Why the climate transition means renewables are here to stay

The carbon emission obligations established under the monumental Paris Agreement of 2015 have gone largely unfulfilled and are at risk of failing. Sensing the urgency to attempt to rectify the situation, countries are now racing to implement mandates for the development of renewable energy assets and the requisite grid enabling infrastructure. These mandates are generating demand for renewable energy infrastructure which, in turn, may lead to an opportunity for investors.

The transition toward a more sustainable energy system presents opportunities for investors which have both patient capital and the sophistication to understand and underwrite the opportunity set. In this short article, we describe what renewable energy assets are and, why this opportunity has arisen. We finish by discussing the risks that investors should consider prior to committing to an investment in renewable energy and energy transition.

What is renewable energy?

The most basic forms of renewable energy generation are solar, wind and hydropower. The latter two technologies have been around for centuries. Over the past 10 years, solar and wind have been the biggest contributors to the rapid expansion of production capacity and are expected to be a driving force behind future growth as well.

In addition to focusing capital and attention on the forms of generation, there is an investment opportunity set focused on renewable-enablement strategies, for example; grid resiliency, smart meters and grid connections - which will be necessary to ensure that the overall energy system is adequate to handle the shift from hydrocarbon fuels - representing more consistent generation characteristics to renewable energy, which has higher levels of intermittency. The current energy system is centralised and top-down, it will require a bottom-up redesign focused on grid architecture. This redesign is a key component of the energy transition which will generate investment opportunities for investors in addition to renewable energy production.

How is the renewable energy market evolving?

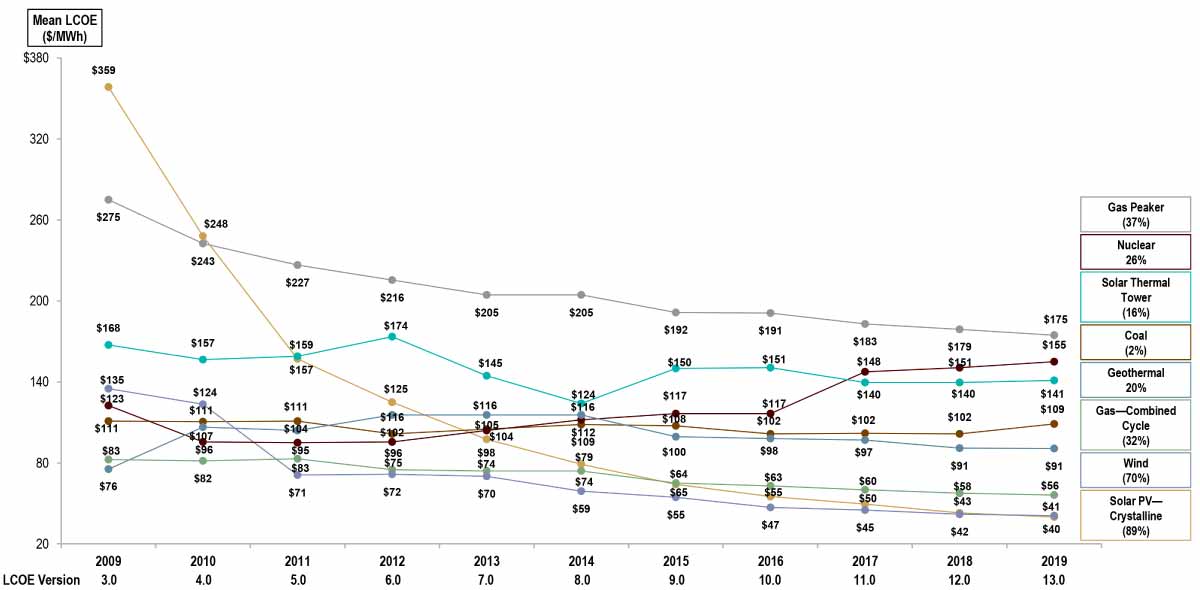

Boosted by a significant drop in the cost of installing and operating an energy asset over its lifetime - often quoted as the levelised cost of energy (LCOE) – in addition to continued government support in various markets, the installed capacity of renewable energy has grown dramatically over the past 10 years.

