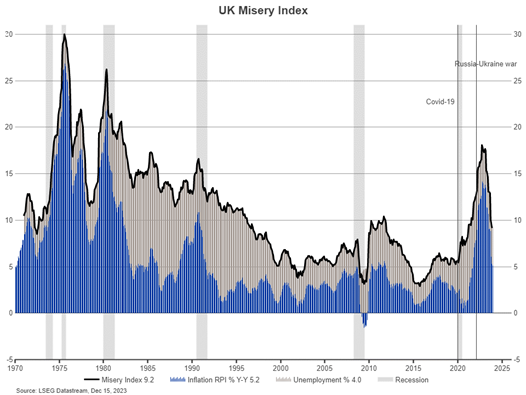

Misery Index still elevated

Misery Index UK: Inflation Rate (RPI) + Unemployment Rate

While the Misery Index has halved from its October 2022 peak, it is still close to the high end of the range since the BoE became independent in 1997 (excluding 2022/2023). In our view, the inflation component is likely to come down further, which would help to reduce the Misery Index. It is murkier on the jobs front. Looking at the decline in job vacancies, the labour market is softening, making it harder to reduce the Misery Index through a lower unemployment rate.

Market reaction: Gilts discount deep rate cuts

UK gilt markets have come a long way since Liz Truss’s mini-budget and the gilt crisis. Trading at 3.82% after the BoE decision today, 10-year gilt yields have fallen by around 100 basis points since October 2022. During the same period, the BoE raised the bank rate by 300 basis points. The spread between long-term bonds and the policy rate has slumped from over 2.2% at the peak of the gilt crisis to -1.45% today; an inverted yield curve, i.e. when the long-term yield is below the short-term rate, is often a good indicator of future recession and rate cuts.

Markets are predicting that economic weakness will force the BoE’s hand into eventually slashing interest rates.

The bottom line

The BoE is inching closer to a reversal on its monetary policy, leaving interest rates unchanged today, but hinting at rate cuts. Long-term yields have anticipated these rate cuts and have fallen sharply in recent months.

Fluctuations in bond yields can impact the liability value of Defined Benefit pension plans. Having a clear-cut strategy to hedge interest rate risk is crucial to manage ups and downs in funding levels. Especially after the bumpy ride of the gilt crisis in 2022, it's essential to set up and stick to a straightforward governance and implementation plan for liability hedging.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.