Renewable energy investment, a combination of public and private capital, exceeded $200 billion for the ninth year in a row. In 2018, new capacity breached the $250 billion mark for the fifth year, seeing a combined $2.6 trillion commitment to renewable energy investments and a four-fold increase in global renewable energy capacity.1 Solar energy has been the winner during that ten year period, with 638 gigawatts (GW) of new power capacity installed.

This rapid expansion of renewable energy capacity has supported the dramatic decline in the cost of technologies as they achieve greater scale. Since 2009, the LCOE for utility-scale solar photovoltaic and onshore wind power generation has dropped by a cumulative 89% and 70%, respectively.2 After a period of consistent and dramatic declines in cost it would not be an unreasonable assumption to expect that costs would stabilise, but that is not the case. Bloomberg New Energy Finance (BNEF)3 research group says that the global benchmark levelised cost of electricity (LCOE) for onshore wind and utility-scale photovoltaics (PV) has fallen 9% and 4%, respectively, since the second half of 2019 - to $44 per megawatt hour (MWh) and $50/MWh, respectively. The group predicts that wind and solar will eventually undercut commissioned coal and natural gas almost everywhere.

Source: Lazard’s Levelized Cost of Energy Analysis – Version 13.0

The ability to source electricity directly from renewable sources, together with achieving long term price certainty, has become a key business objective for corporates who are becoming increasingly pro-active in setting targets for renewable energy use. This has led to strong growth in corporate PPAs in recent years, particularly in the U.S., with major players including; Google, Apple, Amazon, Unilever, and Microsoft. The UK has seen deals from BT, Marks and Spencer, Nestle, McDonalds, HSBC, Lloyds, and Nationwide Building Society.

What might investors consider when committing capital to renewable energy?

Allocations to renewable energy assets may enhance investor portfolios by generating cash yield, providing diversification, and serving as a hedge against dislocations amid the transition to a lower-carbon economy. Approximately four-fifths of the world’s energy still comes from fossil fuels (renewable energy makes up a larger component of electricity generation at 25%). As such, investing in climate infrastructure may improve portfolio resiliency amid the transition to a lower-carbon economy.4

Renewable energy assets have historically offered multi-year, inflation-linked, contracted cashflows with creditworthy counterparties. Such assets can generate low-volatility cash yield in addition to limited correlation with public markets - thereby providing a genuine diversification benefit to investor portfolios.

As with any investment strategy, the benefits need to be considered in the context of the risks. The energy transition industry is in a period of rapid growth with a high risk of disruption in the form of new technology or competitive pressure. Technologies which appear attractive today could be usurped by innovative ones in the future that have the potential to make the former obsolete or less profitable. As a result, the strategy is best tackled by investors that are fleet of foot in order to navigate the rapid progress achieved in this sector - for an example of this, look no further than the dramatic cost reduction of solar power, which has fallen by 89% since 2010. To invest in this strategy, a tolerance for constantly changing landscapes will be necessary.

These are the material risks we believe an investor should consider before making an investment:

- Market (deflationary pricing pressure, see paragraph below)

- Credit (default)

- Operational (inefficient generation)

- Liquidity (availability of buyers at different asset age tranches)

- Technological risk

- Political (subsidy removal)

A general risk for investors in renewables is the long-term path of electricity prices. An increased supply of power generation assets - encouraged by renewables production targets set by national governments or other regulators - may lead to long-term price declines in the price of electricity if not met with an increase in demand. Although PPAs or subsidies can help create income certainty in the early life of assets, renewables investment requires assumptions about the price of electricity in the future. These future electricity prices determine the value of the assets after the PPAs or subsidies end, which can be important in determining the total return achieved by the investor over the life of the investment. Investors should be diligent in evaluating an investment’s exposure to future prices and working with a partner who understands this overarching risk.

What are the access points for renewable energy?

Investors can access renewable energy and energy transition opportunities via both the public and private markets. Public markets can often offer exposure to an existing portfolio of operational assets with the potential to incrementally construct new assets for inclusion in the portfolio. Over the past decade, the sector has become more mainstream in the listed equity markets. This is due to several of the oil and gas majors announcing carbon reduction plans focused on renewable energy or carbon capture, in addition to both public and private energy and infrastructure companies expanding their allocation to energy transition investments. The expanding ecosystem is necessary for the maturation of the sector and adds credibility to the opportunity.

Alternatively, investors can allocate capital via the private market which can either focus solely on one form of production (for example, solar) or take a diversified approach to creating a portfolio of various forms of production (for example, a combination of solar, wind and hydropower).

Given the constraints on direct infrastructure investing for most institutional investors, we believe the most efficient and scalable way to allocate capital to renewable energy assets and grid enablement infrastructure will involve investing through private infrastructure funds. From a dedicated fund investment perspective, the market is growing dramatically with a broadening opportunity set available to investors, which can now choose from global versus regional funds, and concentrated versus diversified. Historically, however, there have been too few institutional-quality funds with an exclusive focus on renewable energy. The universe of these types of funds is now evolving as experienced and successful energy infrastructure managers sharpen their focus on the investment opportunity. There are now fund managers in the renewable space which are investing capital from their third vintage funds and a collection of first-time fund managers which offer unique characteristics compared to their mature peers. Russell Investments is now tracking, in various stages, nearly 70 renewable energy funds. Such developments provide interesting new opportunities to accelerate the flow of institutional capital in support of climate solutions.

Building (greenfield) versus buying (operational)

Particularly within the unlisted market, investors have the option to choose how much asset risk they would like to take with their capital. In simplistic terms, the decision often boils down to whether to build or to buy. Our belief is that top-quality managers can often add value by targeting assets in the latter stages of development where additional return can be unlocked via the negotiation of revenue agreements (for example, PPAs) and construction contracts, restructuring existing permissions and by efficiently managing the construction process, which can range from 12 months to several years. In certain markets, the premium earned by taking on this type of risk has compressed to an unattractive level. This means that investors should make sure they understand where they deploy capital.

The significant flow of investment capital focused on long-term contracted income has distorted the risk-return balance in certain segments of the operational renewable energy market. Renewable energy assets bare varying degrees of credit and longevity/re-contracting risk, which is not being scientifically reflected in pricing in this environment. Over time, the expectation is that the market will evolve to better reflect these risks, but given the maturity of the market, this is not consistently the case today.

Why is it beneficial to have a global guide?

Across the globe, the pace of renewable energy penetration is not consistent which presents opportunities and challenges for institutional investors. Putting China to one side, the bulk of renewables deployment has taken place in North America and Europe, but we believe that the future is clearly in Asia.

Source: Bloomberg New Energy Finance 2018 New Energy Outlook June 2018.

The energy transition should be widespread, which we believe will generate a broad-range of investment opportunities ranging from renewable energy generation to pure-play infrastructure. Whilst there will be a diverse set of strategies that can be prosecuted by investors, the underlying focus on upgrading or renovating the energy system - inclusive of a much-needed emphasis on grid architecture - will be vital to ensuring our energy system is capable of supporting the way that humans will consume energy in the future.

Investors can benefit greatly from the services of a partner that has experience underwriting investments in all the key markets for renewable energy. In particular, we believe a partner benefiting from a global platform and a local regional presence will be best placed to identify the best-in-class managers, in terms of geography and technological capability. This, in turn, will help ensure that an investor is able to create the optimal portfolio from a risk-return perspective.

Read the full paper here.

1 Source: Global Trends in Renewable Energy Investment 2019, Frankfurt School, published September 2019.

2 Source: Global Trends in Renewable Energy Investment 2019, Frankfurt School, published September 2019.

3 Source: BloombergNEF, New Energy Outlook 2019.

4 Source: International Energy Agency, Data and statistics, 12 June 2020.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.